import re

import random

from pathlib import Path

import matplotlib.pyplot as plt

import matplotlib.dates as mdates

import numpy as np

import pandas as pd

from sklearn.linear_model import LinearRegression

from sklearn.metrics import mean_squared_error

from sklearn.preprocessing import LabelEncoder

from sklearn.model_selection import train_test_split

from sklearn.feature_extraction.text import CountVectorizer

import keras

from keras.models import Sequential

from keras.layers import (Dense, Input, Rescaling, Reshape,

SimpleRNN, GRU, LSTM, Bidirectional, Embedding)

from keras.callbacks import EarlyStoppingTime Series & Recurrent Neural Networks

ACTL3143 & ACTL5111 Deep Learning for Actuaries

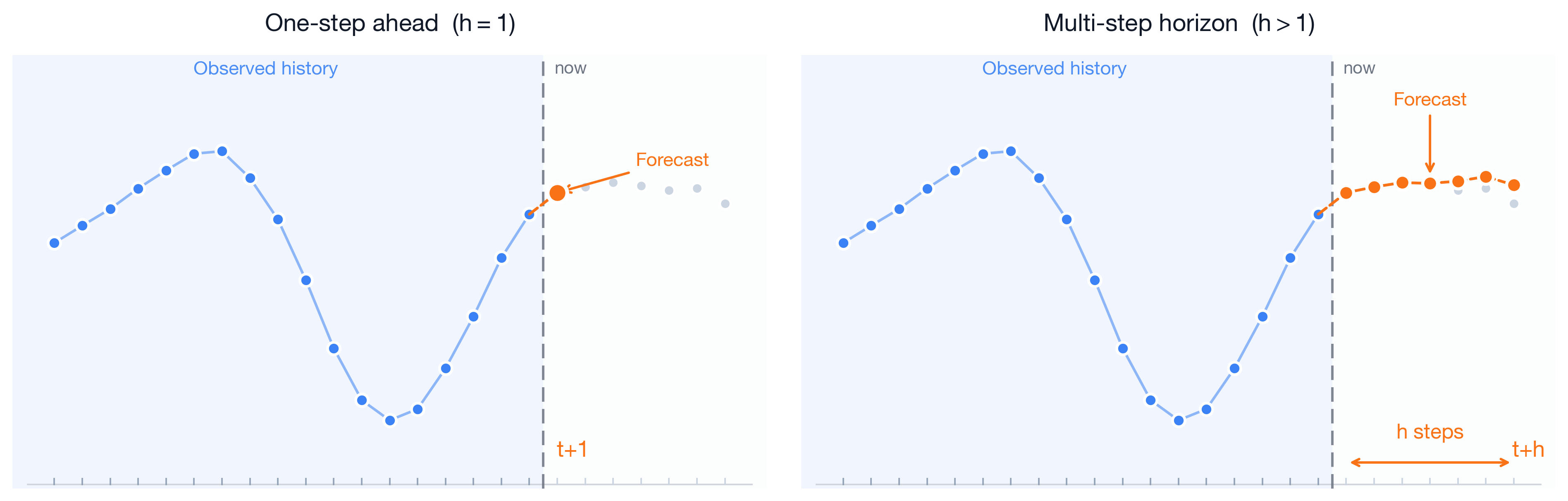

The forecasting problem

We stand at a reference time t: we have seen the series up to now, and want the next h values.

We need to know all covariates at time t to make a prediction at t+1.

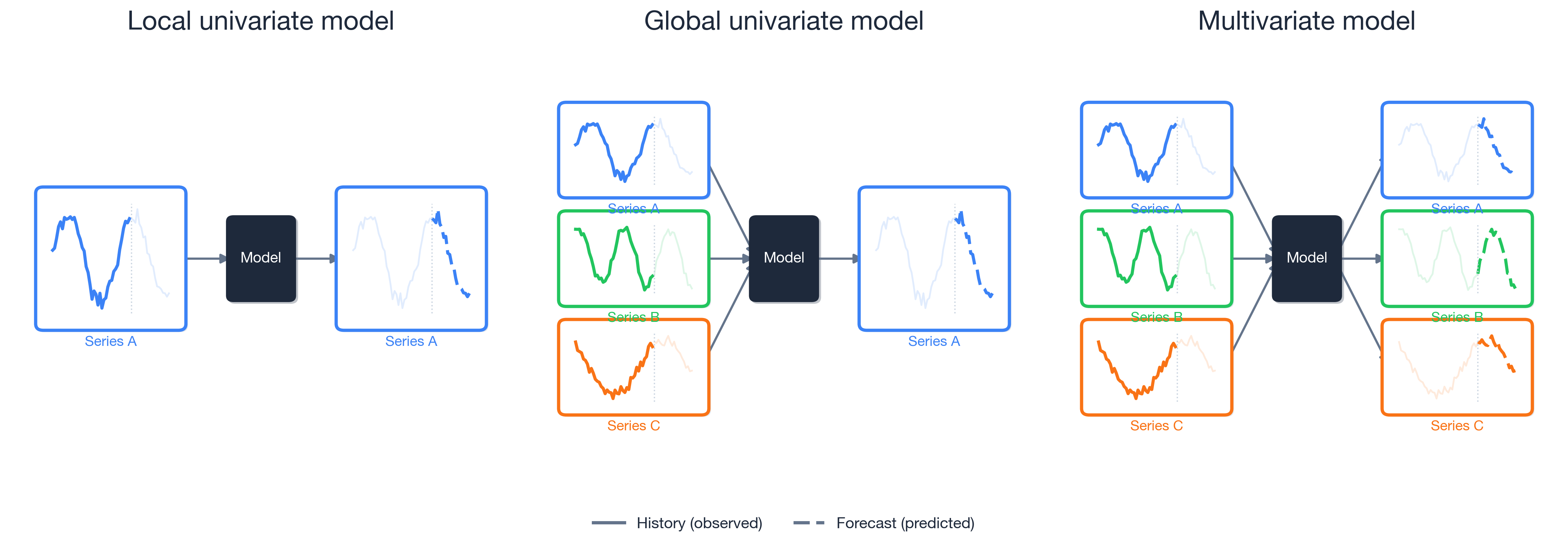

Three kinds of forecasting models

A schematic contrasting local univariate models (one series predicts itself), global univariate models (multiple series predict one), or multivariate models (multiple inputs, multiple targets).

For local models, you would have a separate model for each time series. Global models allow for cross-learning, and are more promising for deep forecasting techniques.

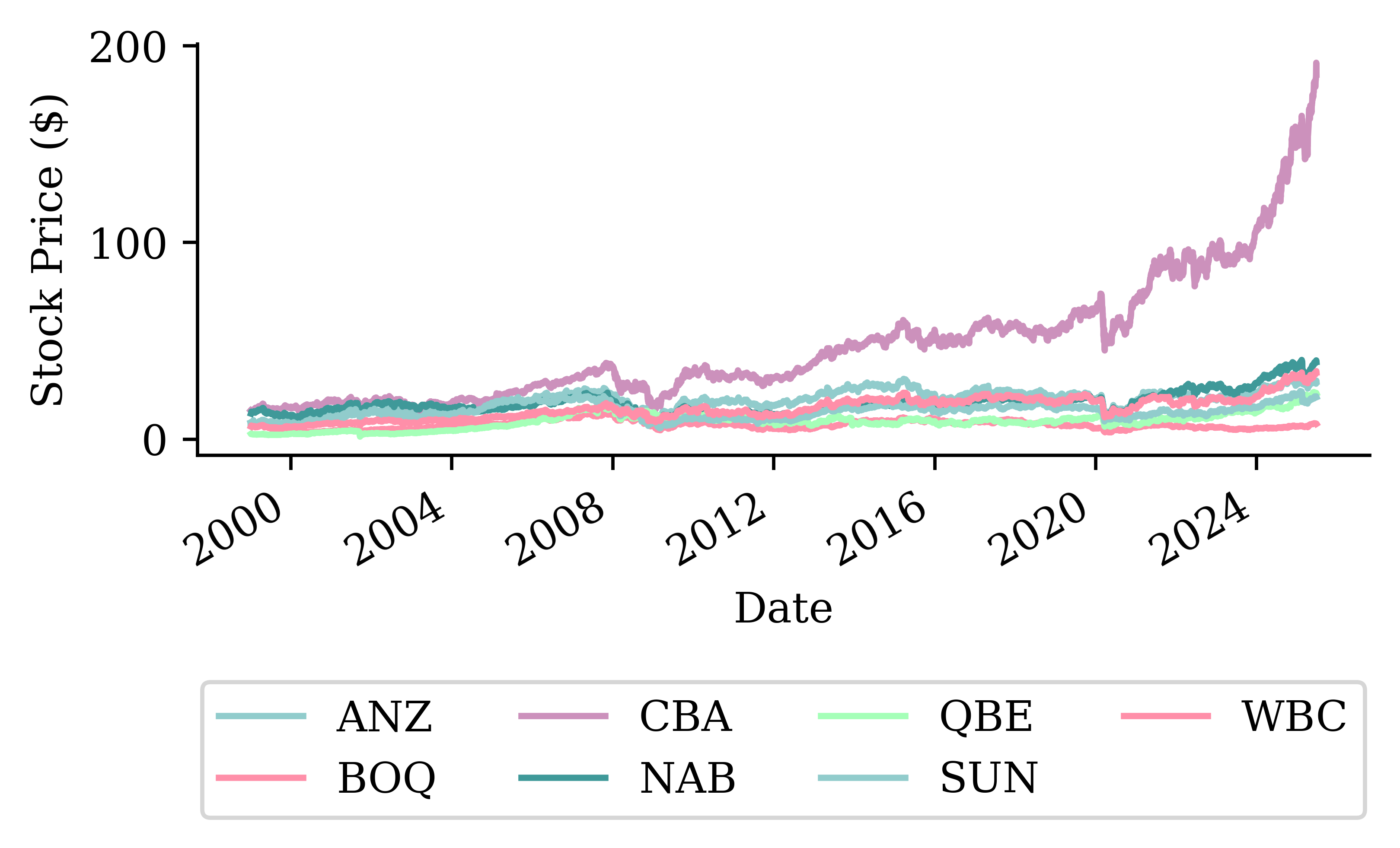

Plot

Question

What is wrong with this plot?

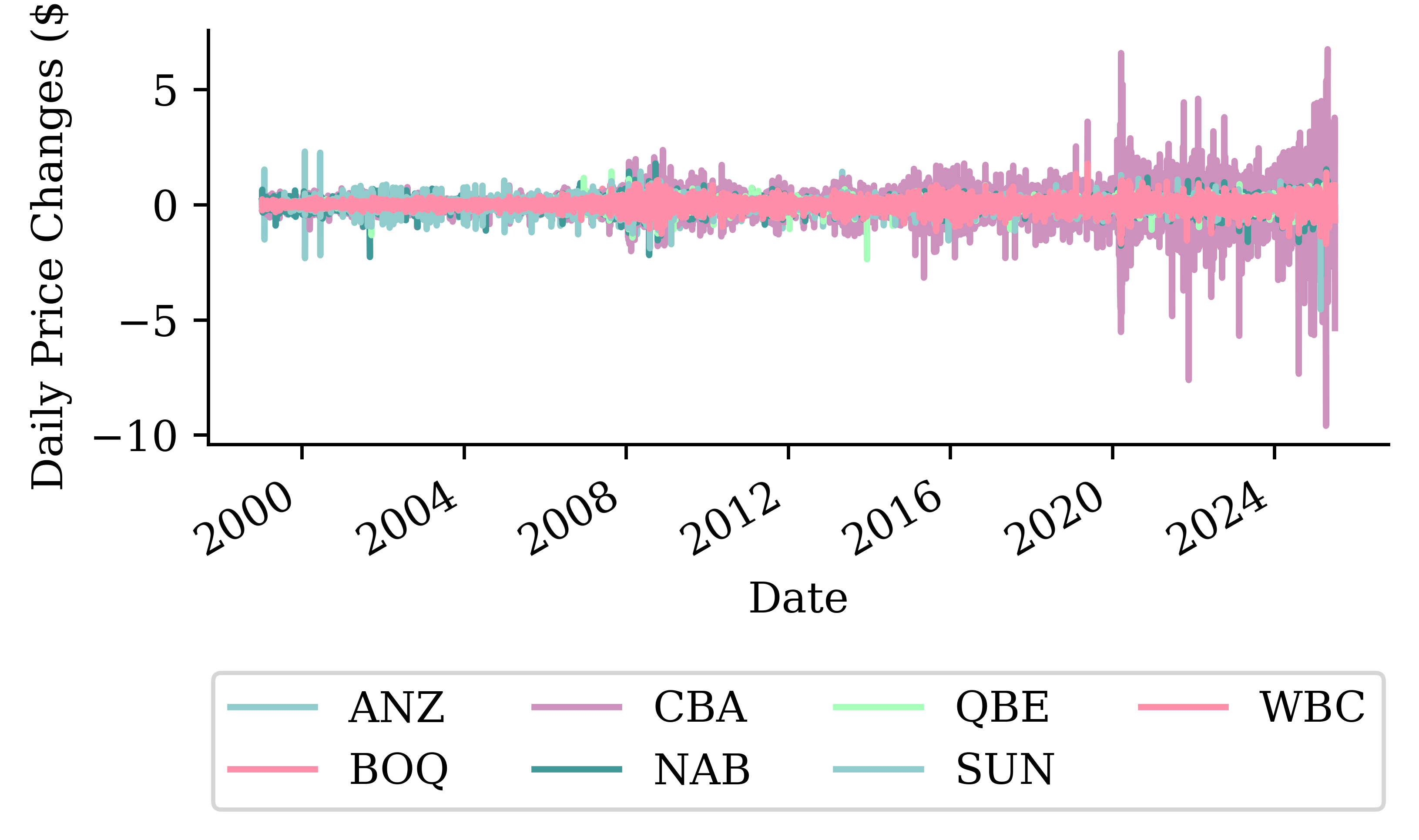

Plot II

Can look at the first differences

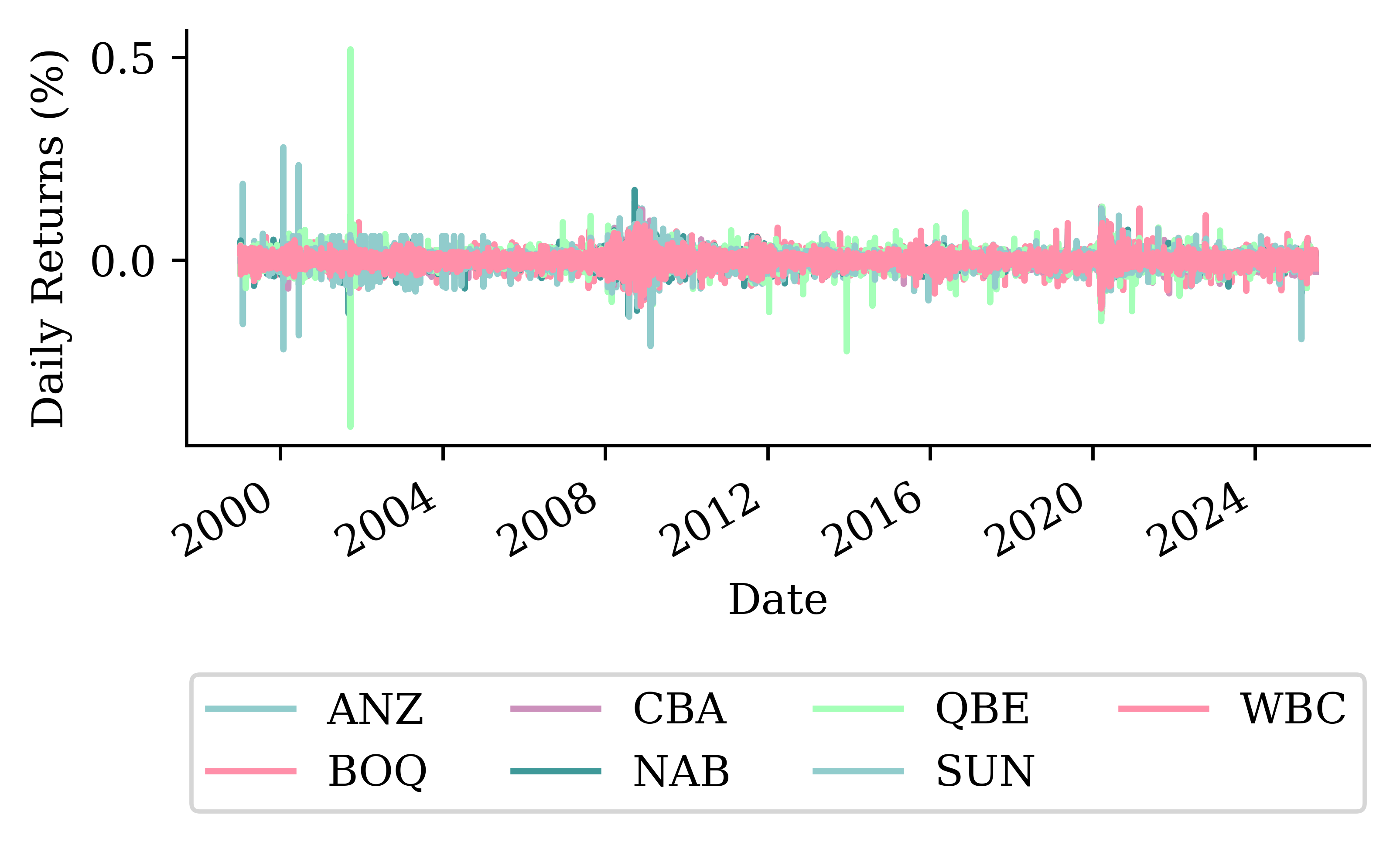

Can look at the percentage changes

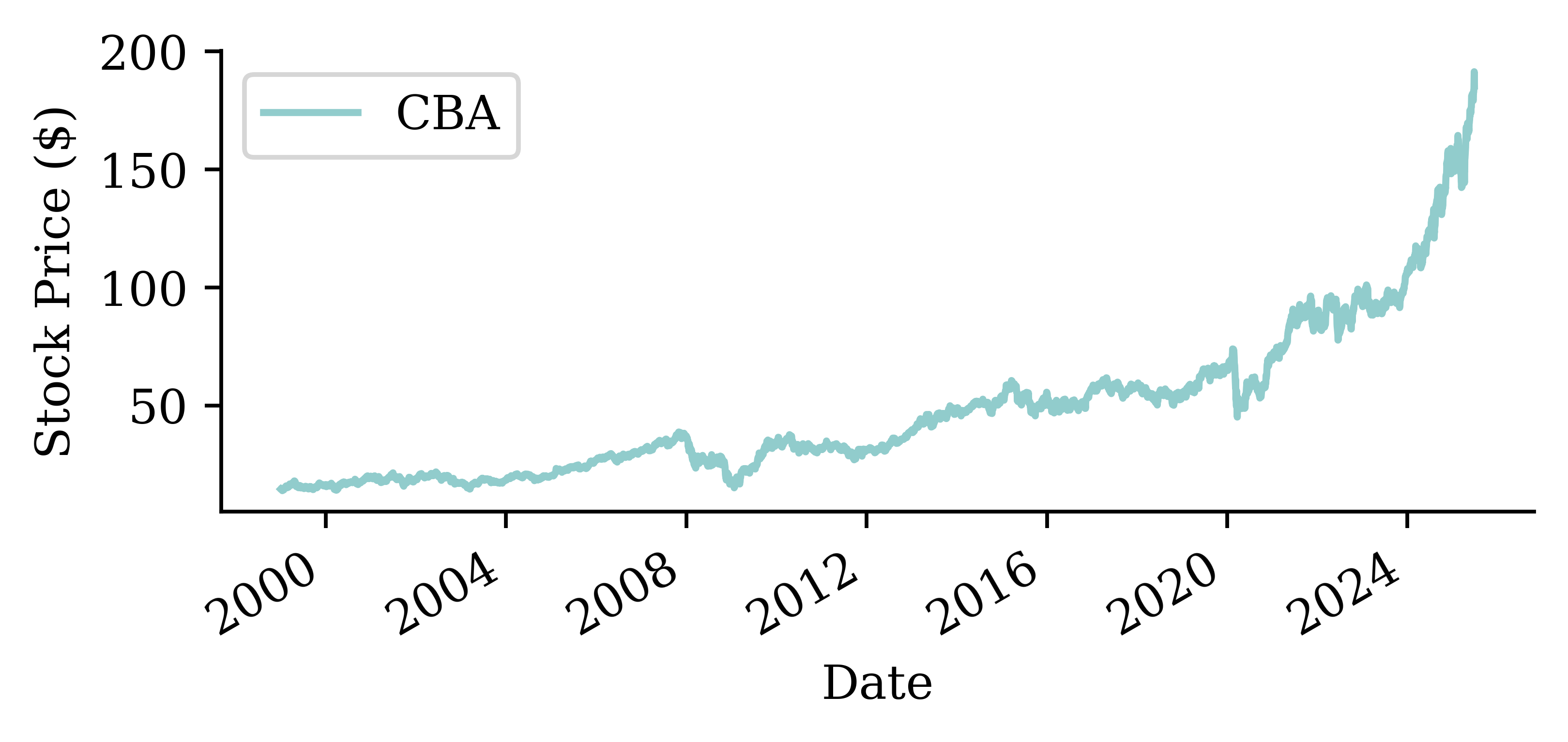

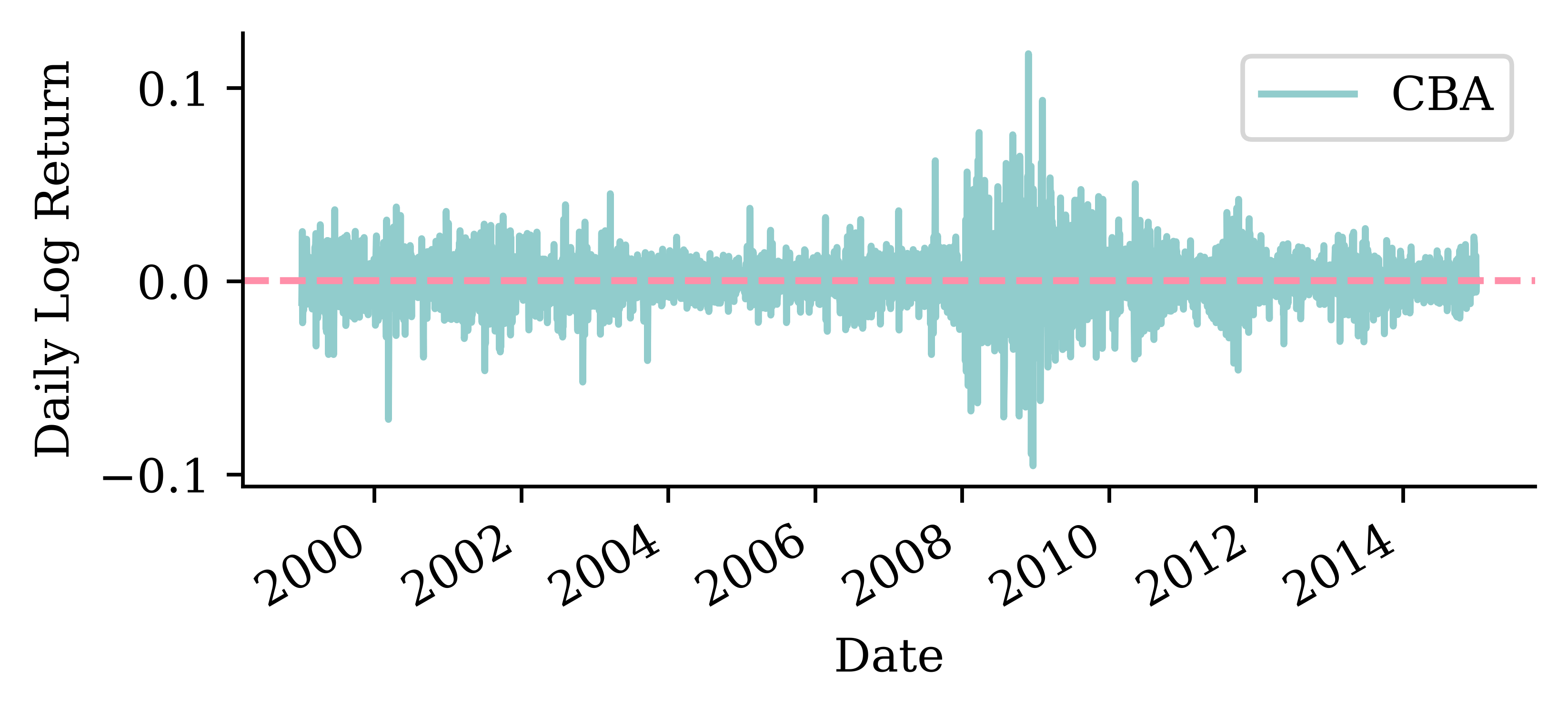

Focus on one stock

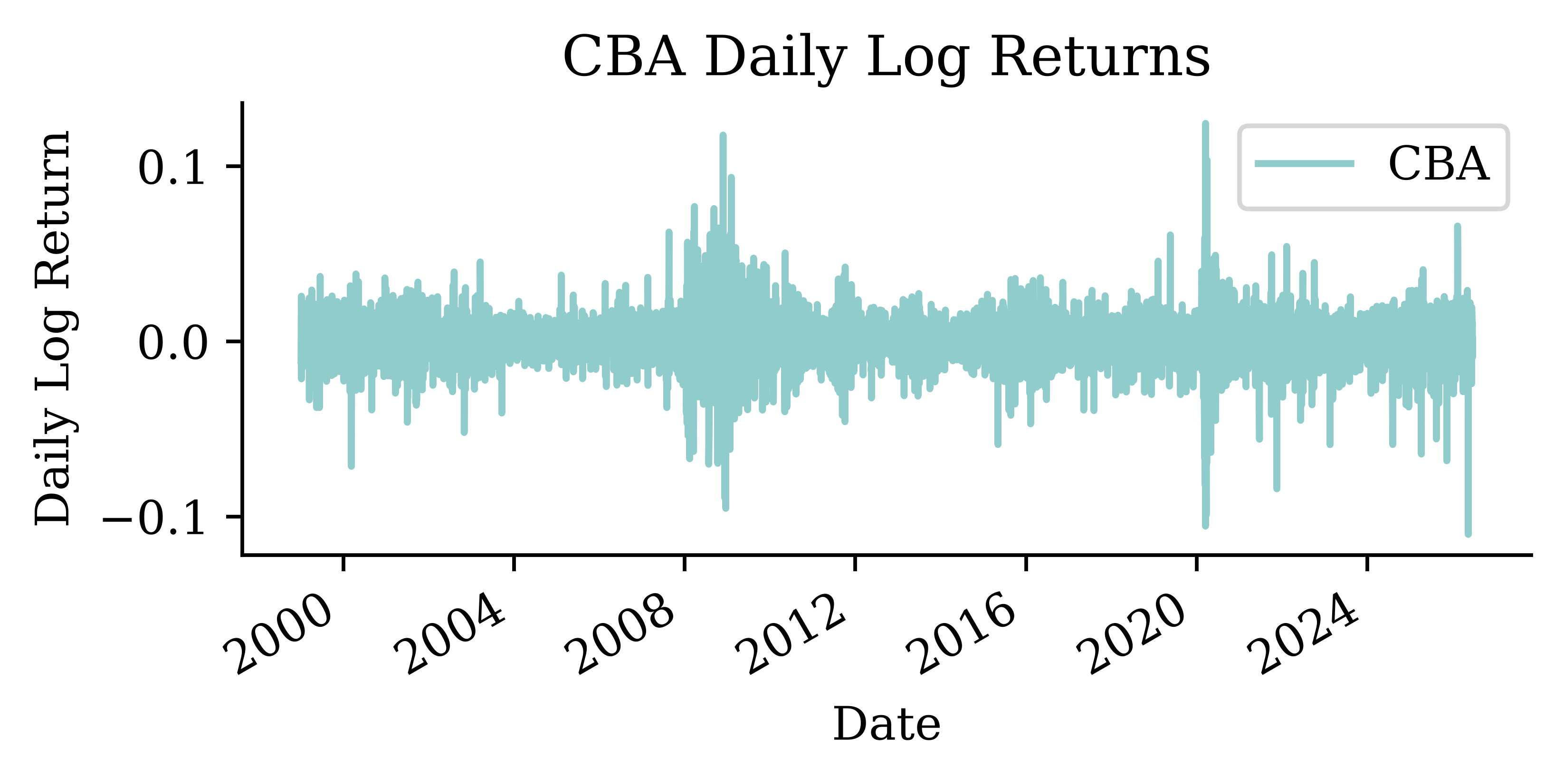

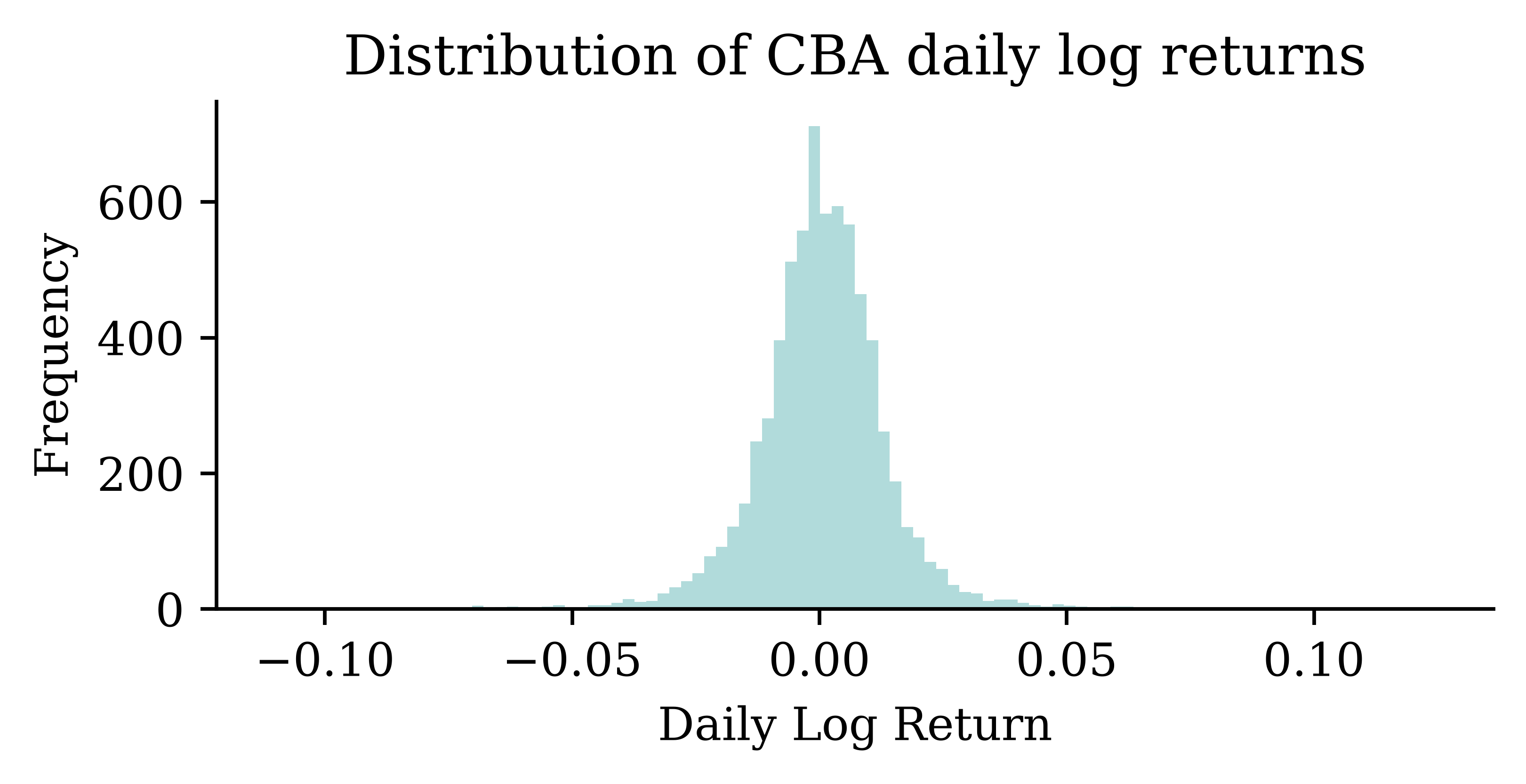

Convert to log returns

Instead of working with raw prices, we’ll work with daily log returns:

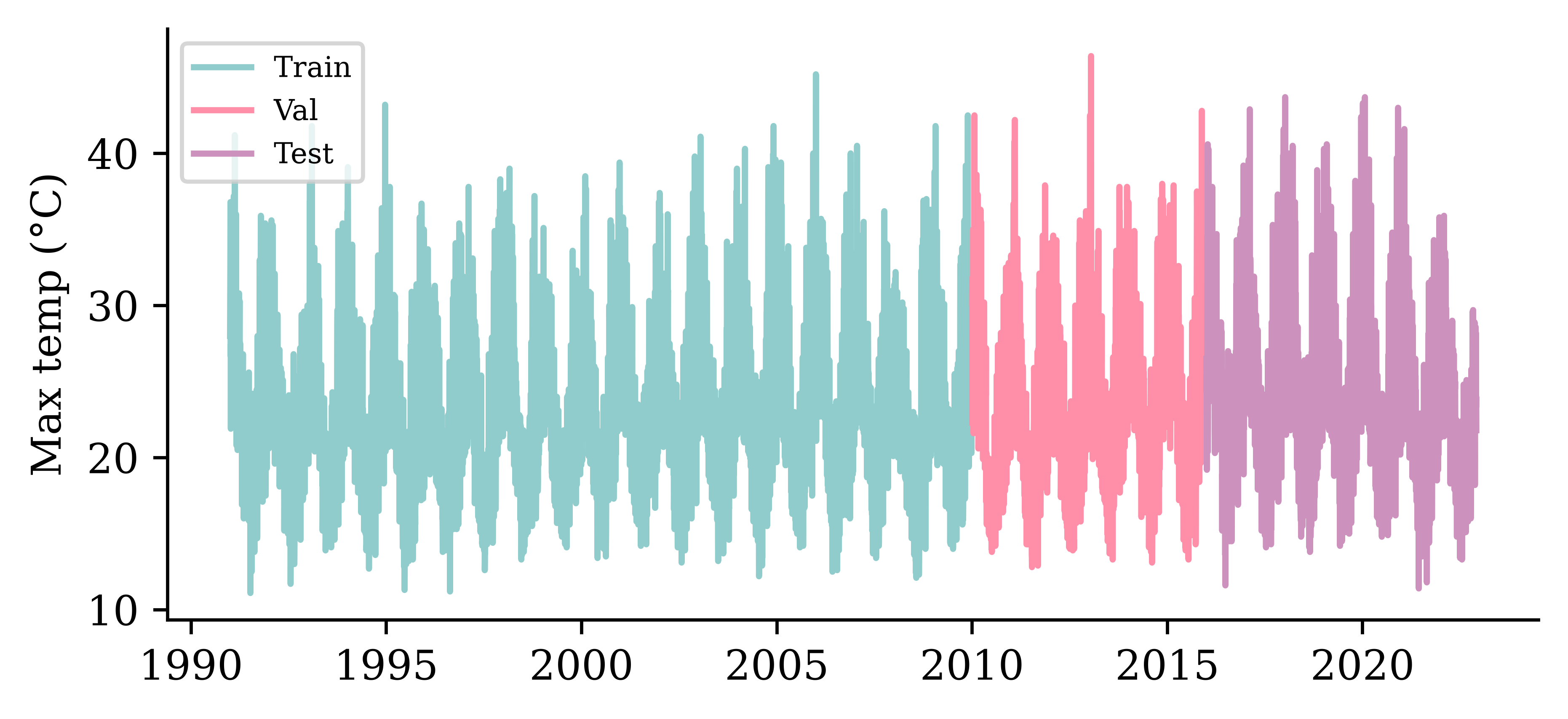

Splitting in time

We never shuffle a time series: train on the oldest data, validate on the middle, and keep the most recent years to test on. The cutoffs live in one place — change these lines to re-split.

Code

import matplotlib.dates as mdates

fig, ax = plt.subplots(figsize=(6, 2.6))

for label, lo, hi in [("Train", None, cba_train_end), ("Val", cba_val_start, cba_val_end), ("Test", cba_test_start, None)]:

ax.plot(stock["CBA"].loc[lo:hi].index, stock["CBA"].loc[lo:hi], label=label)

ax.set_ylabel("CBA price ($)")

ax.xaxis.set_major_locator(mdates.YearLocator(5))

ax.xaxis.set_major_formatter(mdates.DateFormatter("%Y"))

ax.legend(loc="upper left", fontsize=7);

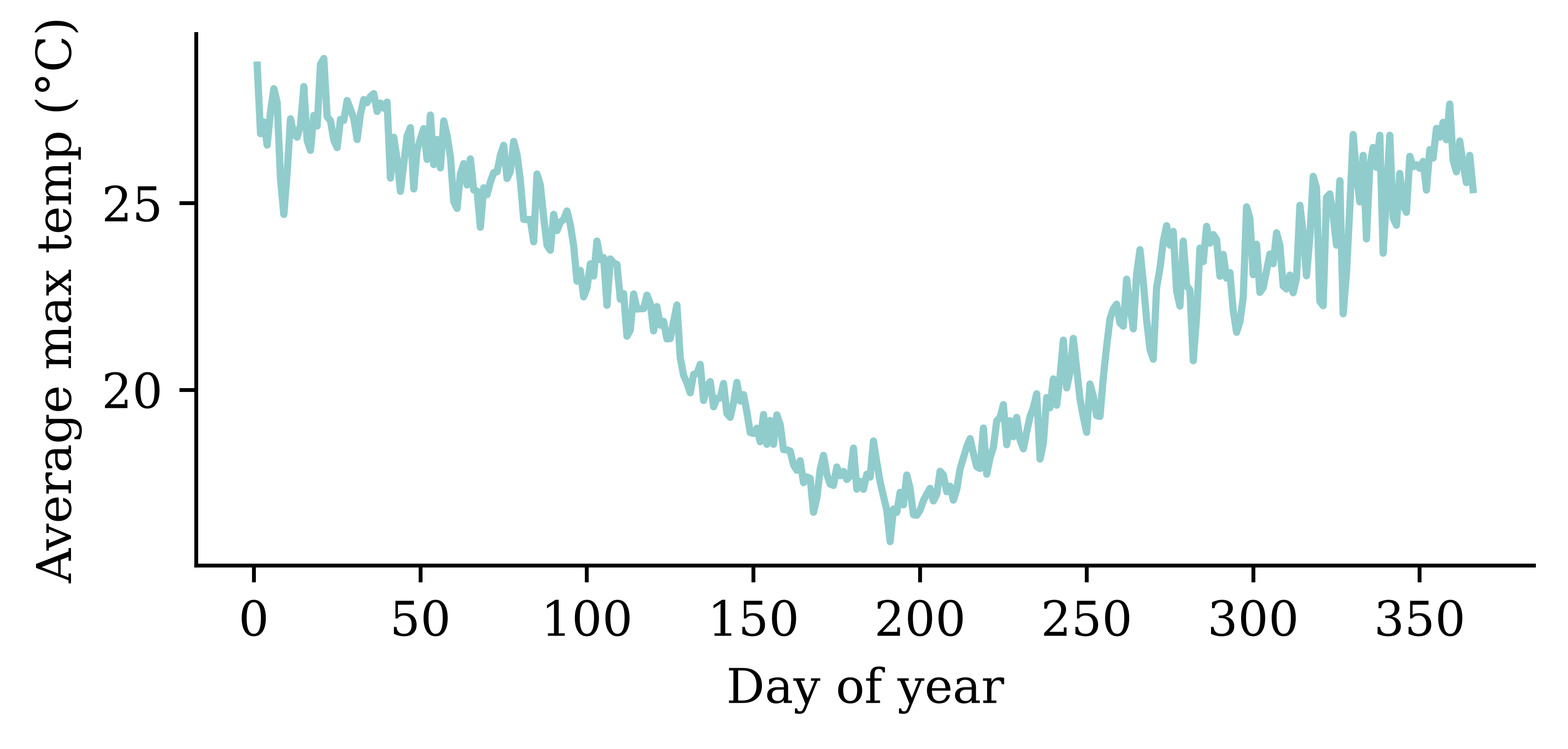

Plot

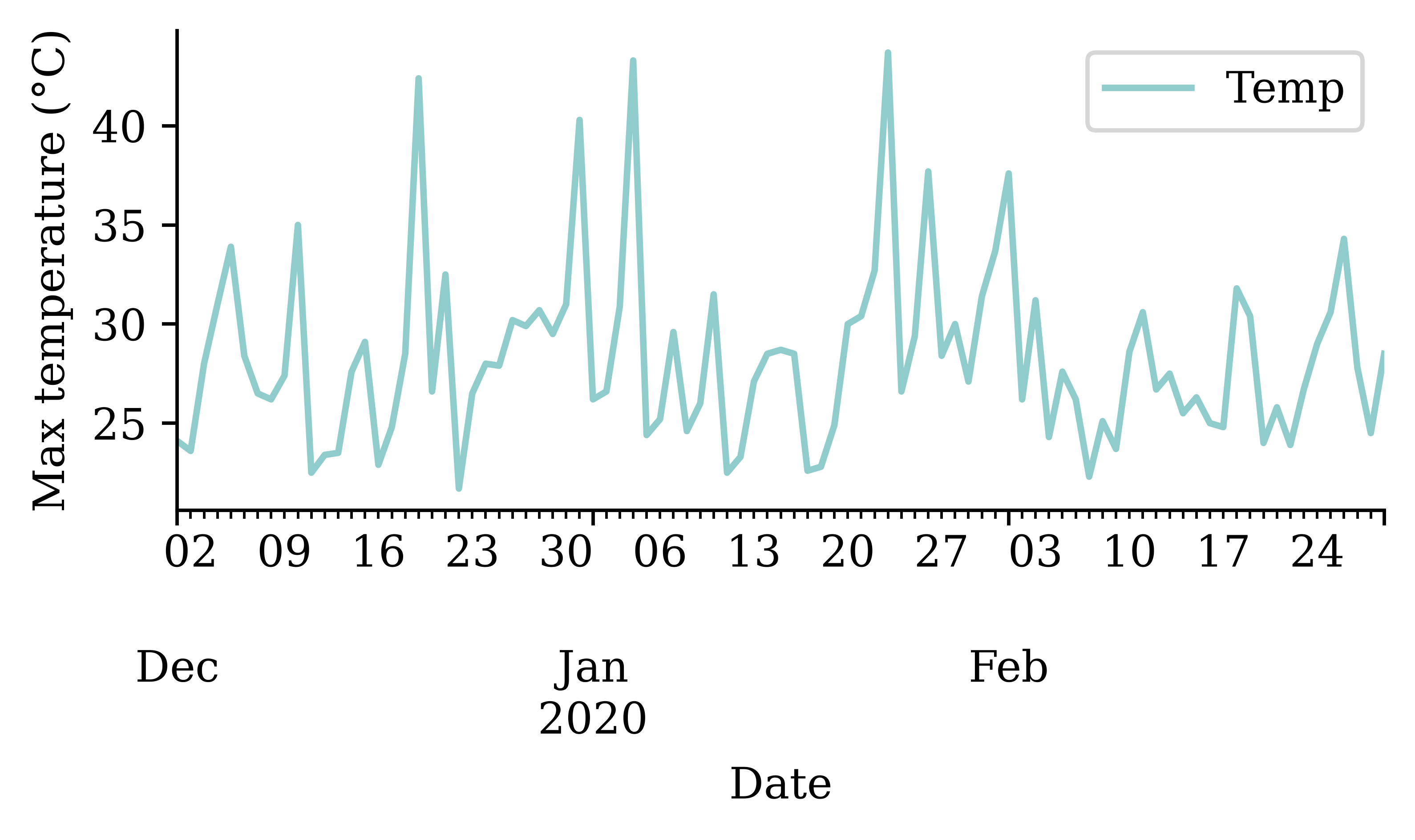

Zooming into one summer

Splitting in time

Code

import matplotlib.dates as mdates

fig, ax = plt.subplots(figsize=(6, 2.6))

for label, lo, hi in [("Train", None, temp_train_end), ("Val", temp_val_start, temp_val_end), ("Test", temp_test_start, None)]:

ax.plot(temps["Temp"].loc[lo:hi].index, temps["Temp"].loc[lo:hi], label=label)

ax.set_ylabel("Max temp (°C)")

ax.xaxis.set_major_locator(mdates.YearLocator(5))

ax.xaxis.set_major_formatter(mdates.DateFormatter("%Y"))

ax.legend(loc="upper left", fontsize=7);

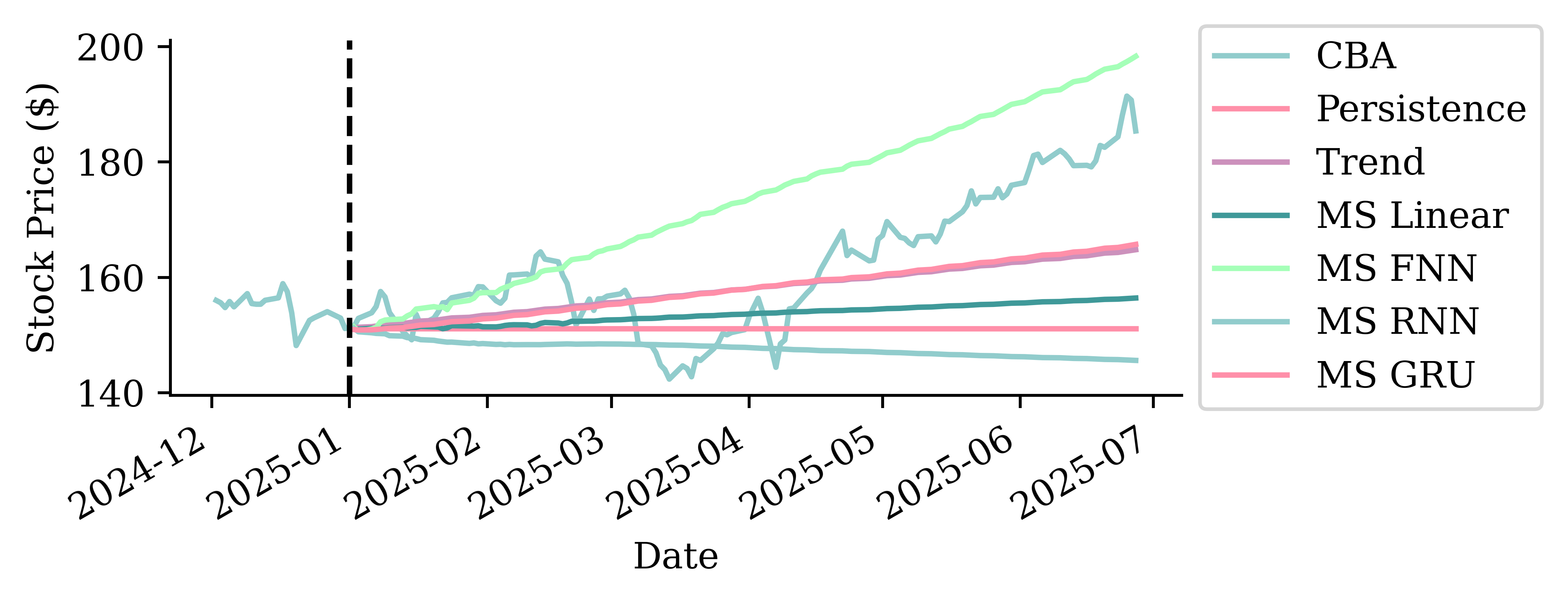

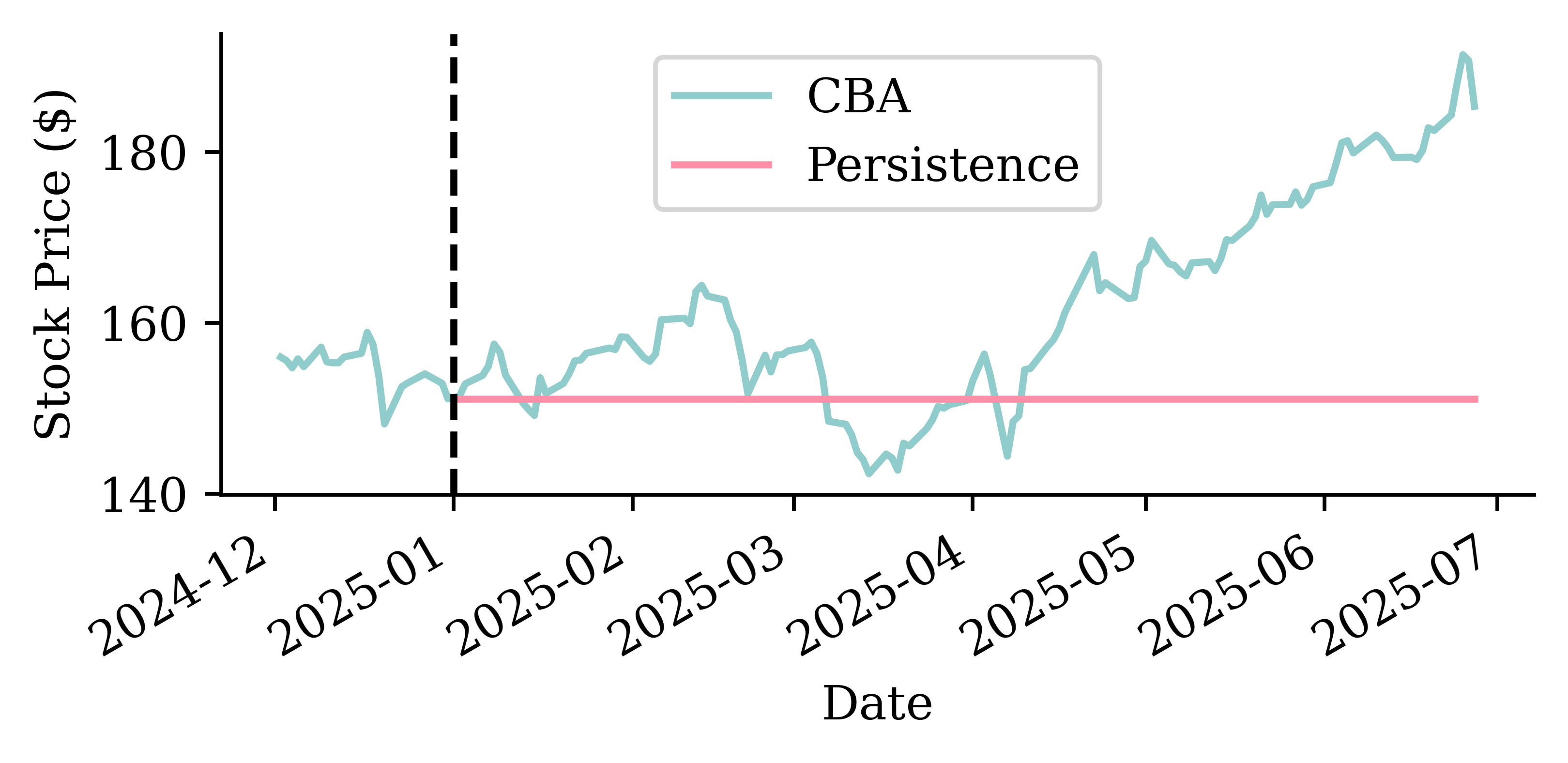

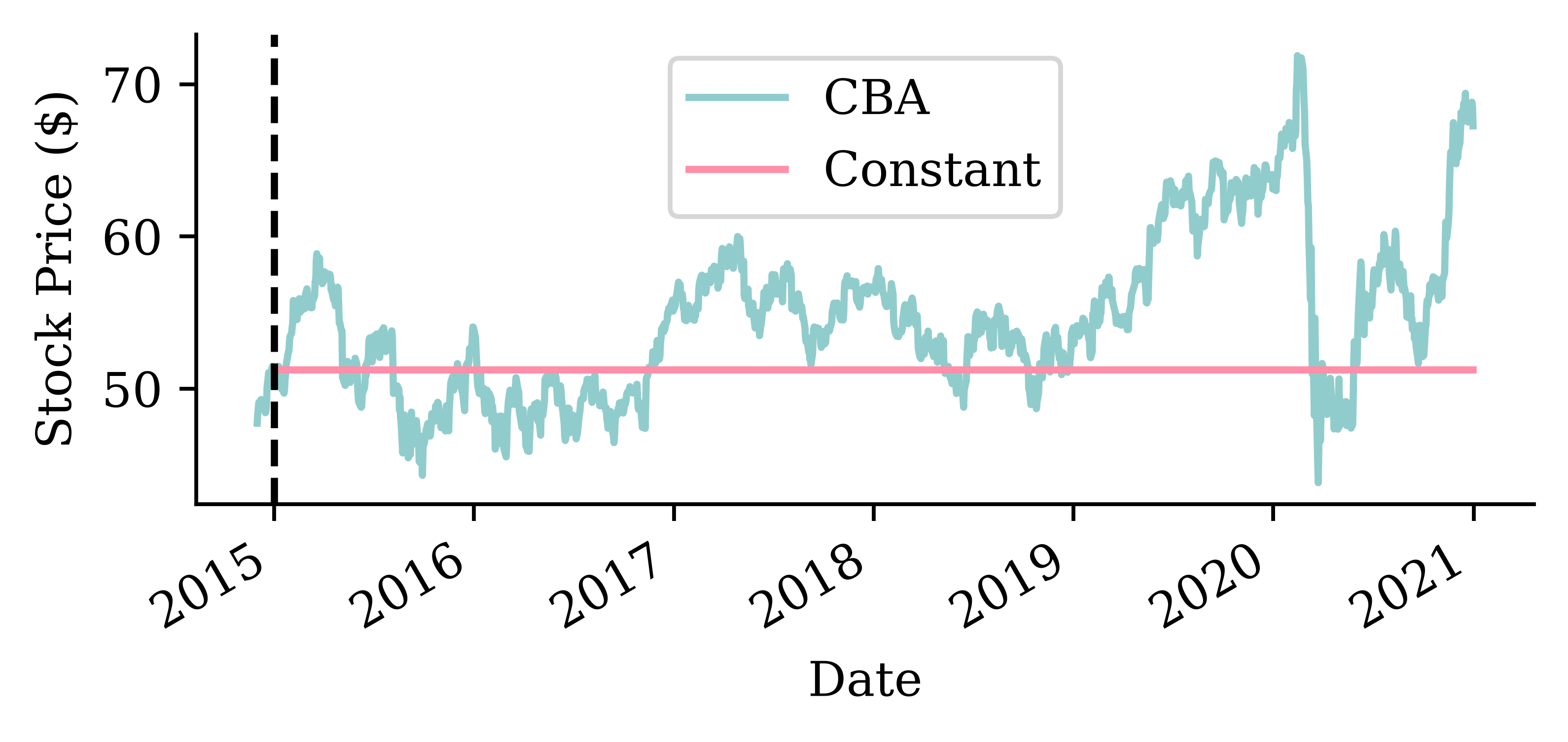

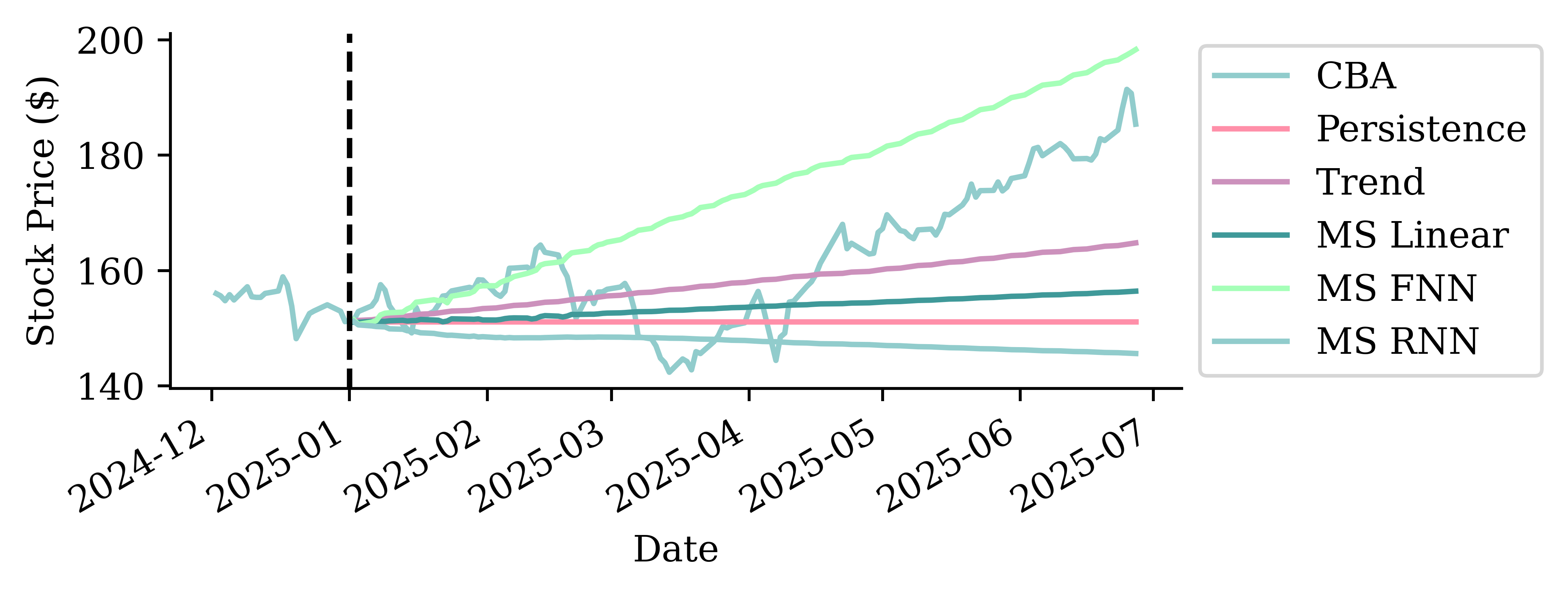

Constant forecast

The whole validation period is held constant at the last price we saw just before it. This is the multi-step naïve forecast (zero log returns from the origin onward).

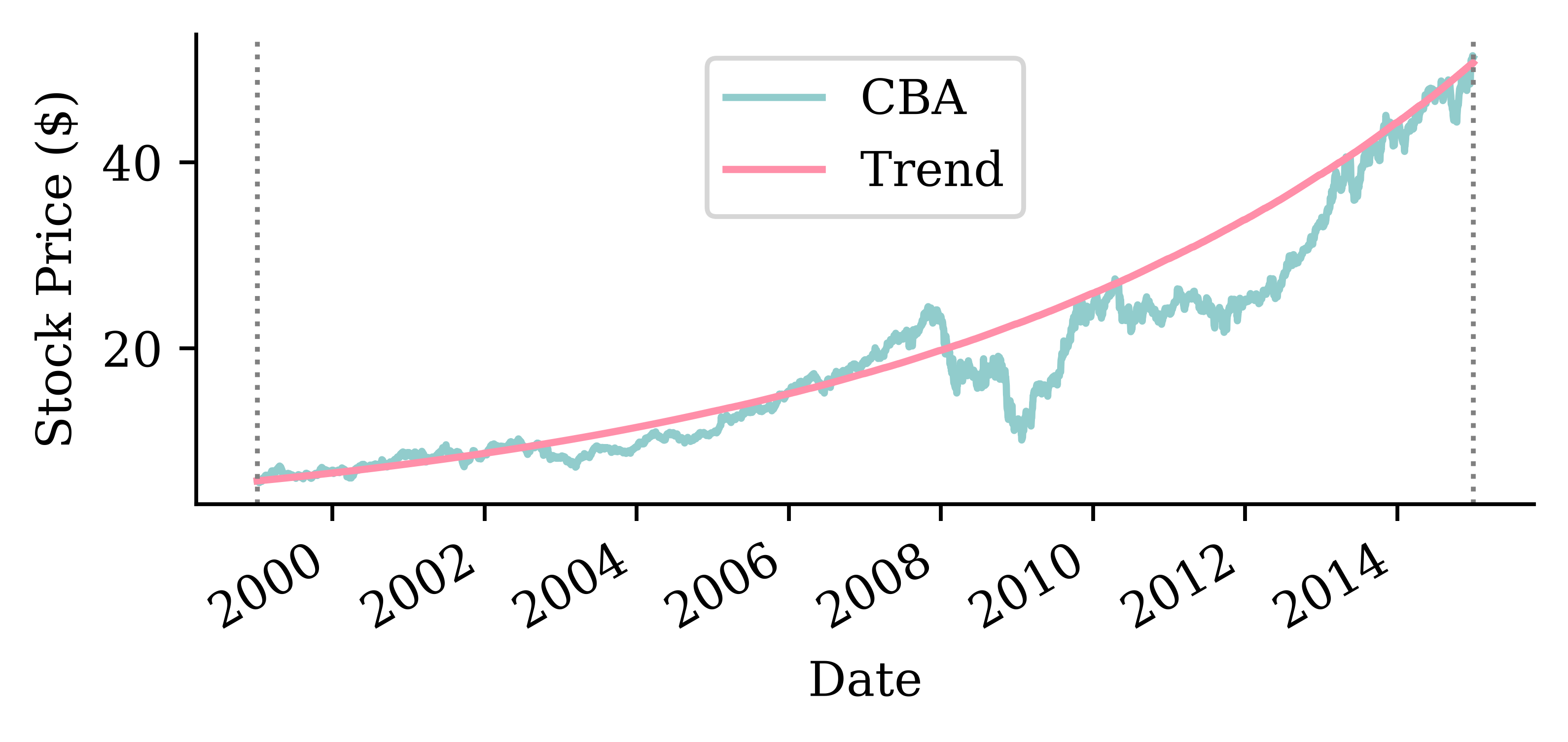

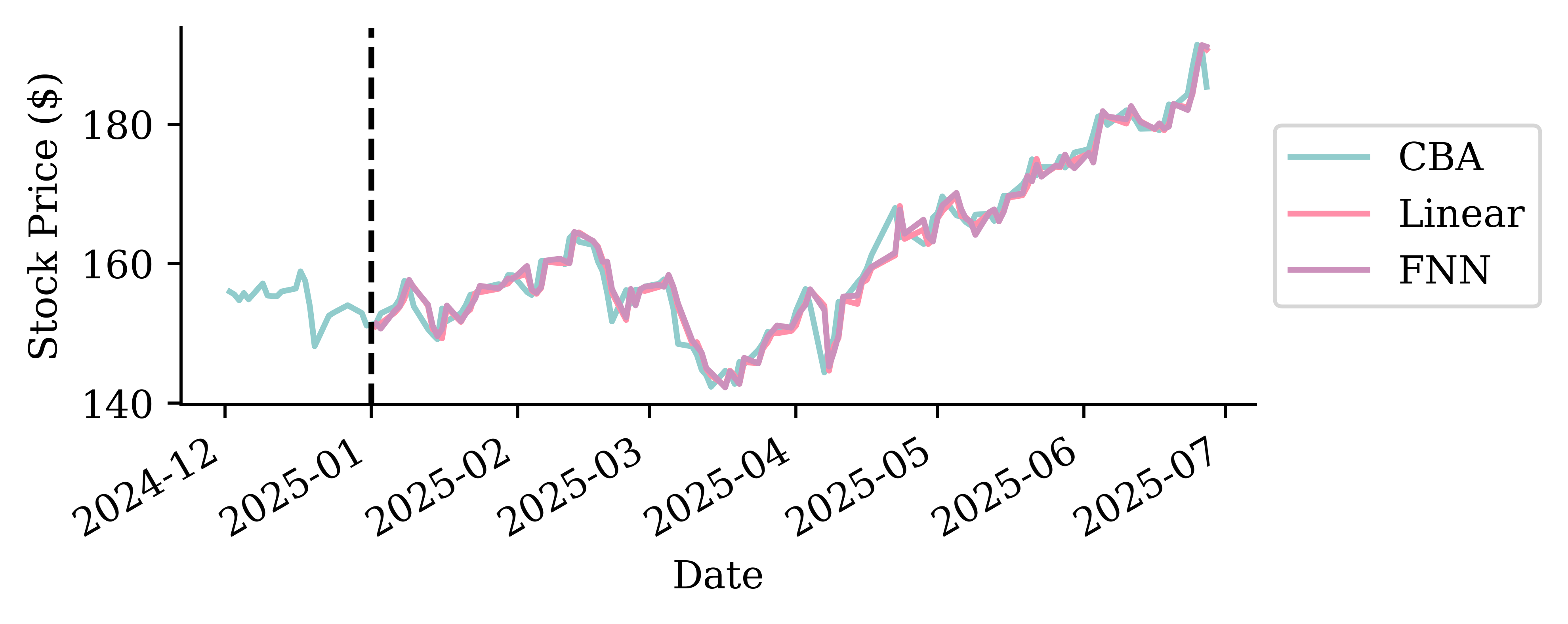

Extrapolate the trend

Average daily log return: 0.000532

Trend fitted

# Create trend forecast over the training period to show the fitted trend

train_trend_log = pd.Series(trend_log, index=train_log_returns.index)

trend_start_price = get_last_price(stock, cutoff_date=train_log_returns.index[0].strftime('%Y-%m-%d'))

train_trend_prices = log_to_price(train_trend_log, trend_start_price)Code

stock.loc[train_log_returns.index, ["CBA"]].plot(label="CBA")

train_trend_prices.plot(label="Trend")

plt.axvline(train_log_returns.index[0], color="gray", linestyle=":", linewidth=1)

plt.axvline(train_log_returns.index[-1], color="gray", linestyle=":", linewidth=1)

plt.ylabel("Stock Price ($)")

plt.legend();

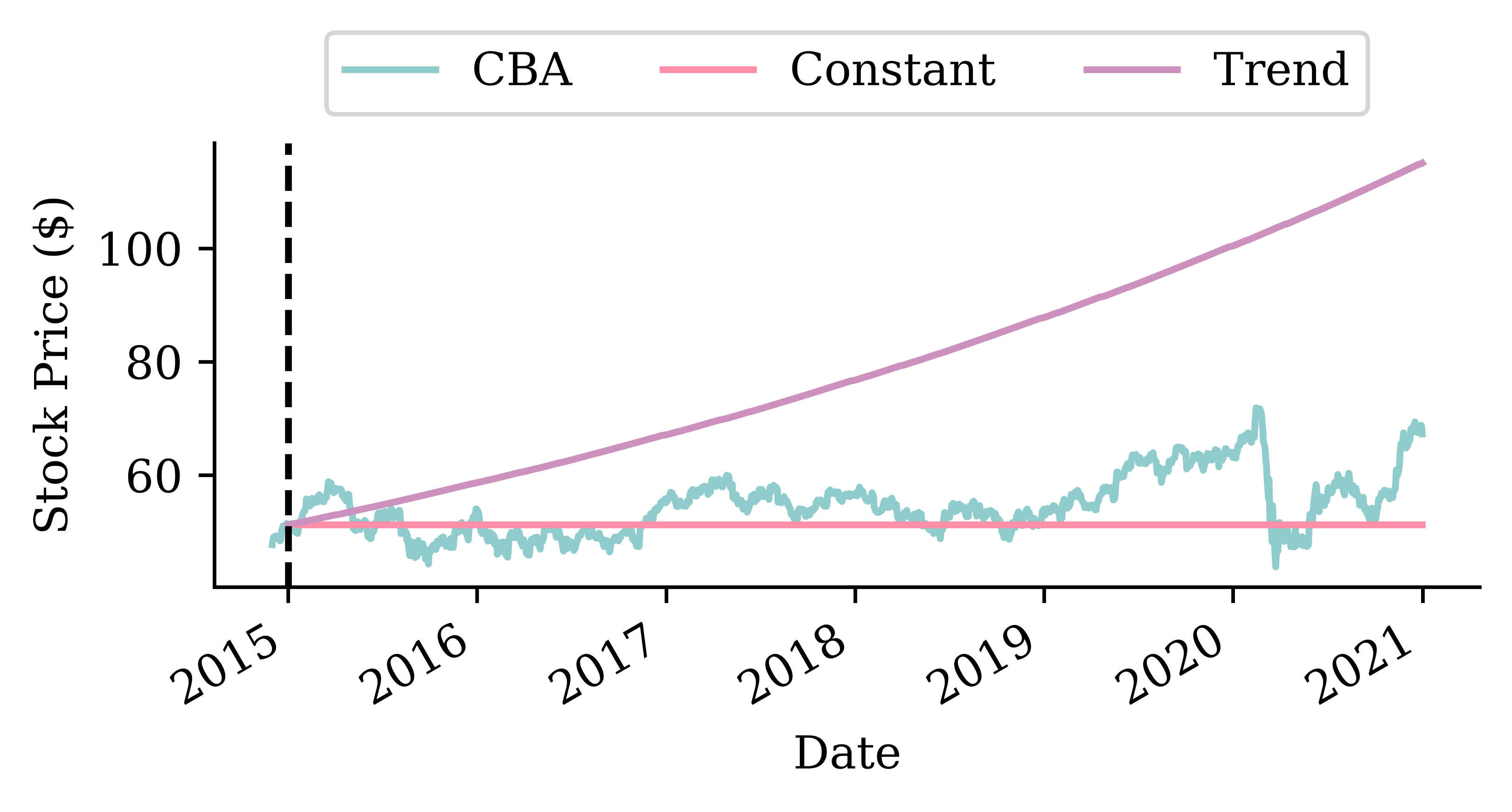

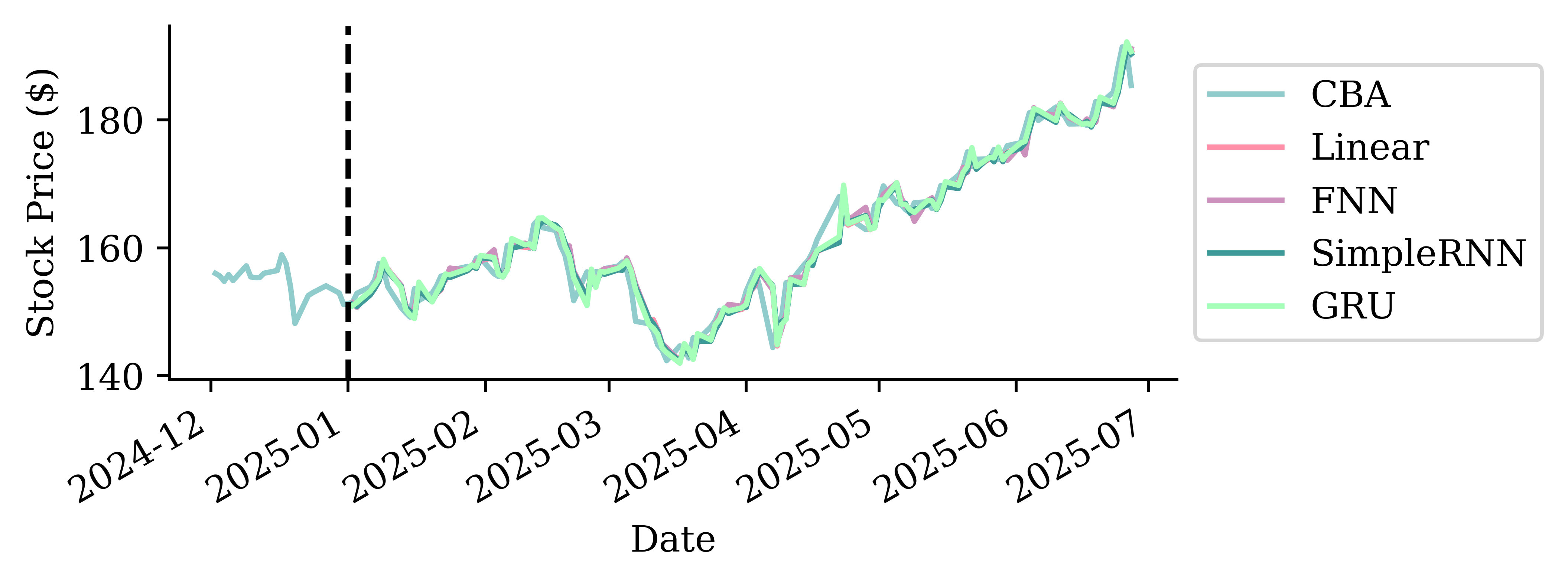

Trend forecasts

Code

stock.loc[start:end, ["CBA"]].plot(label="CBA")

constant_prices.loc[start:end].plot(label="Constant")

trend_prices.loc[start:end].plot(label="Trend")

plt.axvline(f"{cba_val_start}-01", color="black", linestyle="--")

plt.ylabel("Stock Price ($)")

plt.legend(ncol=3, loc="upper center", bbox_to_anchor=(0.5, 1.3));

Persistence forecast (one-step)

Now two baselines for the temperature series. First, persistence: predict tomorrow’s maximum temperature to be the same as today’s, \hat{y}_t = y_{t-1}.

Code

ax = temps.loc[f"{temp_test_start}-01":f"{temp_test_start}-03", "Temp"].plot(label="Actual", x_compat=True)

persistence.loc[f"{temp_test_start}-01":f"{temp_test_start}-03"].plot(ax=ax, label="Persistence", x_compat=True)

ax.set_ylabel("Max temperature (°C)")

ax.xaxis.set_major_locator(mdates.MonthLocator())

ax.xaxis.set_major_formatter(mdates.DateFormatter("%b"))

ax.set_xlabel("")

ax.legend();

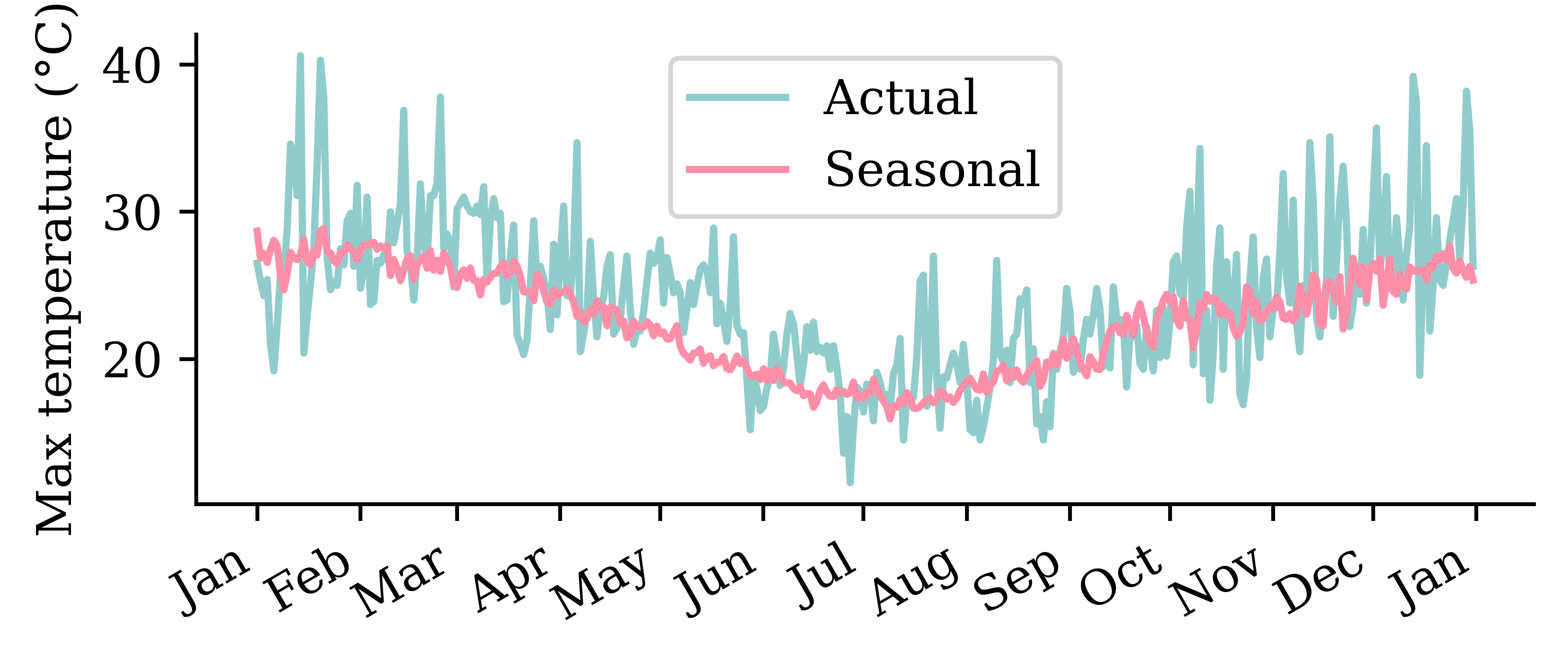

A seasonal baseline

A smarter baseline uses the seasonality: predict each day’s historical average over all years in the training period.

Seasonal forecast

Code

ax = temps.loc[temp_test_start, "Temp"].plot(label="Actual", x_compat=True)

seasonal.loc[temp_test_start].plot(ax=ax, label="Seasonal", x_compat=True)

ax.set_ylabel("Max temperature (°C)")

ax.xaxis.set_major_locator(mdates.MonthLocator())

ax.xaxis.set_major_formatter(mdates.DateFormatter("%b"))

ax.set_xlabel("")

ax.legend();

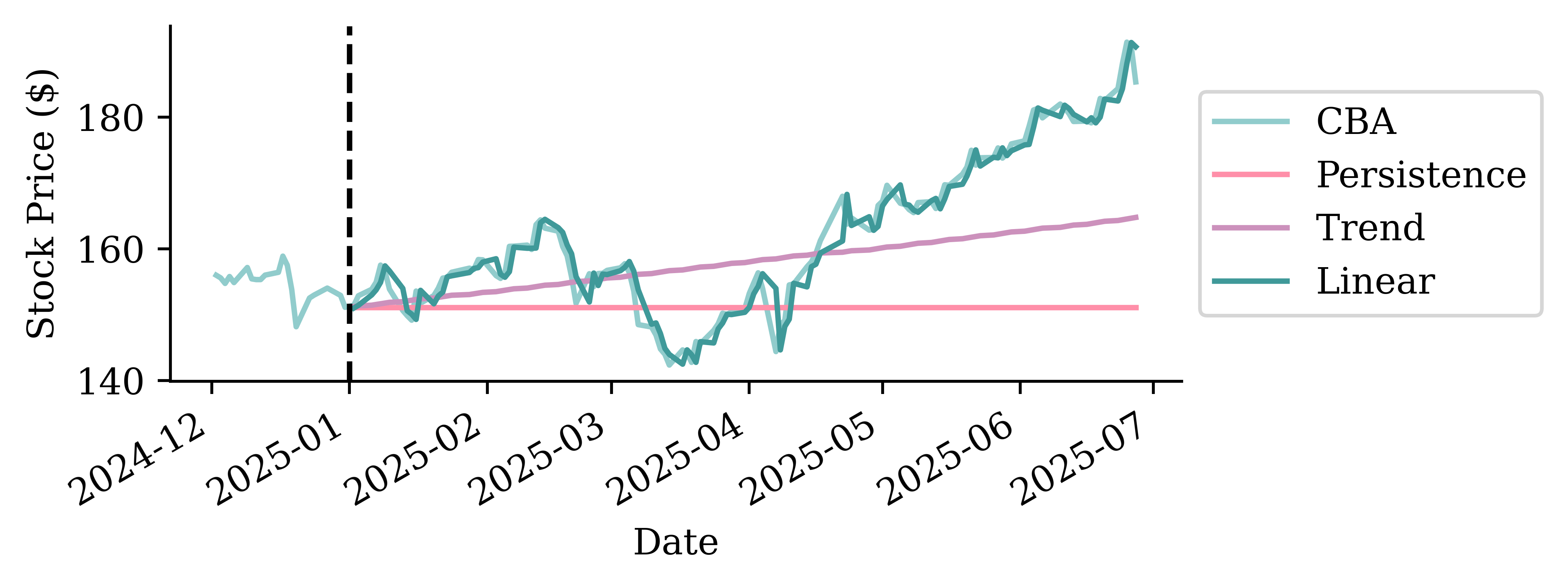

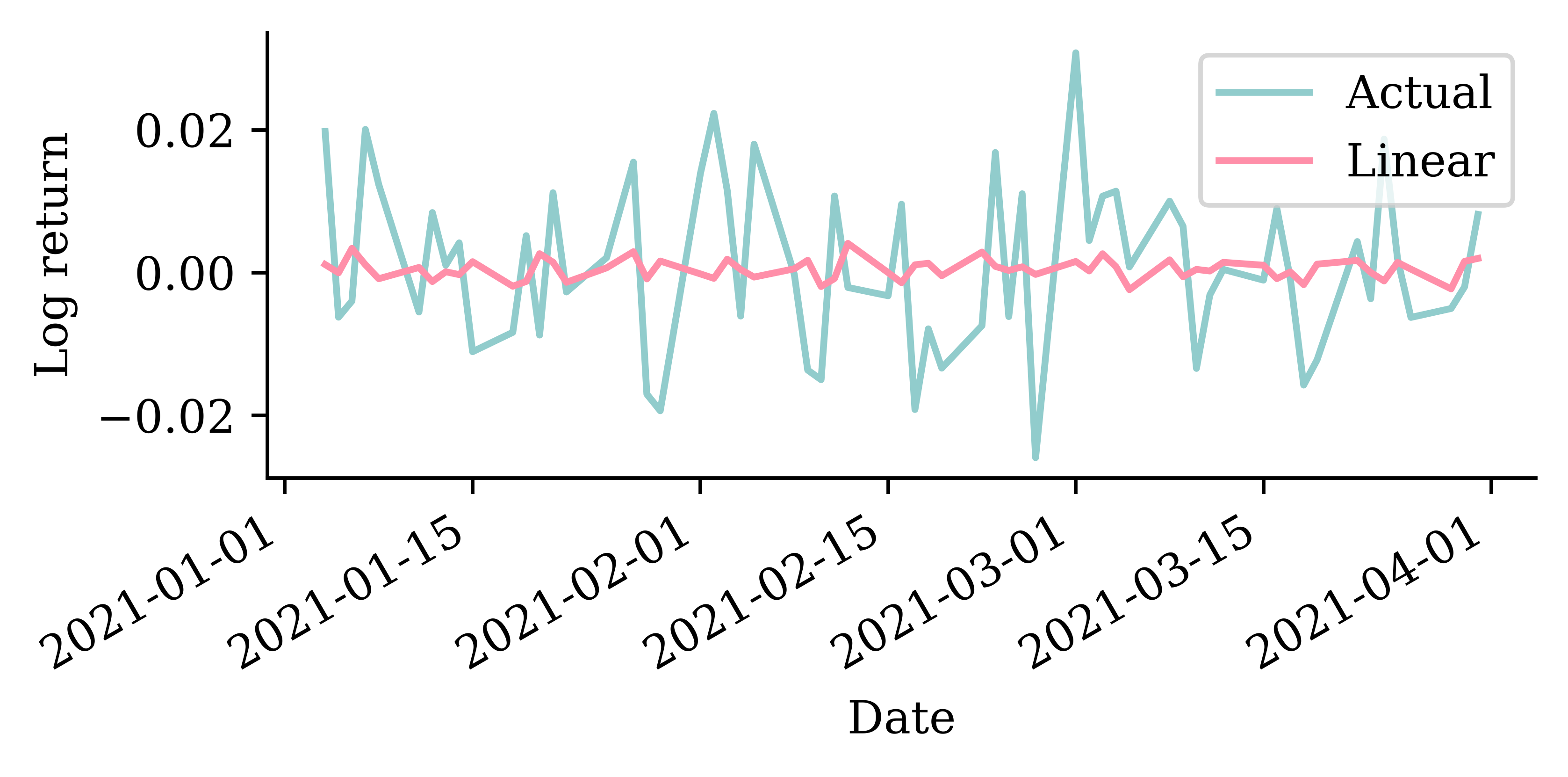

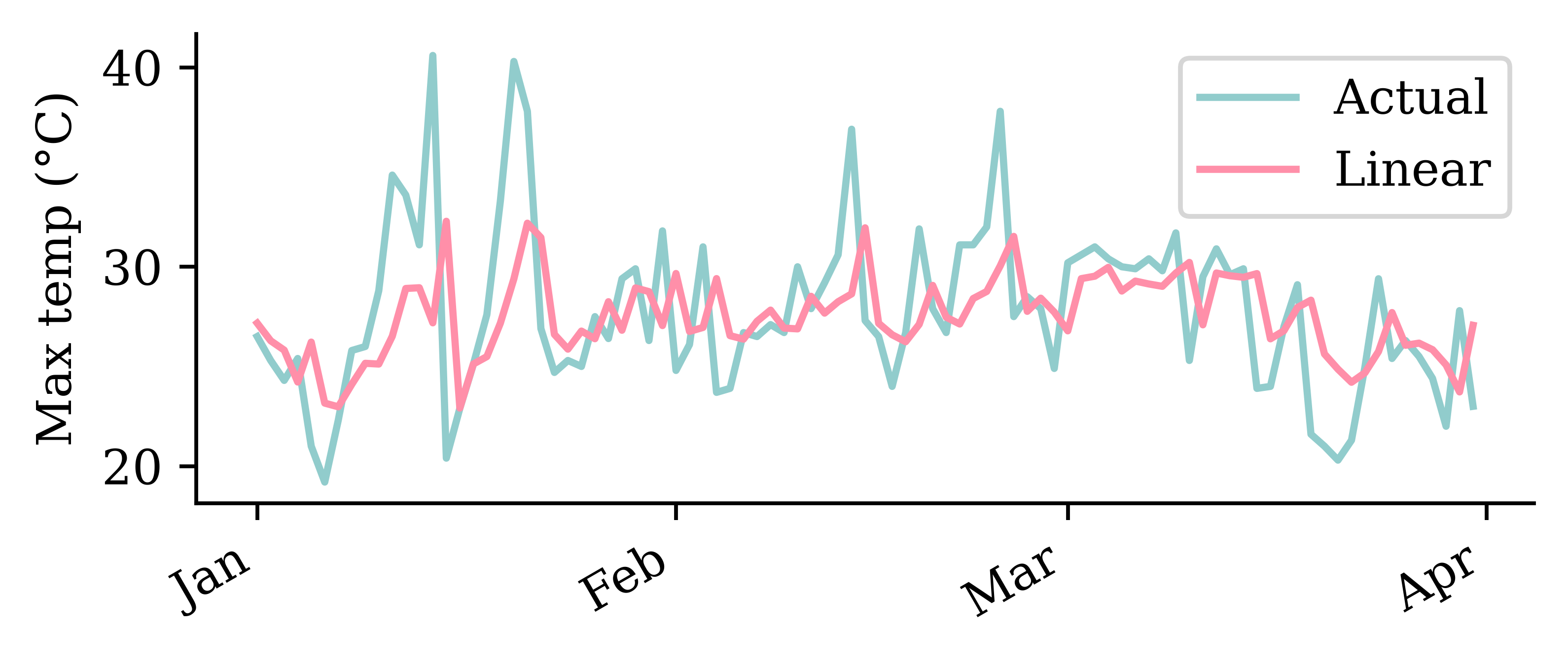

A linear model

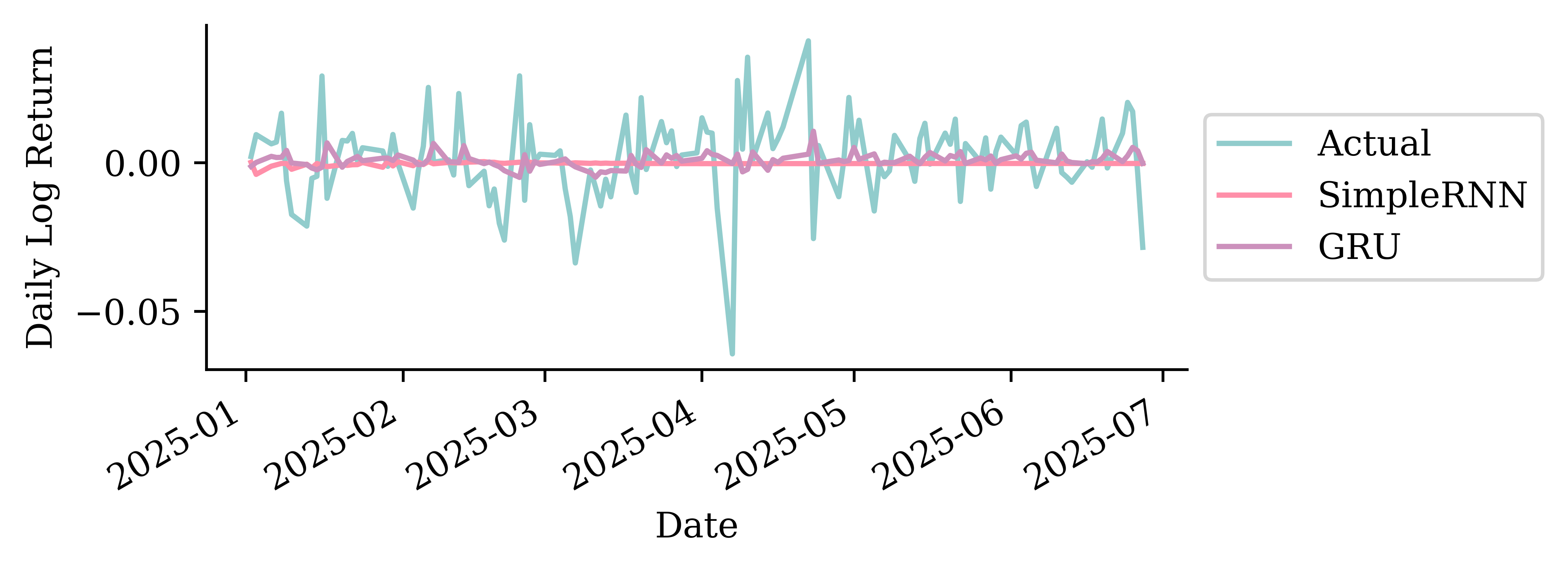

CBA log-return forecasts (Q1 of test set)

Temperature forecasts (Q1 of test set)

Code

ax = pd.DataFrame({"Actual": y_test_temp, "Linear": y_pred_temp}, index=y_test_temp.index).loc[f"{temp_test_start}-01":f"{temp_test_start}-03"].plot(x_compat=True)

ax.set_ylabel("Max temp (°C)")

ax.set_xlabel("")

ax.xaxis.set_major_locator(mdates.MonthLocator())

ax.xaxis.set_major_formatter(mdates.DateFormatter("%b"))

ax.legend();

A feedforward network

Same architecture for both; only the input rescaling differs: temperatures are divided by 40 (their rough maximum), log returns by their training-set standard deviation (finance_scale ≈ 0.014).

scale = 1 / finance_scale # for weather: 1/40

model = Sequential([Rescaling(scale), Dense(32, activation="leaky_relu"), Dense(1)])

model.compile(optimizer="adam", loss="mean_absolute_error")

model.fit(X_train_cba, y_train_cba, validation_data=(X_val_cba, y_val_cba), epochs=500,

callbacks=[EarlyStopping(patience=15, restore_best_weights=True)], verbose=0)CBA log-return forecasts (Q1 of test set)

Temperature forecasts (Q1 of test set)

Code

ax = pd.DataFrame({"Actual": y_test_temp, "FNN": y_pred_temp}, index=y_test_temp.index).loc[f"{temp_test_start}-01":f"{temp_test_start}-03"].plot(x_compat=True)

ax.set_ylabel("Max temp (°C)")

ax.xaxis.set_major_locator(mdates.MonthLocator())

ax.xaxis.set_major_formatter(mdates.DateFormatter("%b %Y"))

ax.set_xlabel("")

ax.legend();

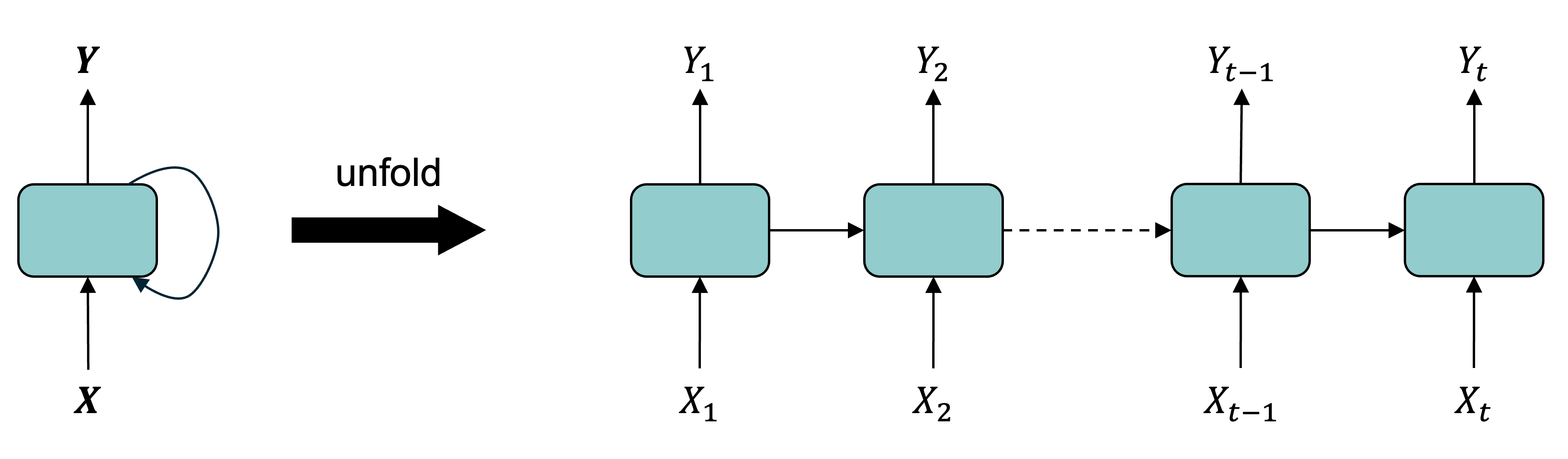

Diagram of an RNN cell

The RNN processes each data point in the sequence one by one, while keeping memory of what came before.

Schematic of a recurrent neural network. E.g. SimpleRNN, LSTM, or GRU.

Intuition/demo: Fizz Buzz

Play Fizz Buzz: count up, but say “Fizz” on multiples of 3, “Buzz” on multiples of 5, and “Fizz Buzz” on multiples of both.

A vector-to-sequence RNN playing Fizz Buzz: one START input, the running count is the hidden state passed to the right, the spoken word is the output at each step.

Each player only needs the count from their neighbour (the hidden state) to know what to say and what to pass on — no separate input per step.

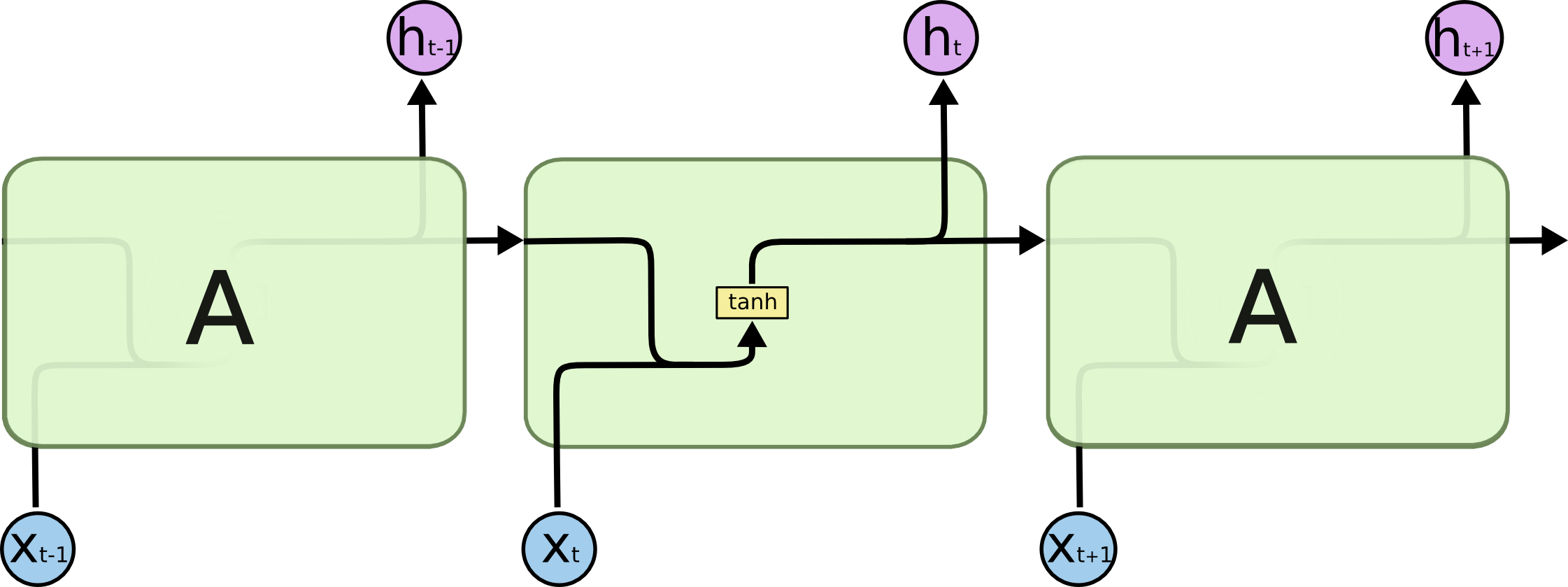

A SimpleRNN cell

Diagram of a SimpleRNN cell.

All the outputs before the final one are often discarded.

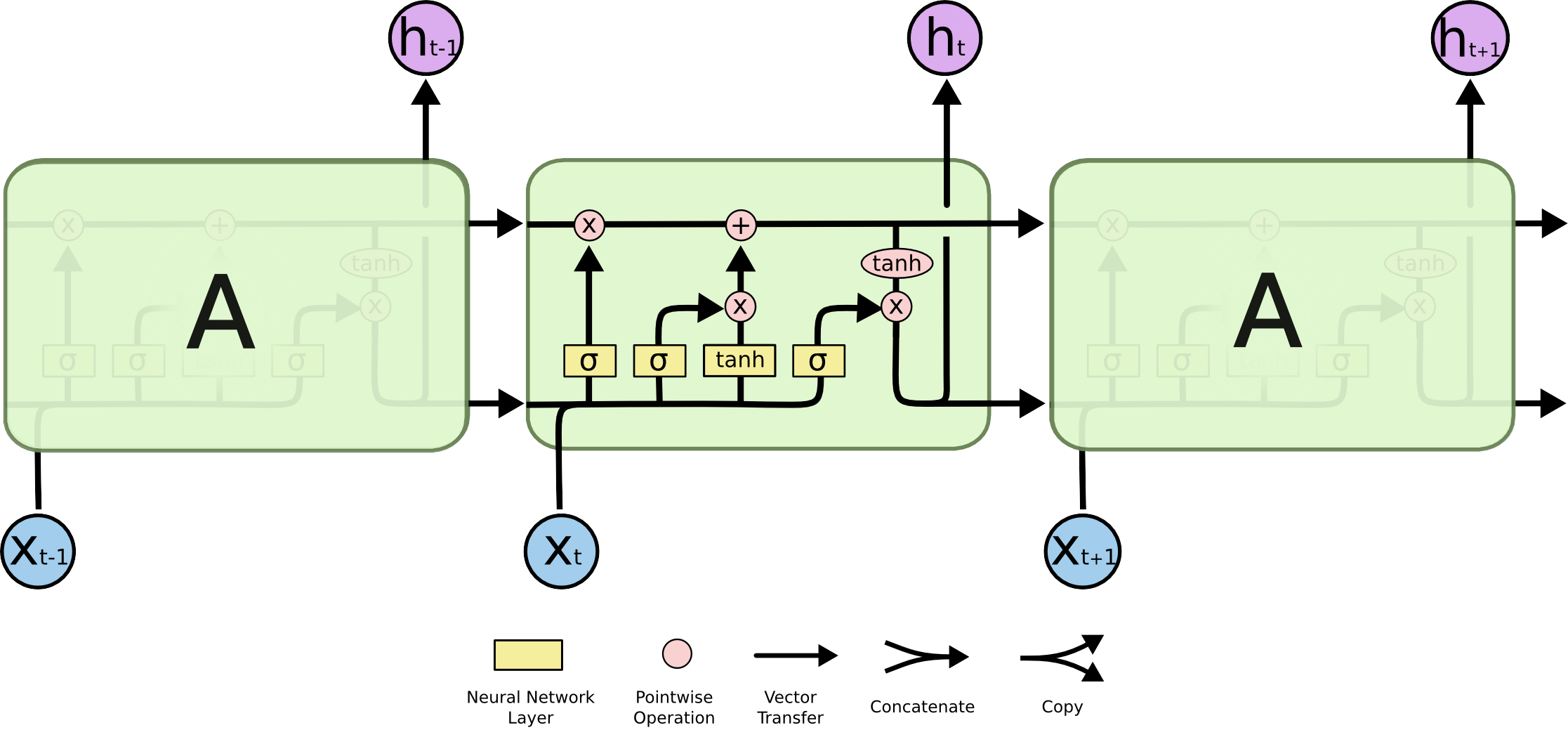

Long short-term memory (LSTM)

Diagram of an LSTM cell.

Gated Recurrent Unit (GRU)

Diagram of a GRU cell.

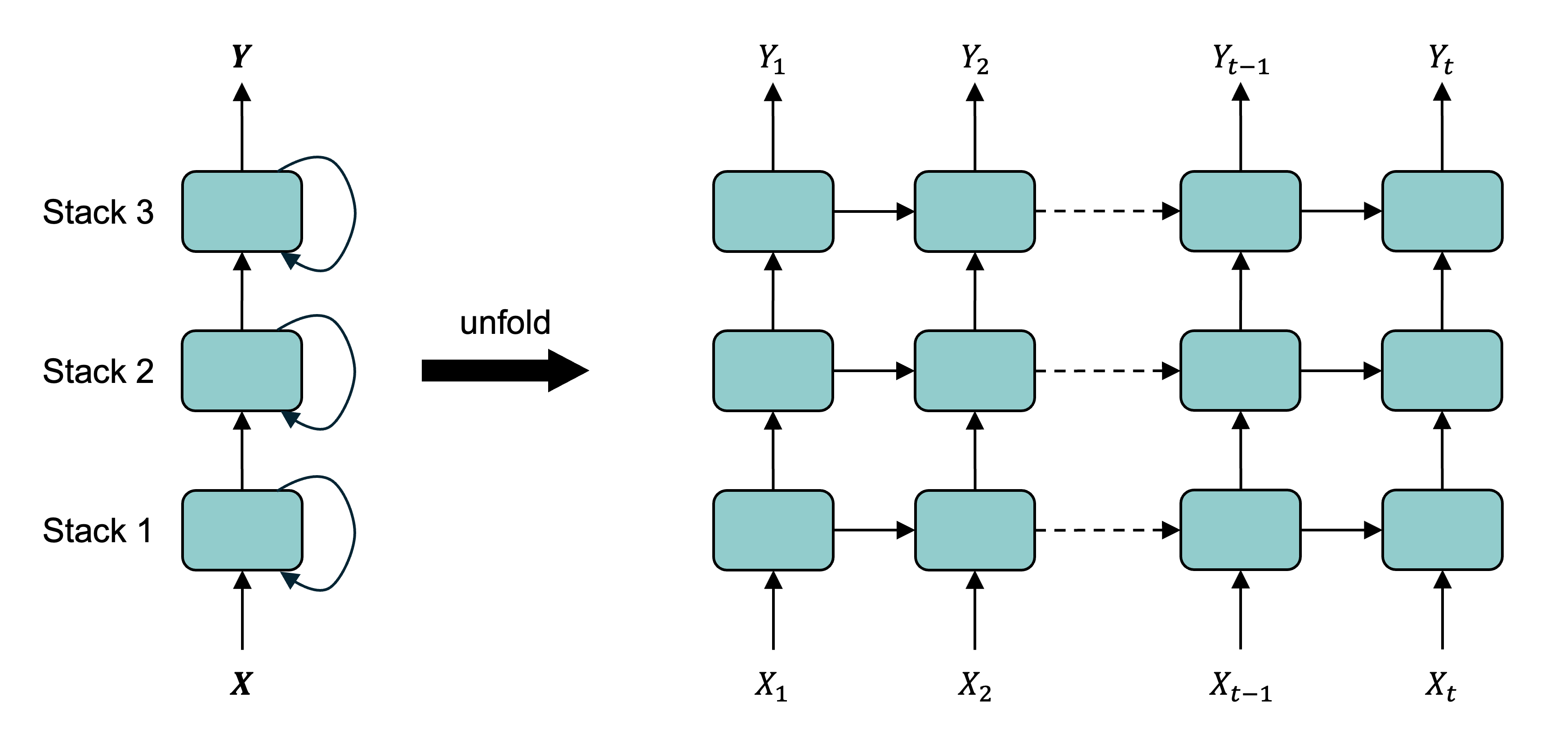

Recurrent layers can be stacked

Deep RNN unrolled through time.

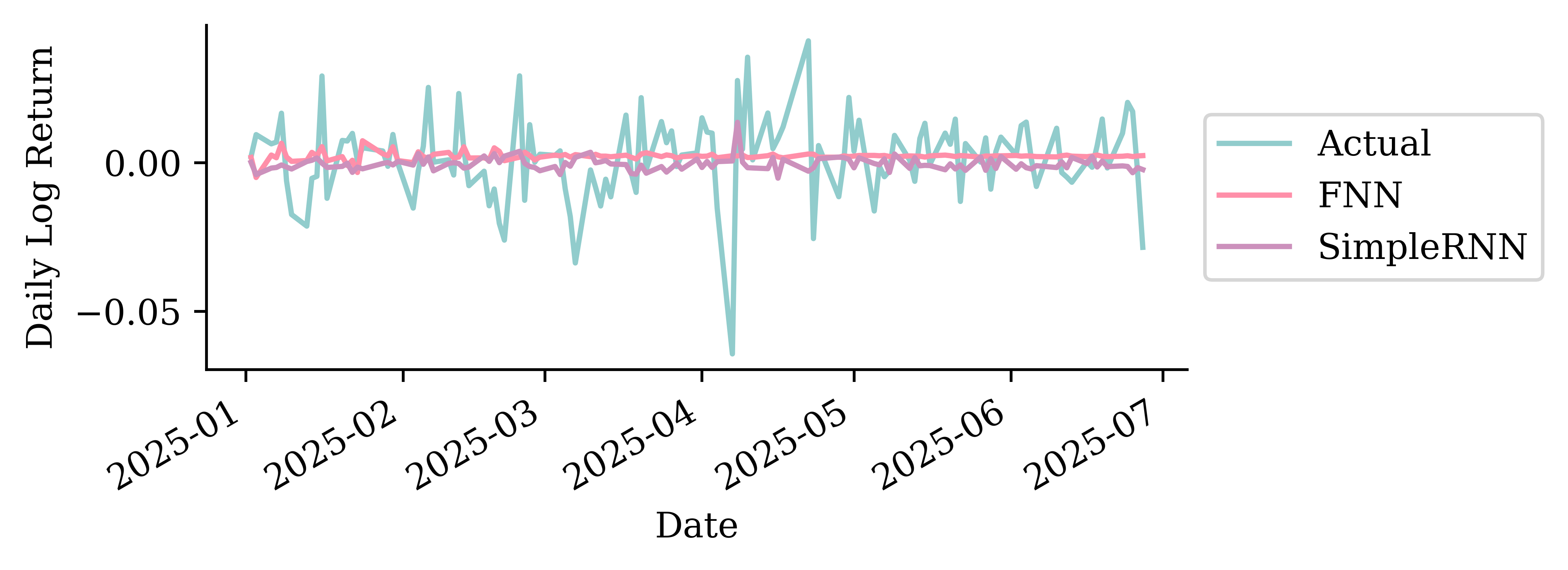

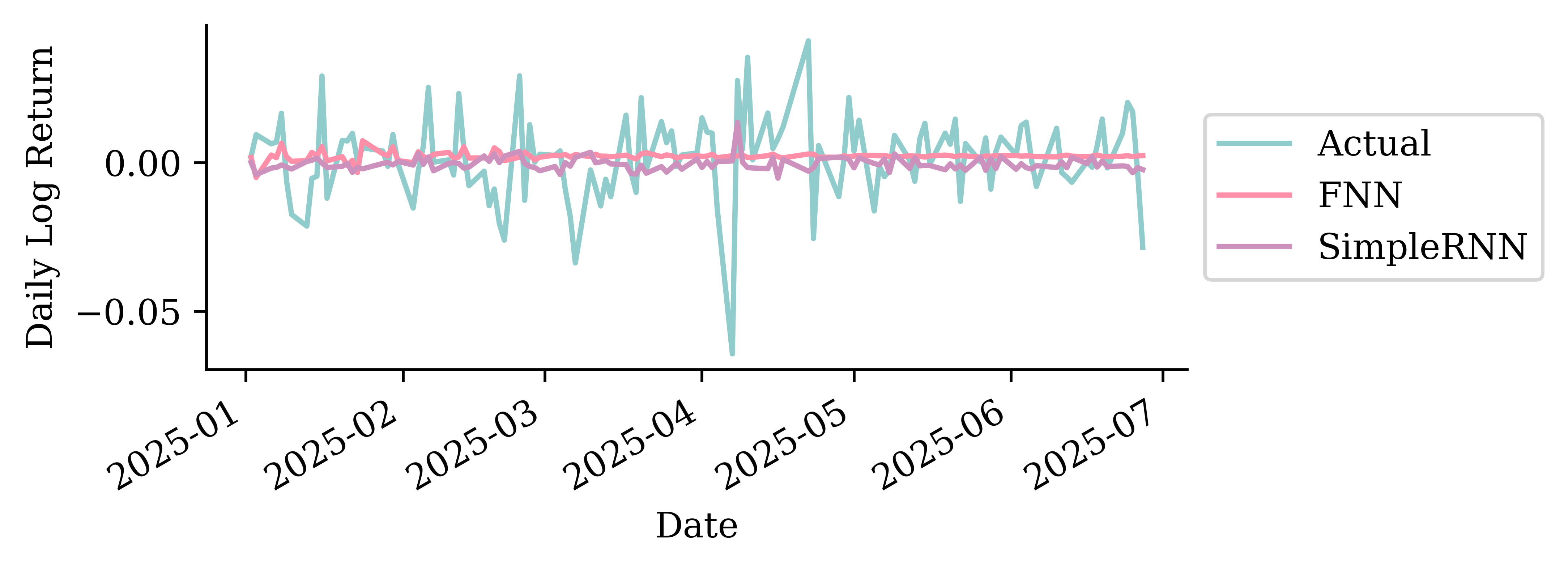

Fitting the SimpleRNN

scale = 1 / finance_scale # for weather: 1/40

model = Sequential([Rescaling(scale), Reshape((-1, 1)), SimpleRNN(64, activation="tanh"), Dense(1)])

model.compile(optimizer="adam", loss="mean_absolute_error")

model.fit(X_train_cba, y_train_cba, validation_data=(X_val_cba, y_val_cba), epochs=500,

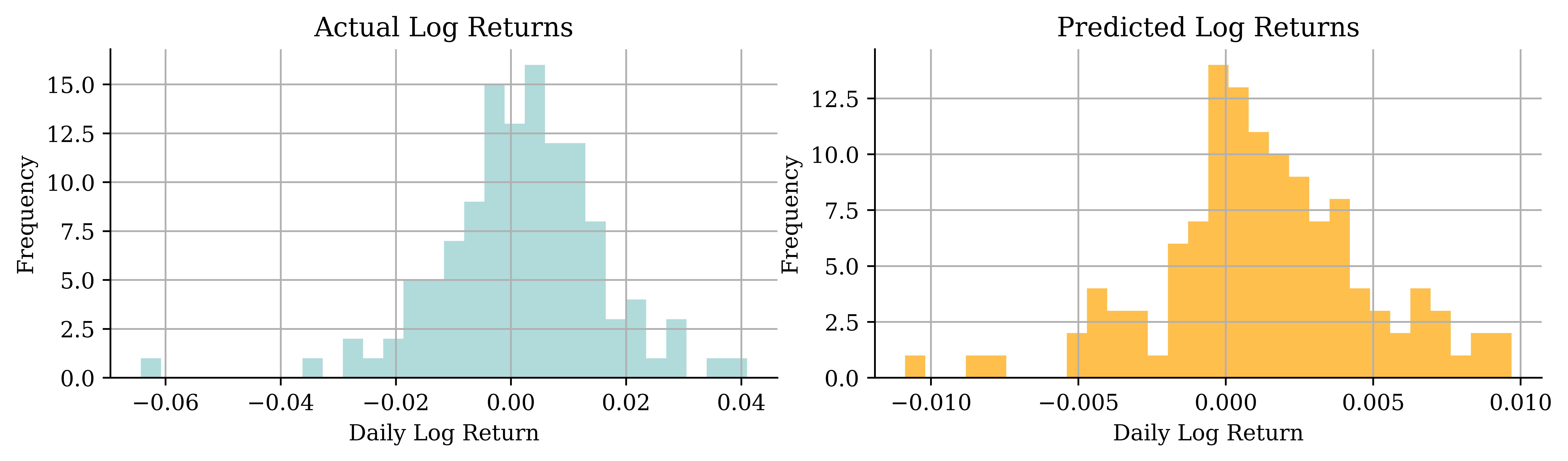

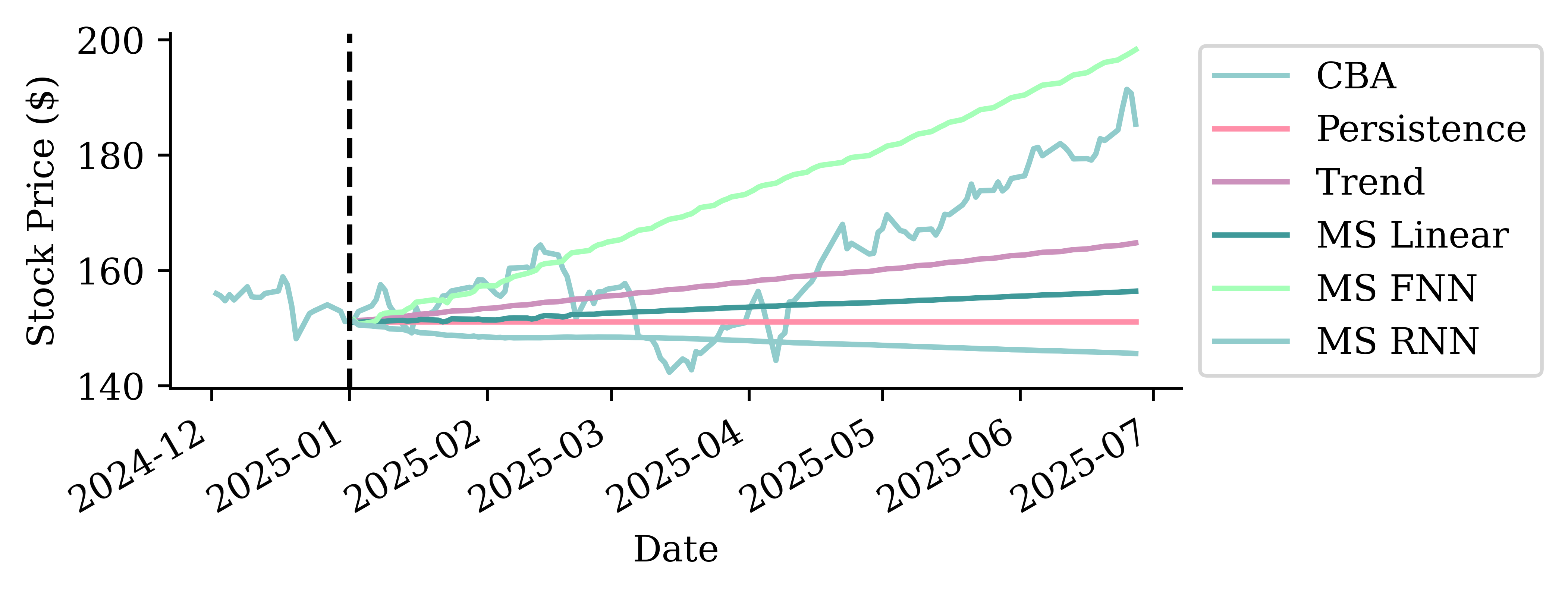

callbacks=[EarlyStopping(patience=15, restore_best_weights=True)], verbose=0)CBA stock price forecasts (test set)

Temperature forecasts (test set)

Code

ax = pd.DataFrame({"Actual": y_test_temp, "SimpleRNN": y_pred_temp}, index=y_test_temp.index).loc[f"{temp_test_start}-01":f"{temp_test_start}-03"].plot(x_compat=True)

ax.set_ylabel("Max temp (°C)")

ax.xaxis.set_major_locator(mdates.MonthLocator())

ax.xaxis.set_major_formatter(mdates.DateFormatter("%b %Y"))

ax.set_xlabel("")

ax.legend();

Fitting a GRU

scale = 1 / finance_scale # for weather: 1/40

model = Sequential([Rescaling(scale), Reshape((-1, 1)), GRU(16, activation="tanh"), Dense(1)])

model.compile(optimizer="adam", loss="mean_absolute_error")

model.fit(X_train_cba, y_train_cba, validation_data=(X_val_cba, y_val_cba), epochs=500,

callbacks=[EarlyStopping(patience=15, restore_best_weights=True)], verbose=0)CBA stock price forecasts (test set)

Temperature forecasts (test set)

Code

ax = pd.DataFrame({"Actual": y_test_temp, "GRU": y_pred_temp}, index=y_test_temp.index).loc[f"{temp_test_start}-01":f"{temp_test_start}-03"].plot(x_compat=True)

ax.set_ylabel("Max temp (°C)")

ax.xaxis.set_major_locator(mdates.MonthLocator())

ax.xaxis.set_major_formatter(mdates.DateFormatter("%b %Y"))

ax.set_xlabel("")

ax.legend();

Forecasting a few weeks ahead

Start the model with the last 40 real days, then forecast the next four weeks. Over a short horizon the errors may be small enough.

Code

horizon = 28

seed = X_test_temp.iloc[0].to_numpy()

short = pd.Series(autoregressive_forecast(fnn_w, seed, horizon),

index=y_test_temp.index[:horizon])

y_test_temp.iloc[:horizon].plot(label="Actual", marker=".", x_compat=True)

short.plot(label="Recursive FNN", marker=".", color="#CC91BC", x_compat=True)

plt.ylabel("Max temp (°C)")

ax = plt.gca()

ax.xaxis.set_major_locator(mdates.DayLocator(interval=7))

ax.xaxis.set_major_formatter(mdates.DateFormatter("%b %d"))

plt.xlabel("")

plt.legend(loc="center left", bbox_to_anchor=(1, 0.5));

Forecasting a year ahead

Keep unrolling for the whole test period and the small errors compound. The forecast drifts off, loses the seasonal cycle, and settles on a flat plateau, much worse than the trivial baseline.

Code

long = pd.Series(autoregressive_forecast(fnn_w, X_test_temp.iloc[0].to_numpy(), len(y_test_temp)),

index=y_test_temp.index)

y_test_temp.plot(label="Actual")

seasonal.reindex(y_test_temp.index).plot(label="Seasonal baseline")

long.plot(label="Recursive FNN", color="#CC91BC")

plt.ylabel("Max temp (°C)")

plt.legend(loc="center left", bbox_to_anchor=(1, 0.5));

A multivariate example

Code

fig, axs = plt.subplots(2, 2, figsize=(5.5, 3.5), sharex=True)

for ax, s in zip(axs.flat, station_files):

actual_mt[s].loc[f"{temp_test_start}-01":f"{temp_test_start}-03"].plot(ax=ax, label="Actual", x_compat=True)

pred_mt[s].loc[f"{temp_test_start}-01":f"{temp_test_start}-03"].plot(ax=ax, label="GRU", x_compat=True)

ax.set_title(s, fontsize=9); ax.set_ylabel("Max temp (°C)"); ax.set_xlabel("")

axs[0, 0].legend(fontsize=7)

for ax in [axs[1, 0], axs[1, 1]]:

ax.xaxis.set_major_locator(mdates.MonthLocator())

ax.xaxis.set_major_formatter(mdates.DateFormatter("%b %Y"))

plt.tight_layout();