Distributional Regression

ACTL3143 & ACTL5111 Deep Learning for Actuaries

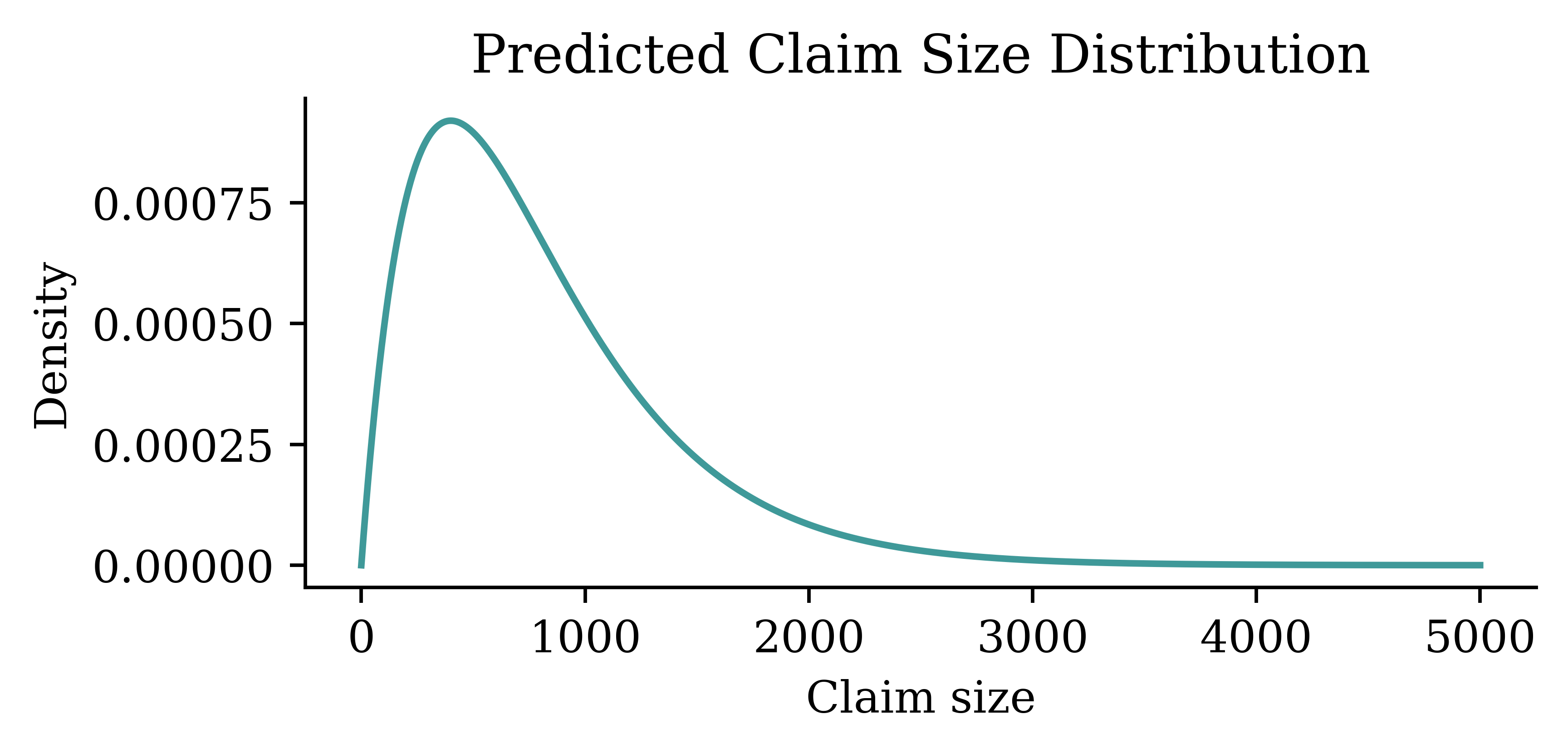

Distributional regression

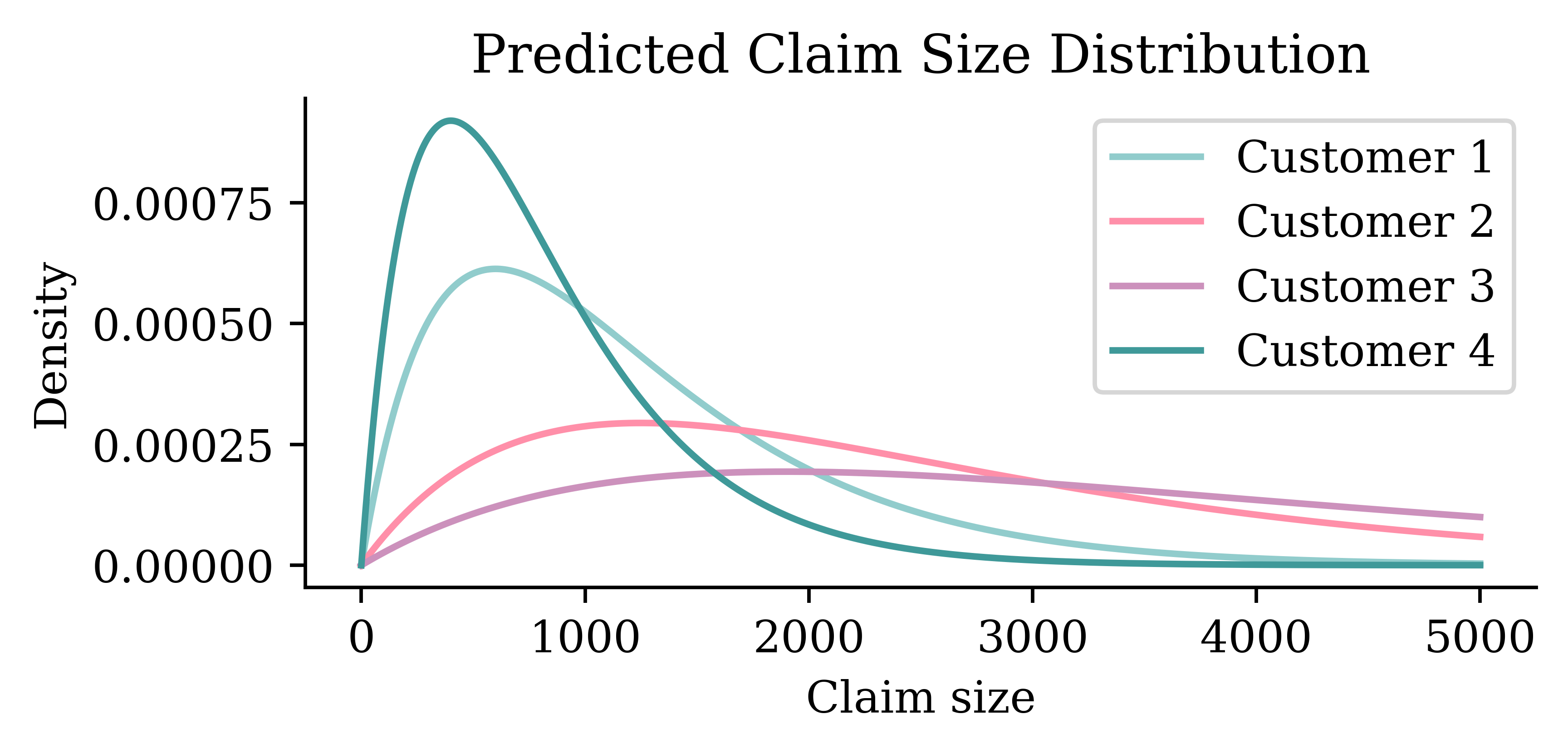

Customer 2 = (40, 5, 🚐)

Distributional regression

Customer 3 = (19, 1, 🏎️)

Distributional regression

Customer 4 = (60, 10, 🚘)

Distributional regression

All customers

One model, many distributions

Feed in a batch of customers and the model returns a predicted claim-size distribution for each one.

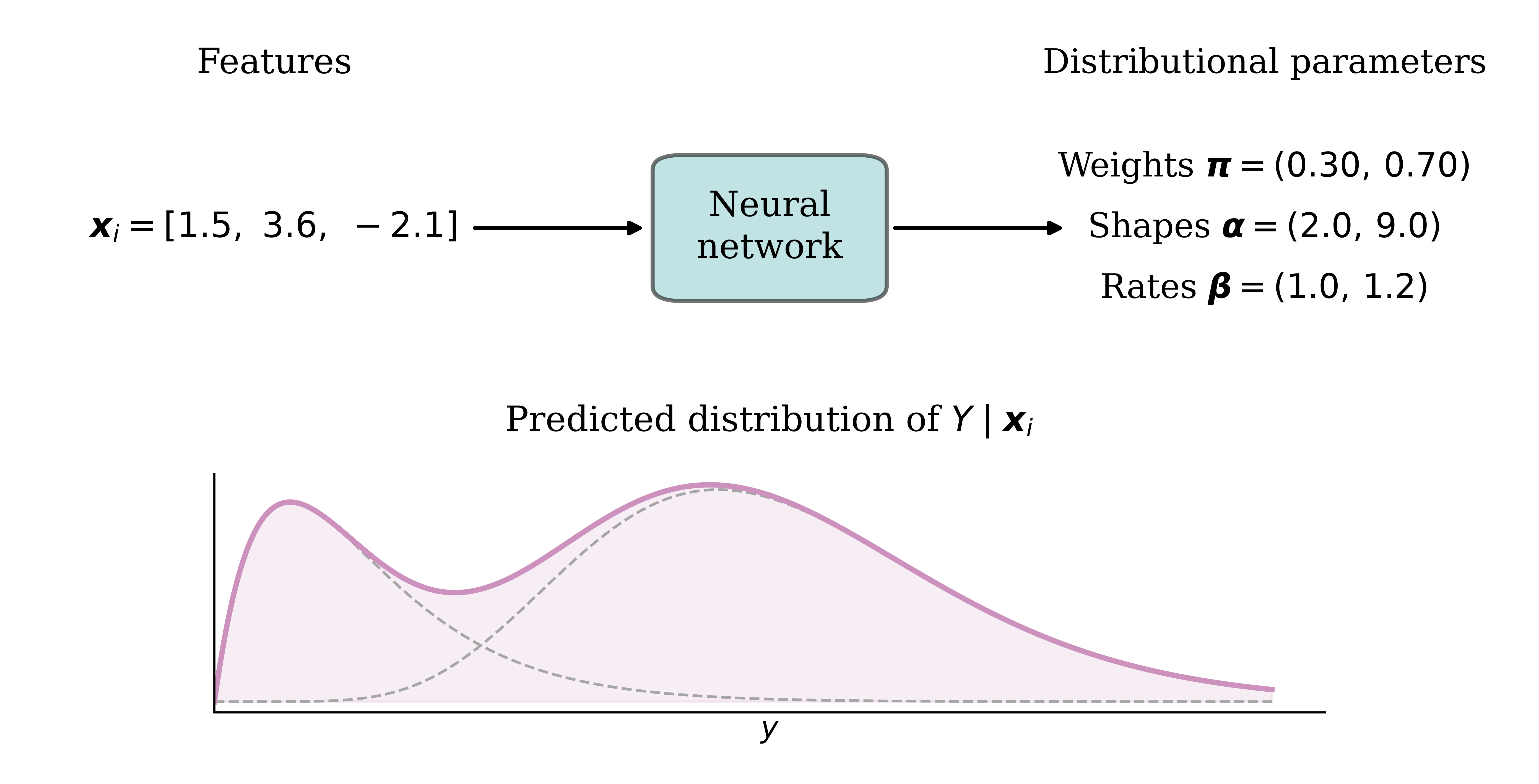

Predicting distribution parameters

In practice the network doesn’t emit a whole curve — it emits the parameters of a chosen distribution family, which then define the distribution.

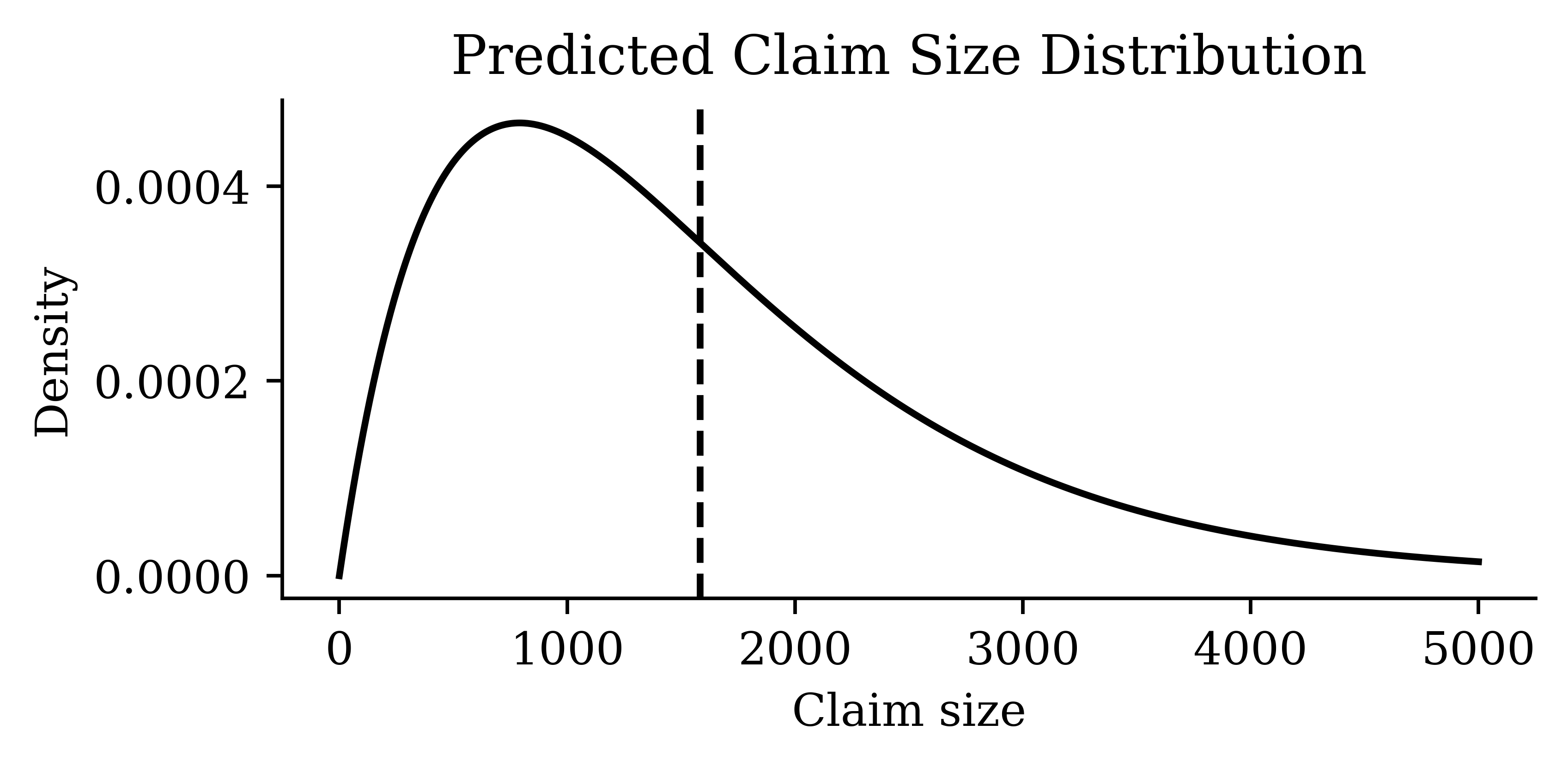

Anatomy of a predicted distribution

From a single predicted distribution we can read off the mean, the variance, and high quantiles (e.g. Value-at-Risk).

Traditional vs distributional regression

Same inputs, same model — the difference is what comes out.

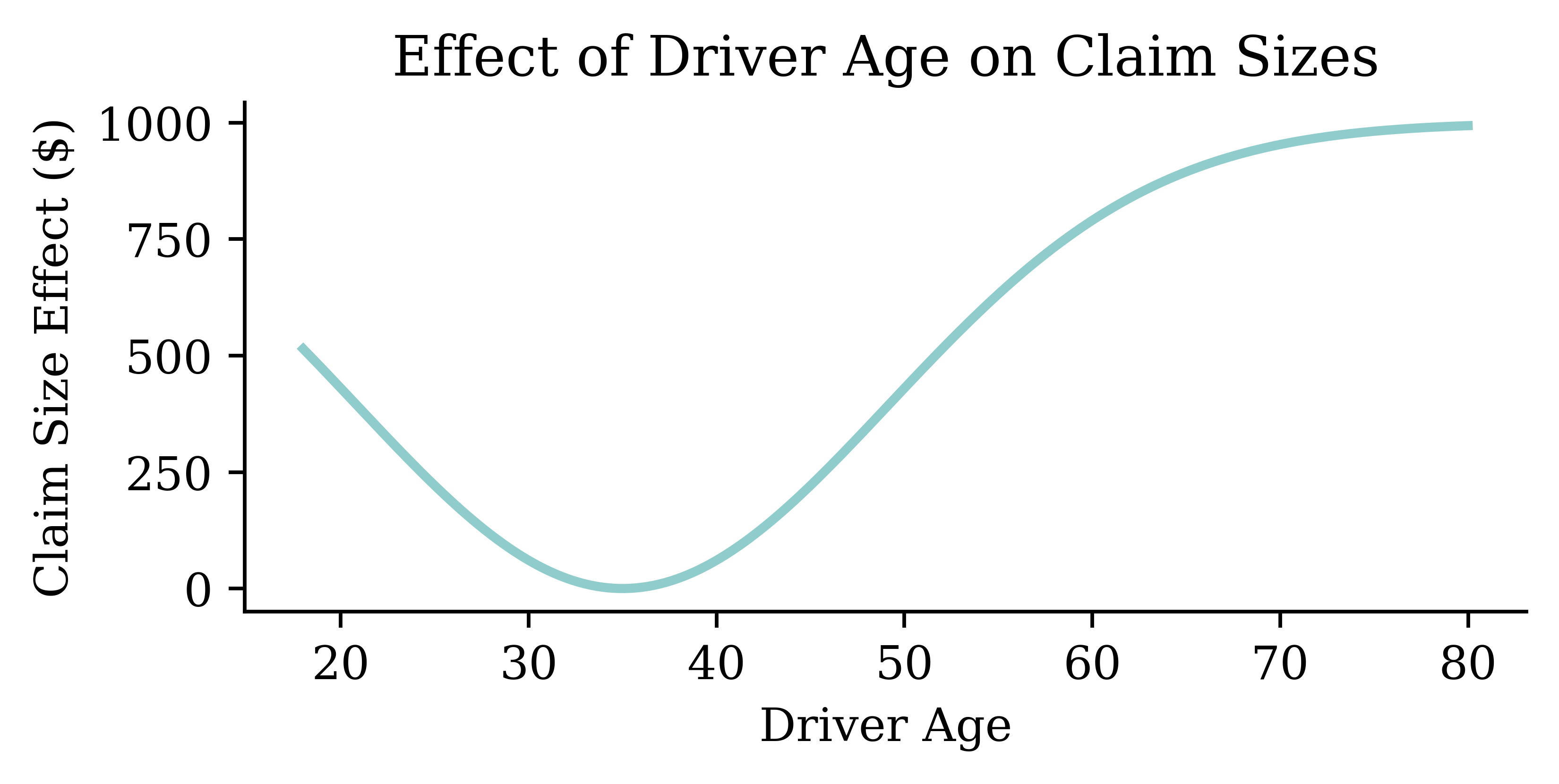

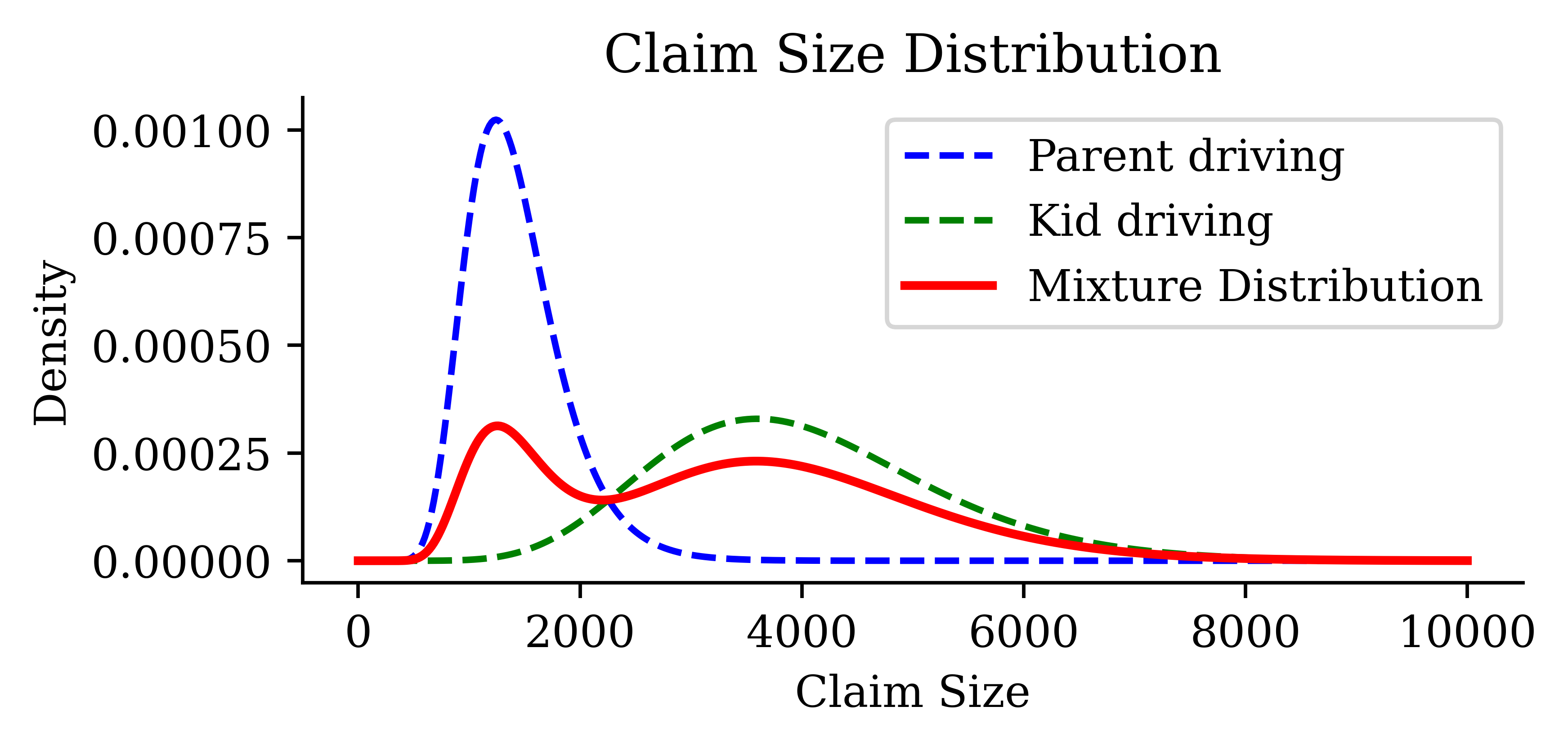

Example 1: Non-monotonicity

GLMs cannot (easily) do this \longrightarrow Use a neural network

Example 2: Multimodality

Key idea

- Earlier machine learning models focused on point estimates.

- However, in many applications, we need to understand the distribution of the response variable.

- Each prediction becomes a distribution over the possible outcomes

We will focus on regression not classification

Classifiers already give us a probability, which is a big step up compared to regression models.

However, neural networks’ “probabilities” can be overconfident.

We already saw a case of this.

See Guo et al. (2017).

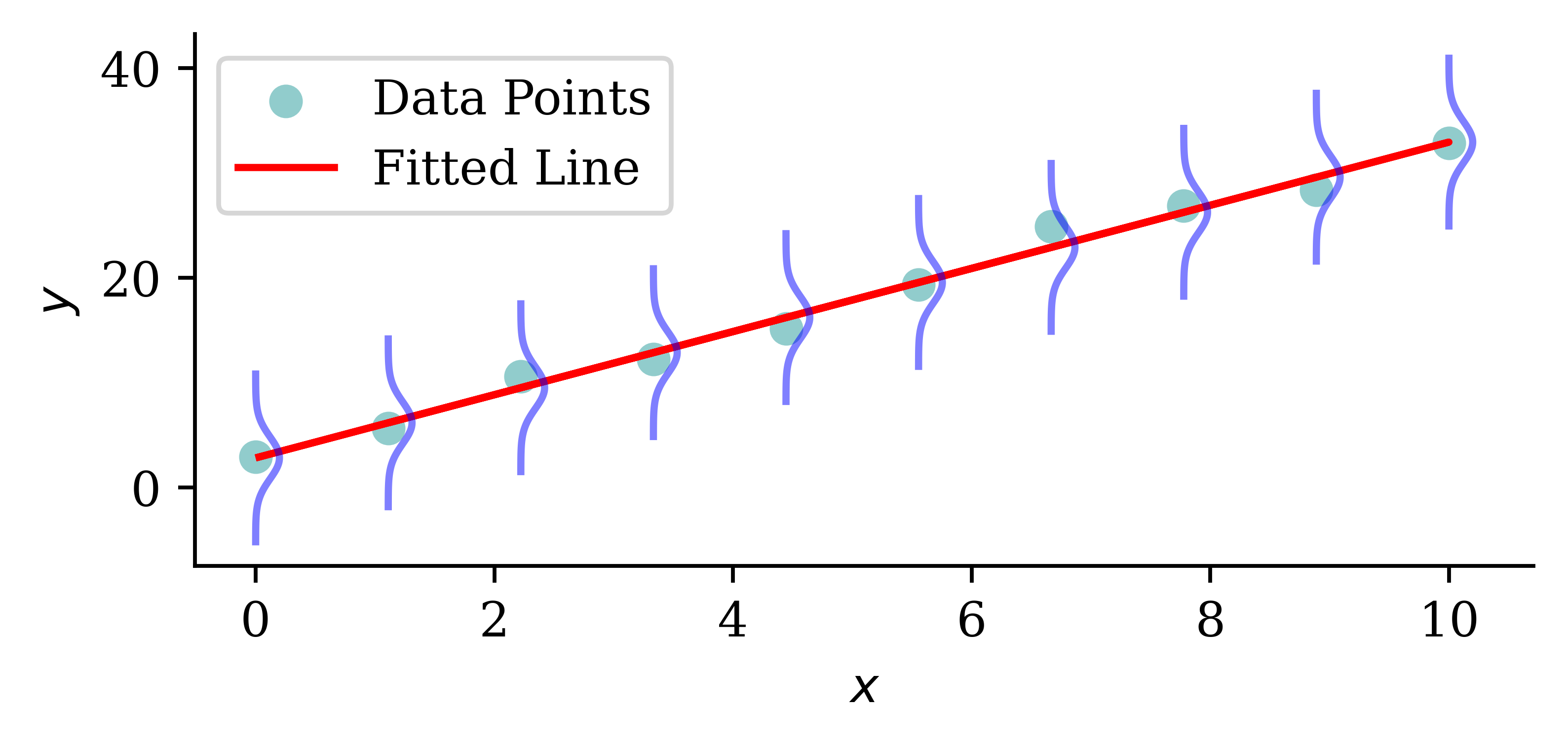

Visualising the distribution of each Y

Code

# Generate sample data for linear regression

np.random.seed(0)

X_toy = np.linspace(0, 10, 10)

np.random.shuffle(X_toy)

beta_0 = 2

beta_1 = 3

y_toy = beta_0 + beta_1 * X_toy + np.random.normal(scale=2, size=X_toy.shape)

sigma_toy = 2 # Assuming a standard deviation for the normal distribution

# Fit a simple linear regression model

coefficients = np.polyfit(X_toy, y_toy, 1)

predicted_y = np.polyval(coefficients, X_toy)

# Plot the data points and the fitted line

plt.scatter(X_toy, y_toy, label='Data Points')

plt.plot(X_toy, predicted_y, color='red', label='Fitted Line')

# Draw the normal distribution bell curve sideways at each data point

for i in range(len(X_toy)):

mu = predicted_y[i]

y_values = np.linspace(mu - 4*sigma_toy, mu + 4*sigma_toy, 100)

x_values = stats.norm.pdf(y_values, mu, sigma_toy) + X_toy[i]

plt.plot(x_values, y_values, color='blue', alpha=0.5)

plt.xlabel('$x$')

plt.ylabel('$y$')

plt.legend()

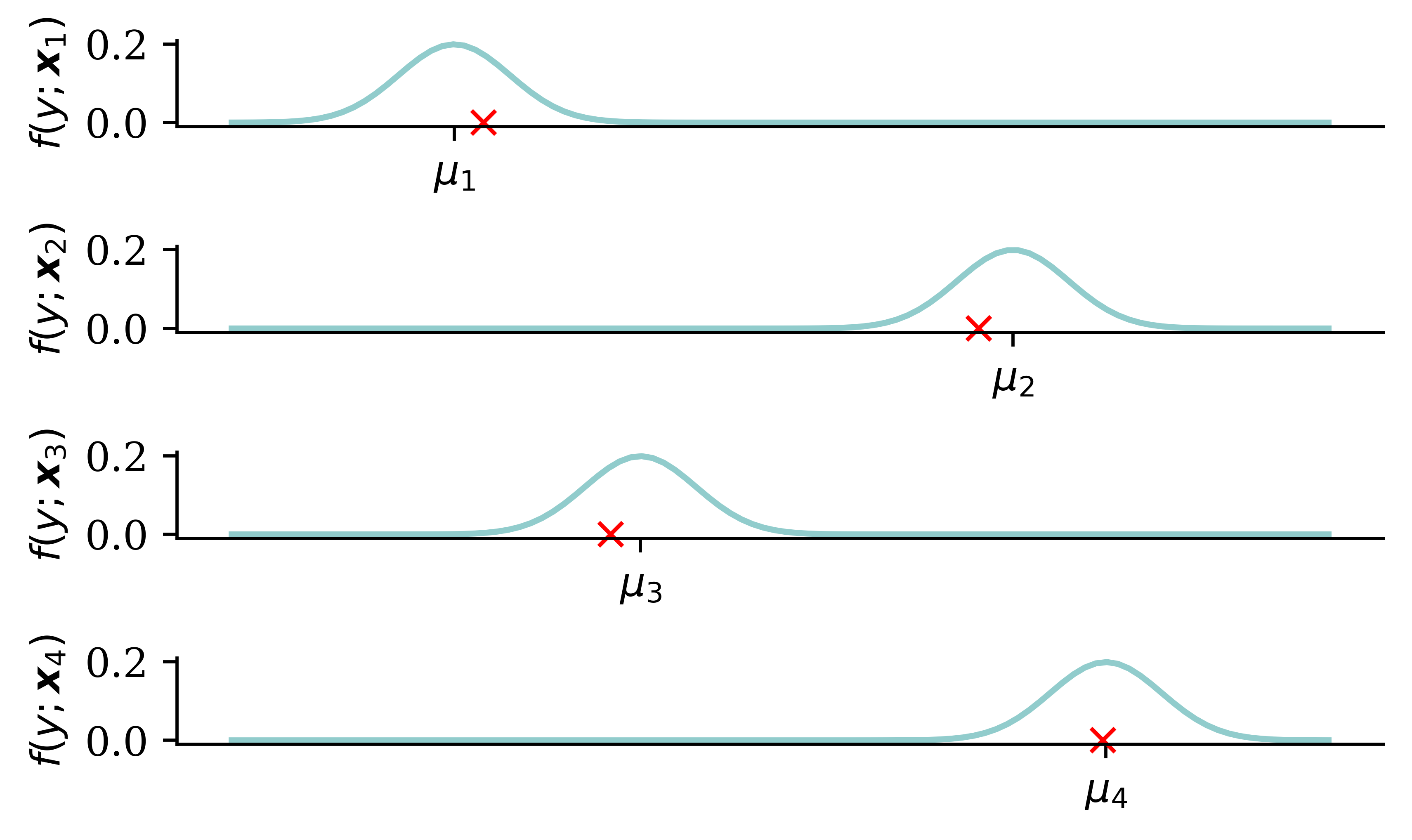

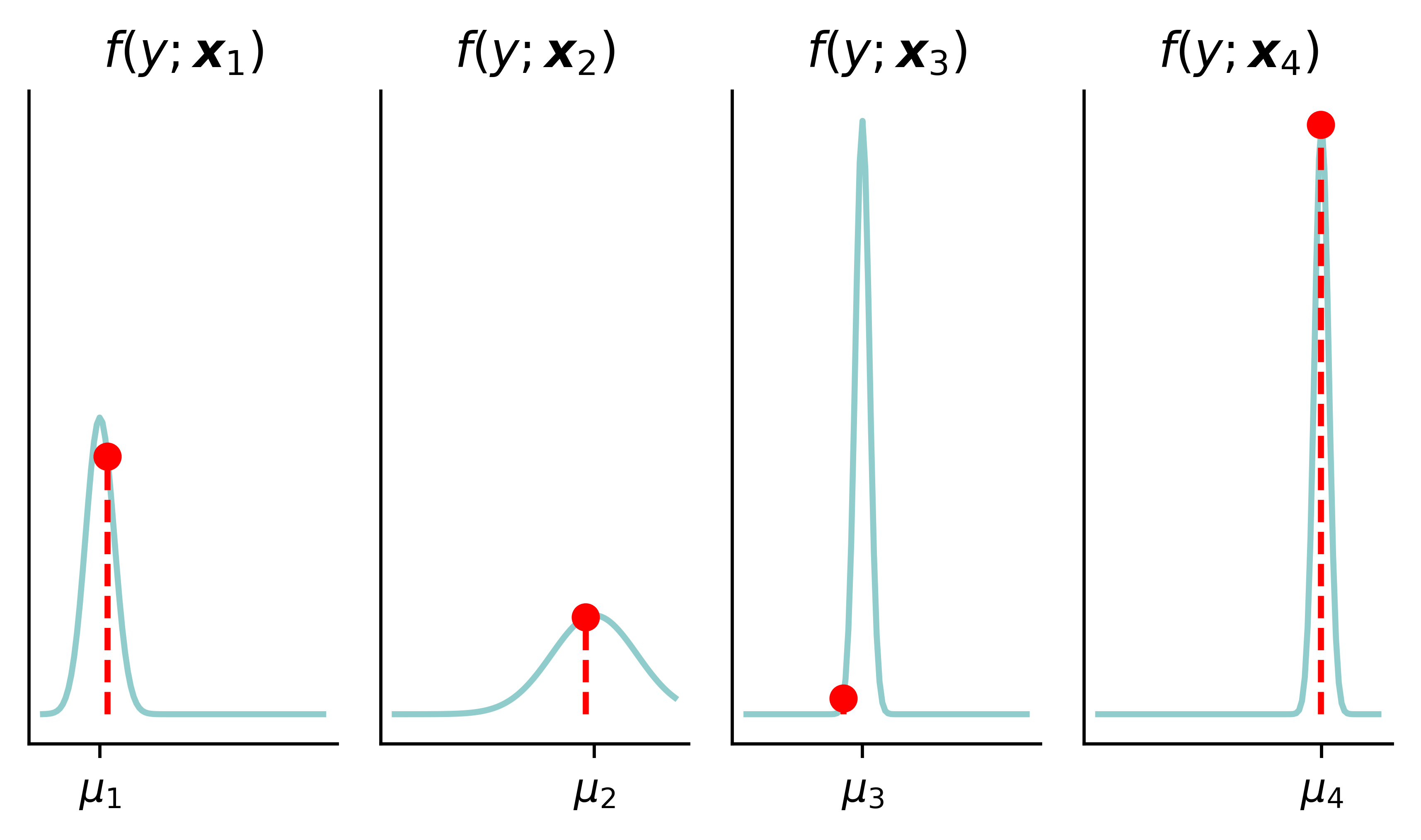

The predicted distributions

Code

y_pred = np.polyval(coefficients, X_toy[:4])

fig, axes = plt.subplots(4, 1, figsize=(5.0, 3.0))

x_min = y_pred[:4].min() - 4*sigma_toy

x_max = y_pred[:4].max() + 4*sigma_toy

x_grid = np.linspace(x_min, x_max, 100)

# Plot each normal distribution with different means vertically

for i, ax in enumerate(axes):

mu = y_pred[i]

y_grid = stats.norm.pdf(x_grid, mu, sigma_toy)

ax.plot(x_grid, y_grid)

ax.set_ylabel(f'$f(y ; \\boldsymbol{{x}}_{{{i+1}}})$')

ax.set_xticks([y_pred[i]], labels=[r'$\mu_{' + str(i+1) + r'}$'])

ax.plot(y_toy[i], 0, 'rx', clip_on=False)

plt.tight_layout();

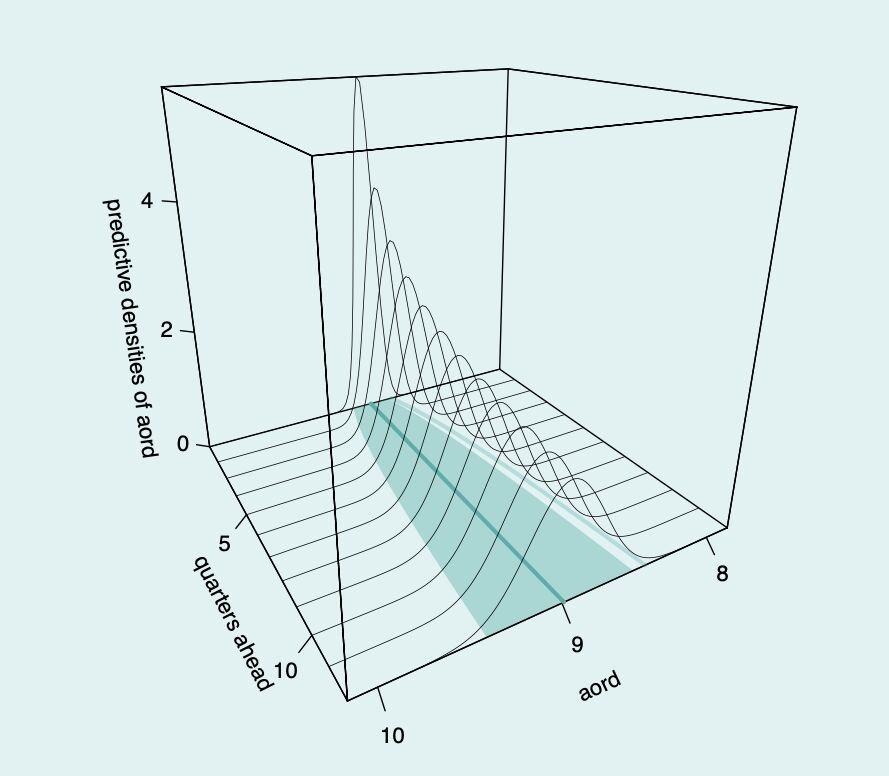

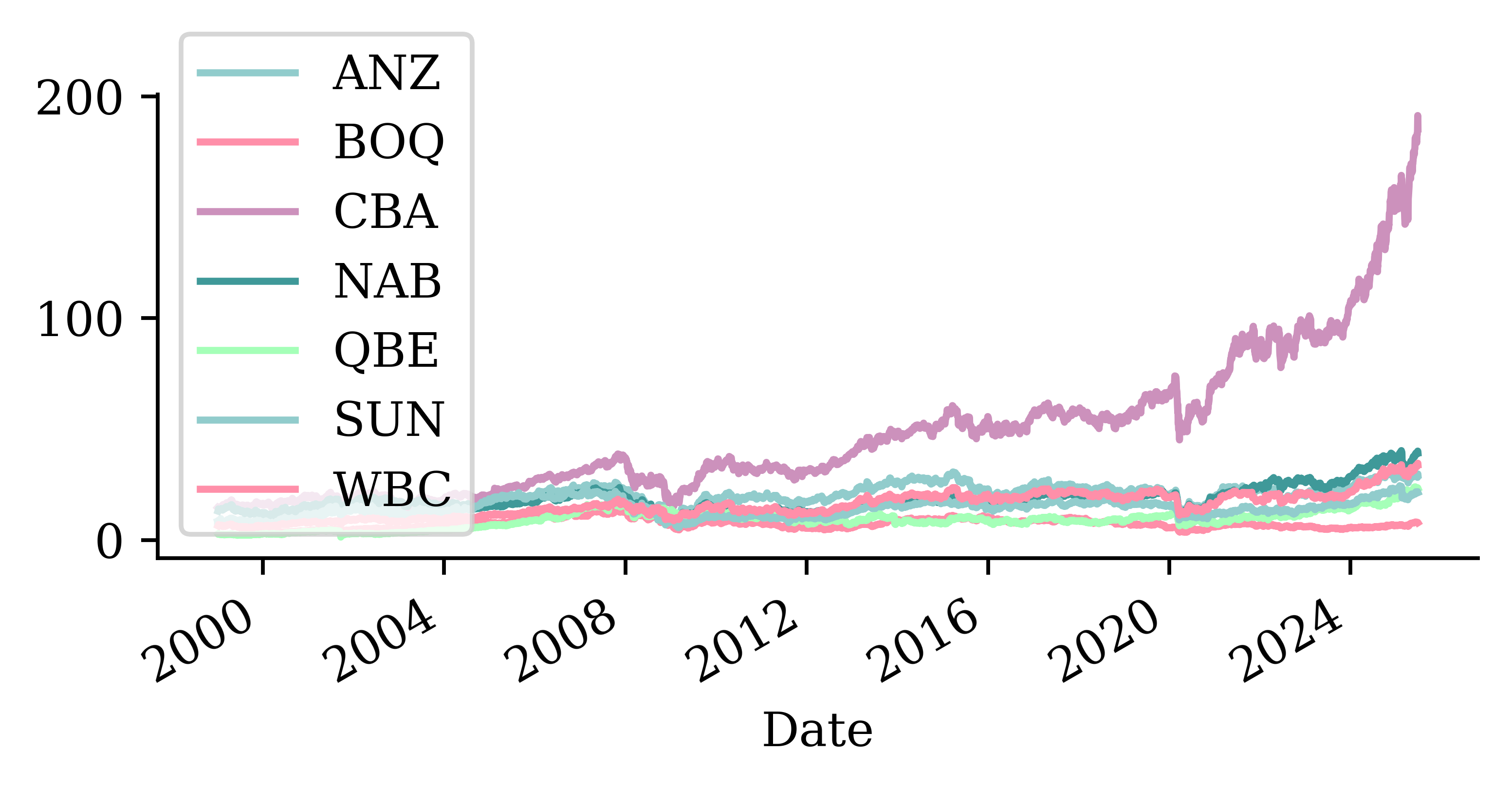

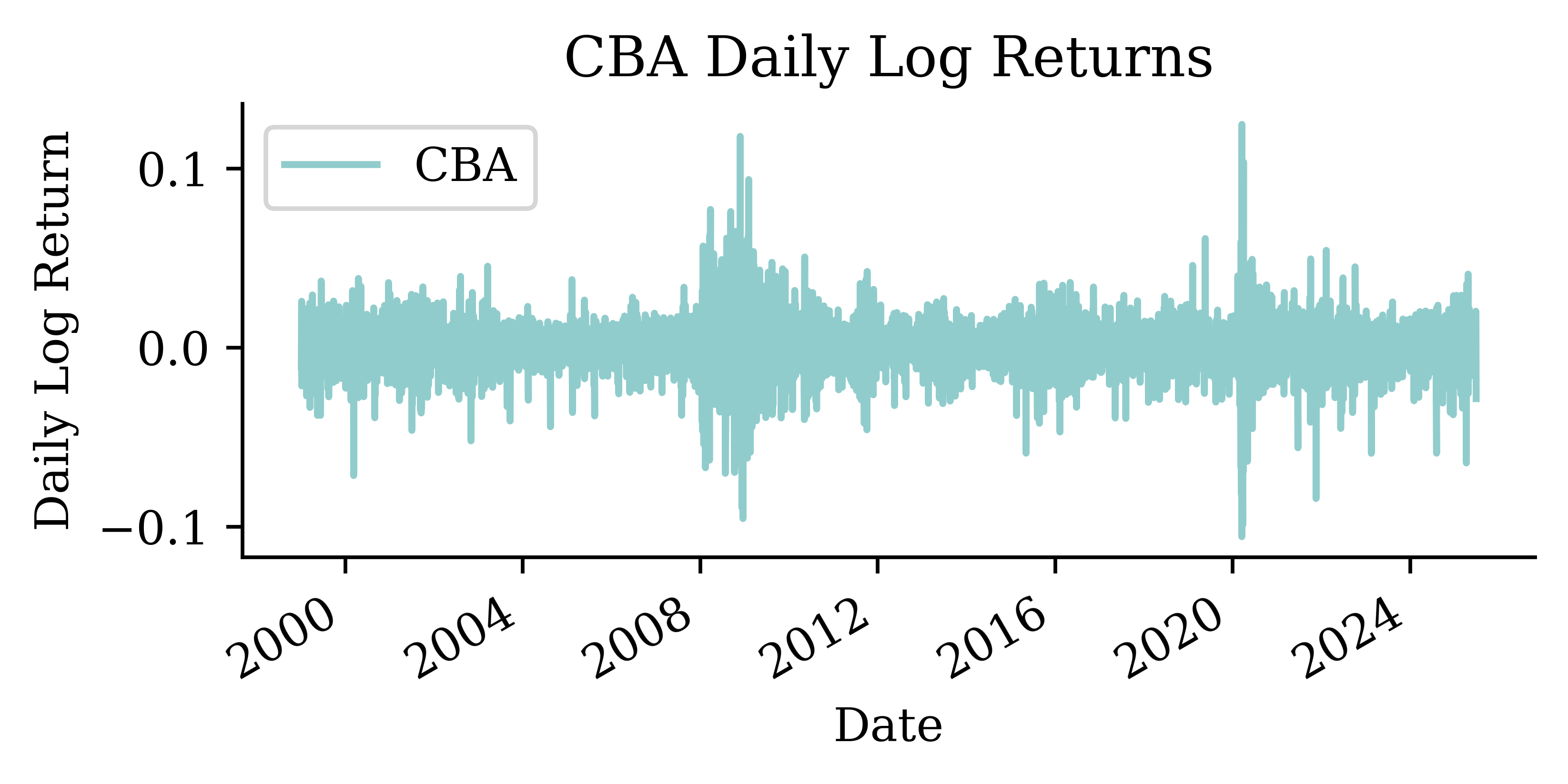

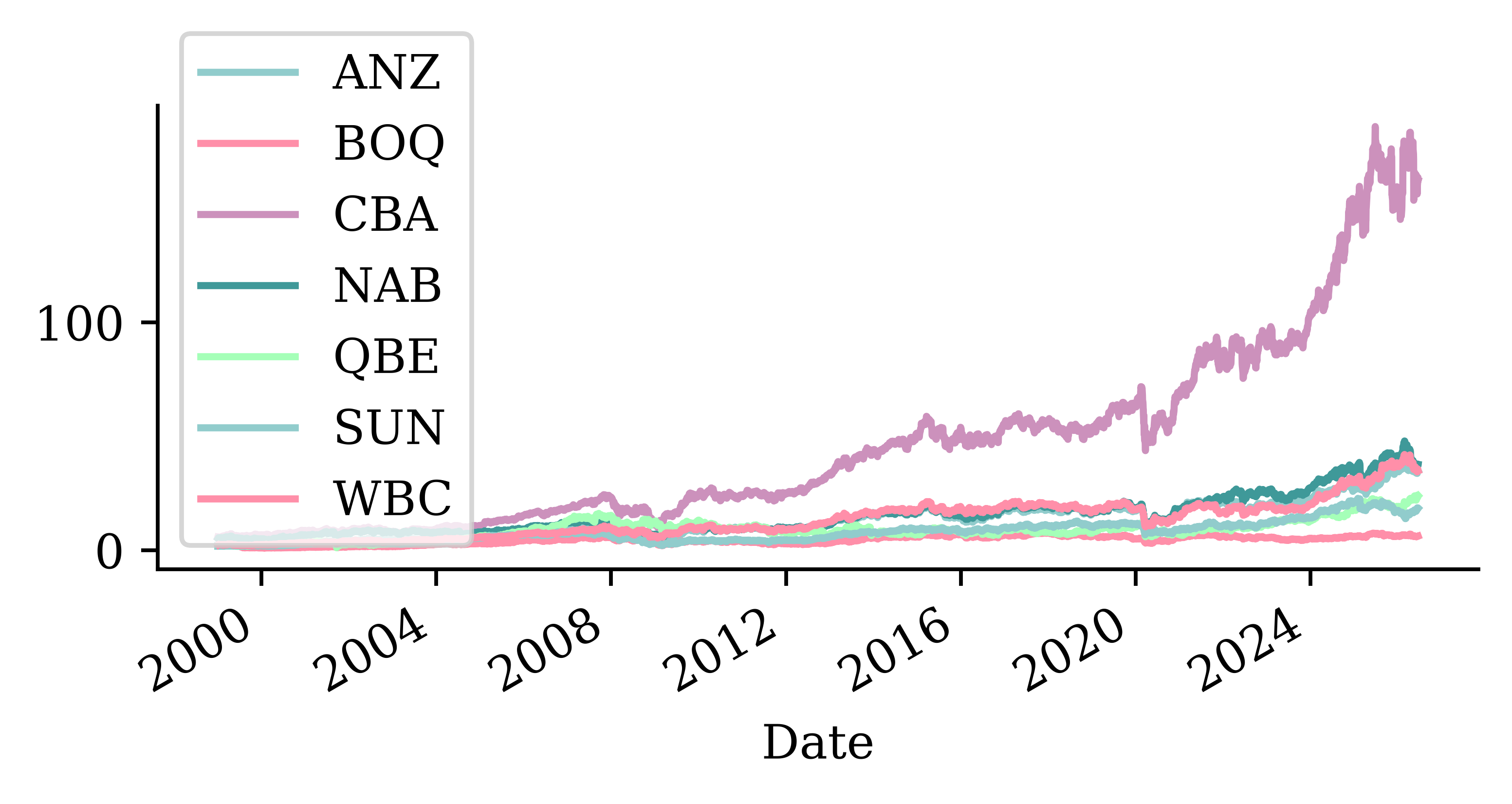

Stock price forecasting

Code

def lagged_timeseries(df, target, window):

lagged = pd.DataFrame()

for i in range(window, 0, -1):

lagged[f"T-{i}"] = df[target].shift(i)

lagged["T"] = df[target].values

return lagged

stocks = pd.read_csv("data/interim/aus_fin_stocks.csv")

stocks["Date"] = pd.to_datetime(stocks["Date"])

stocks = stocks.set_index("Date")

_ = stocks.pop("ASX200")

stock = stocks[["CBA"]]

stock = stock.ffill()

# Compute daily log returns

stock_log = np.log(stock / stock.shift(1)).dropna()

# Helper functions for converting log returns to prices

def log_to_price(log_returns, initial_price):

cumulative_log_returns = log_returns.cumsum()

return initial_price * np.exp(cumulative_log_returns)

def get_last_price(stock_df, cutoff_date):

last_known_date = stock_df.loc[:cutoff_date].index[-1]

return stock_df.loc[last_known_date, "CBA"]

# Create lagged features from log returns

df_lags = lagged_timeseries(stock_log, "CBA", 40)

# Split the data in time (same cutoffs as the Time Series lecture)

X_train = df_lags.loc[:"2014"]

X_val = df_lags.loc["2015":"2020"]

X_test = df_lags.loc["2021":]

# Remove any with NAs and split into X and y

X_train = X_train.dropna()

X_val = X_val.dropna()

X_test = X_test.dropna()

y_train = X_train.pop("T")

y_val = X_val.pop("T")

y_test = X_test.pop("T")

lr = LinearRegression()

lr.fit(X_train, y_train);

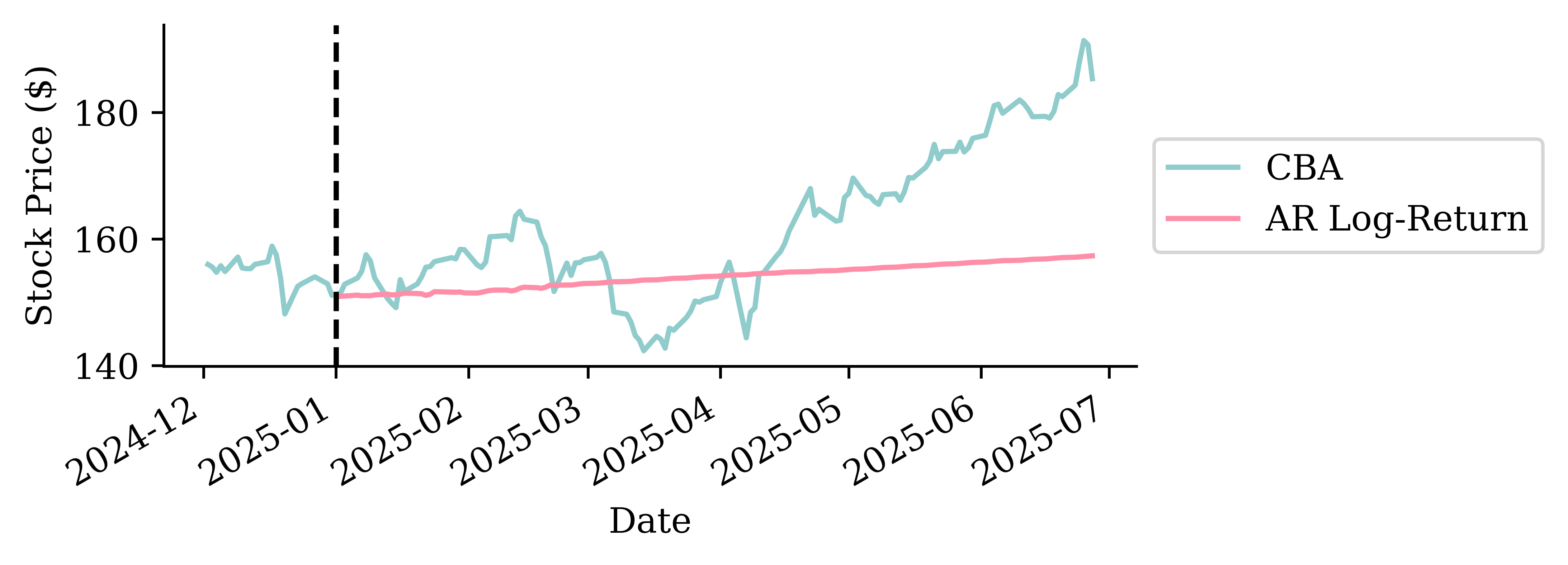

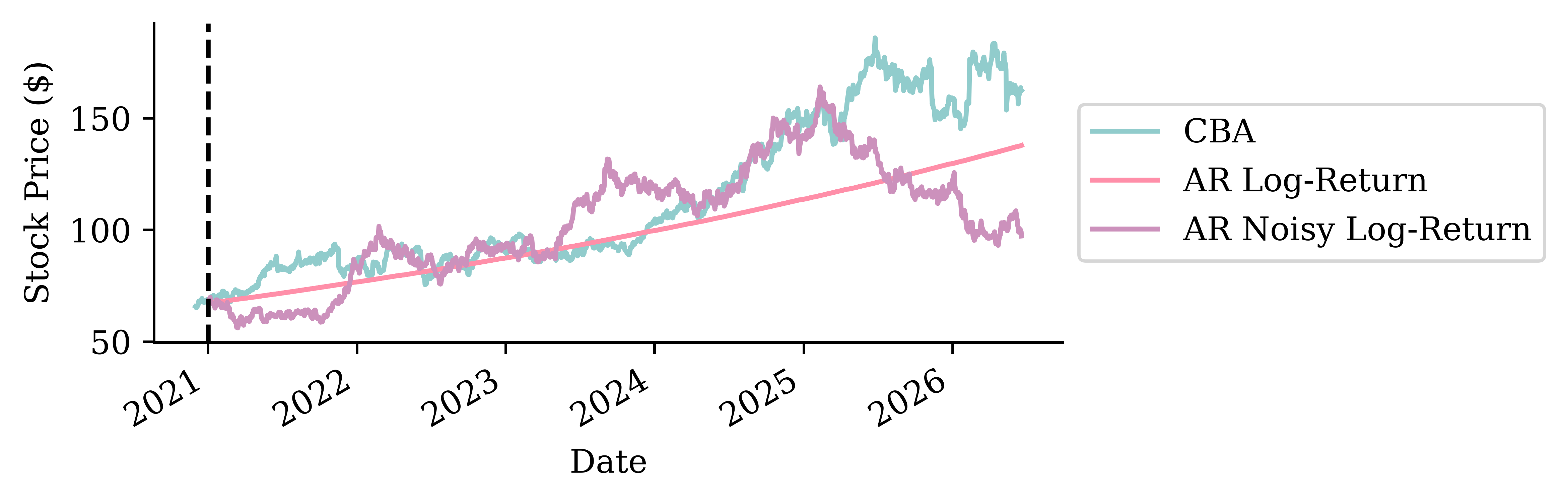

Original forecast

Code

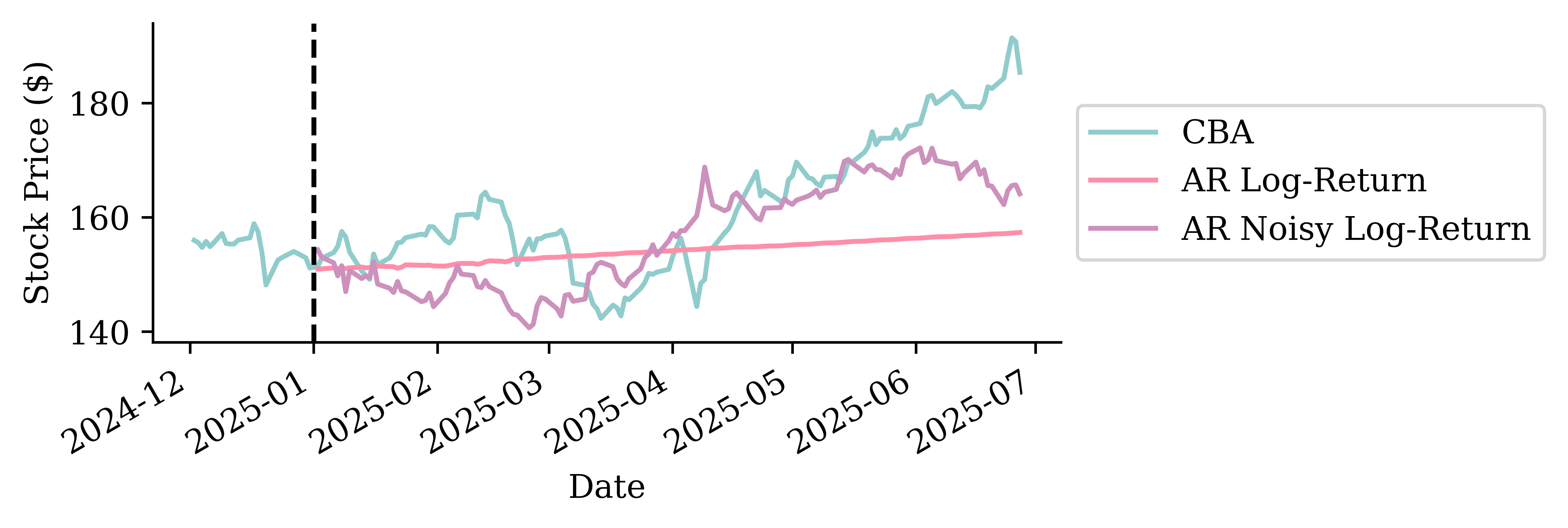

With noise

With noise

With noise

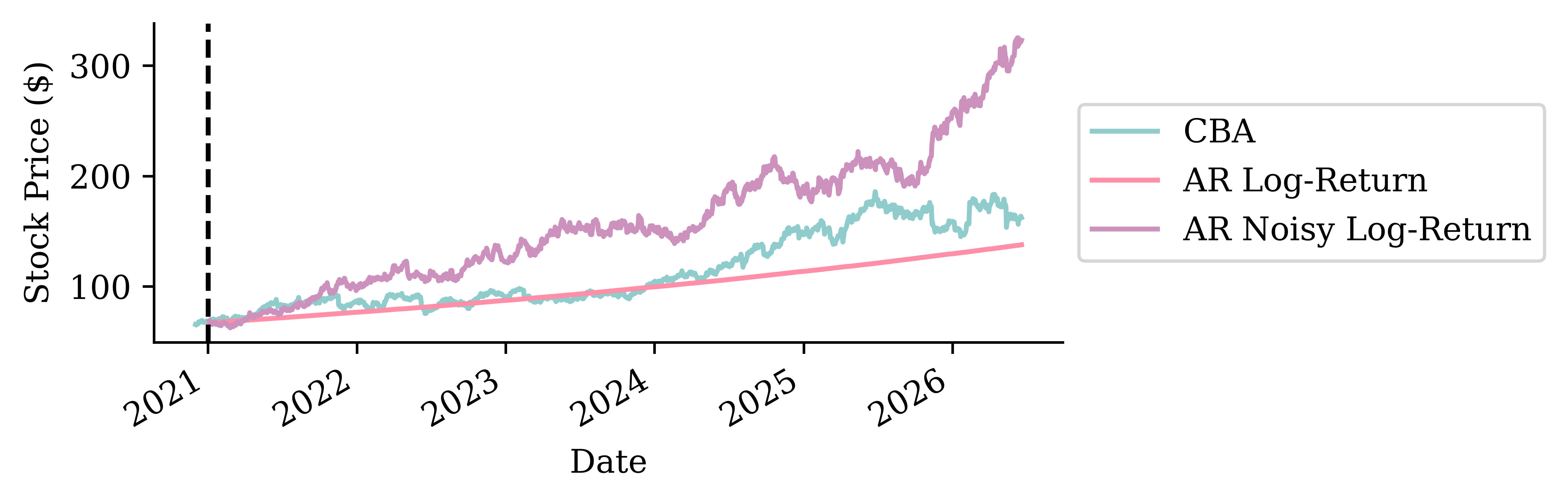

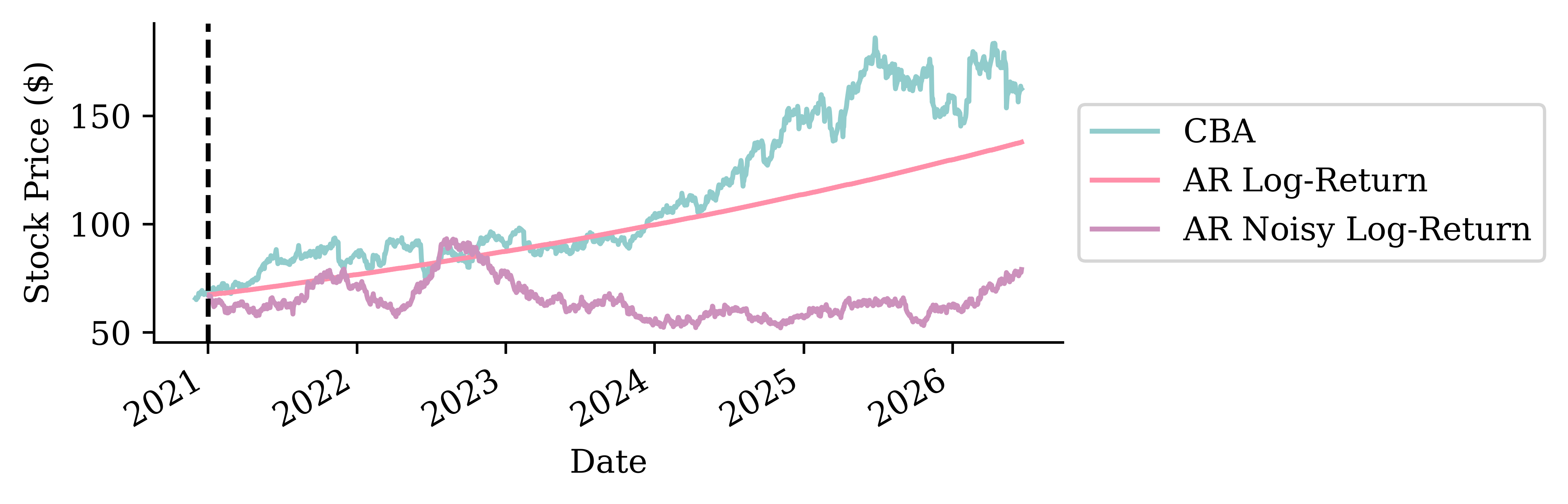

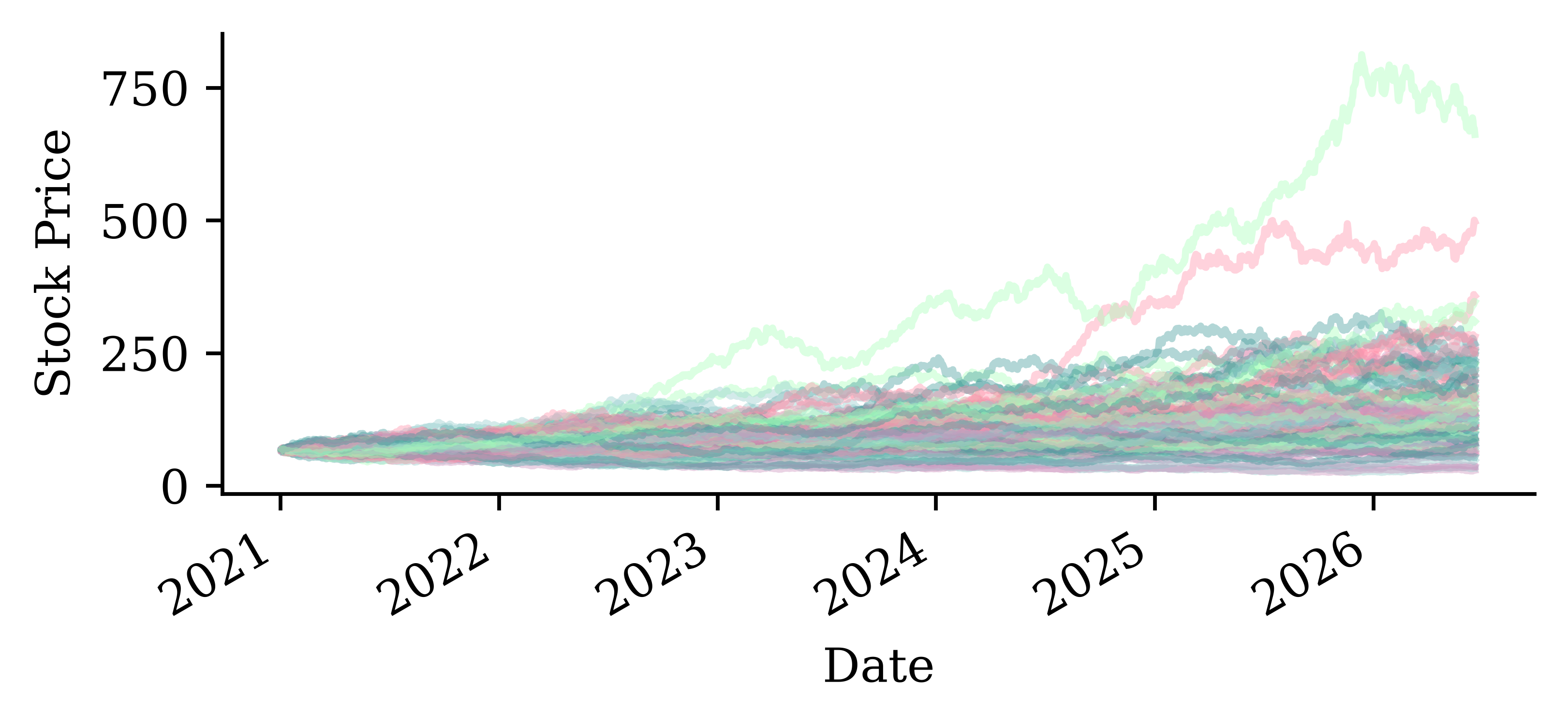

Many noisy forecasts

95% “prediction intervals”

Code

# Plot the mean forecast

plt.figure(figsize=(8, 3))

plt.plot(stock.loc["2020-12":].index, stock.loc["2020-12":]["CBA"], label="CBA")

plt.plot(mean_forecast, label="Mean")

# Plot the quantile-based shaded area

plt.fill_between(mean_forecast.index,

lower_quantile,

upper_quantile,

color="grey", alpha=0.2)

# Plot settings

plt.axvline(pd.Timestamp("2021-01-01"), color="black", linestyle="--")

plt.legend(loc="center left", bbox_to_anchor=(1, 0.5))

plt.xlabel("Date")

plt.ylabel("Stock Price")

plt.tight_layout();

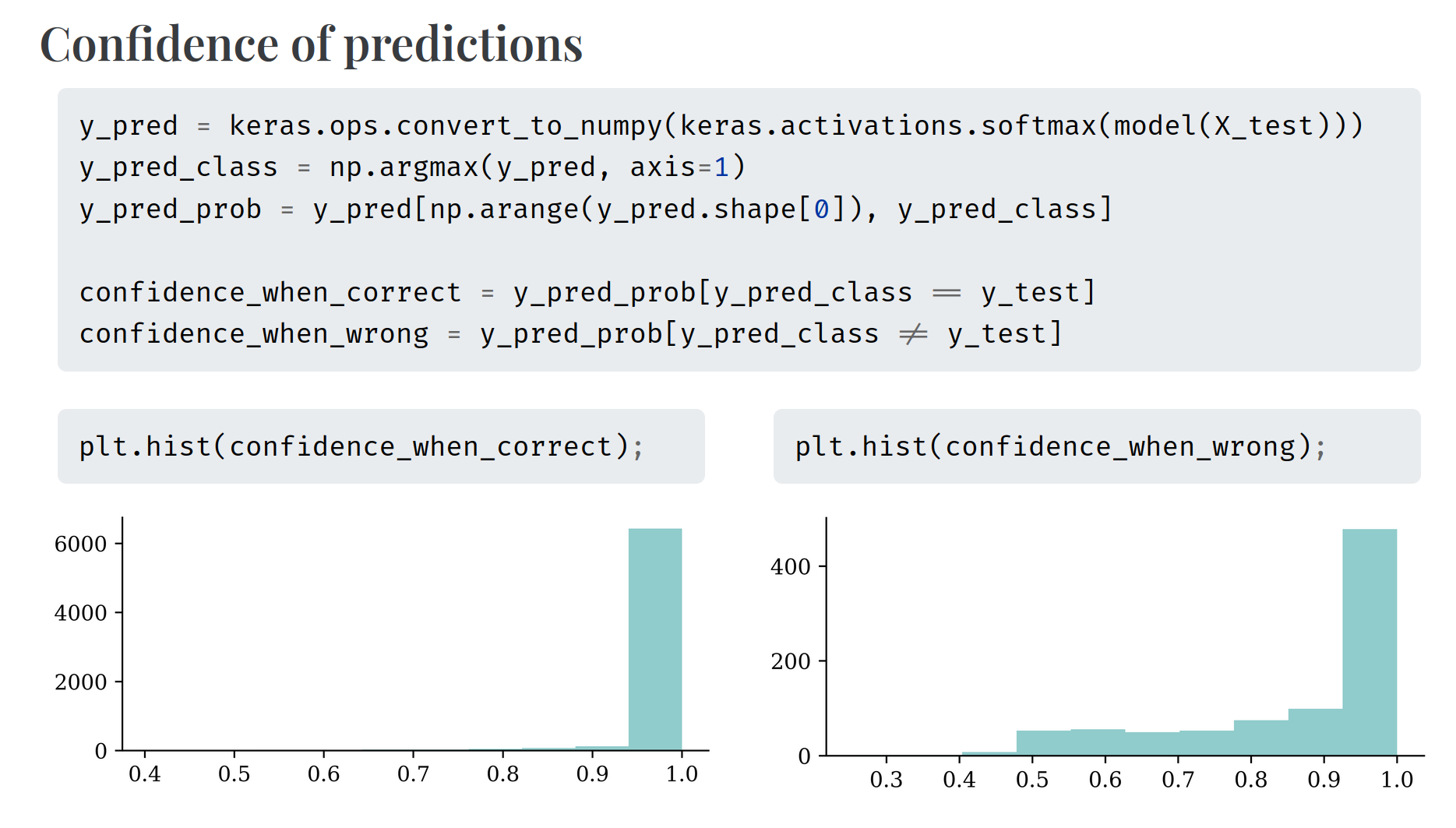

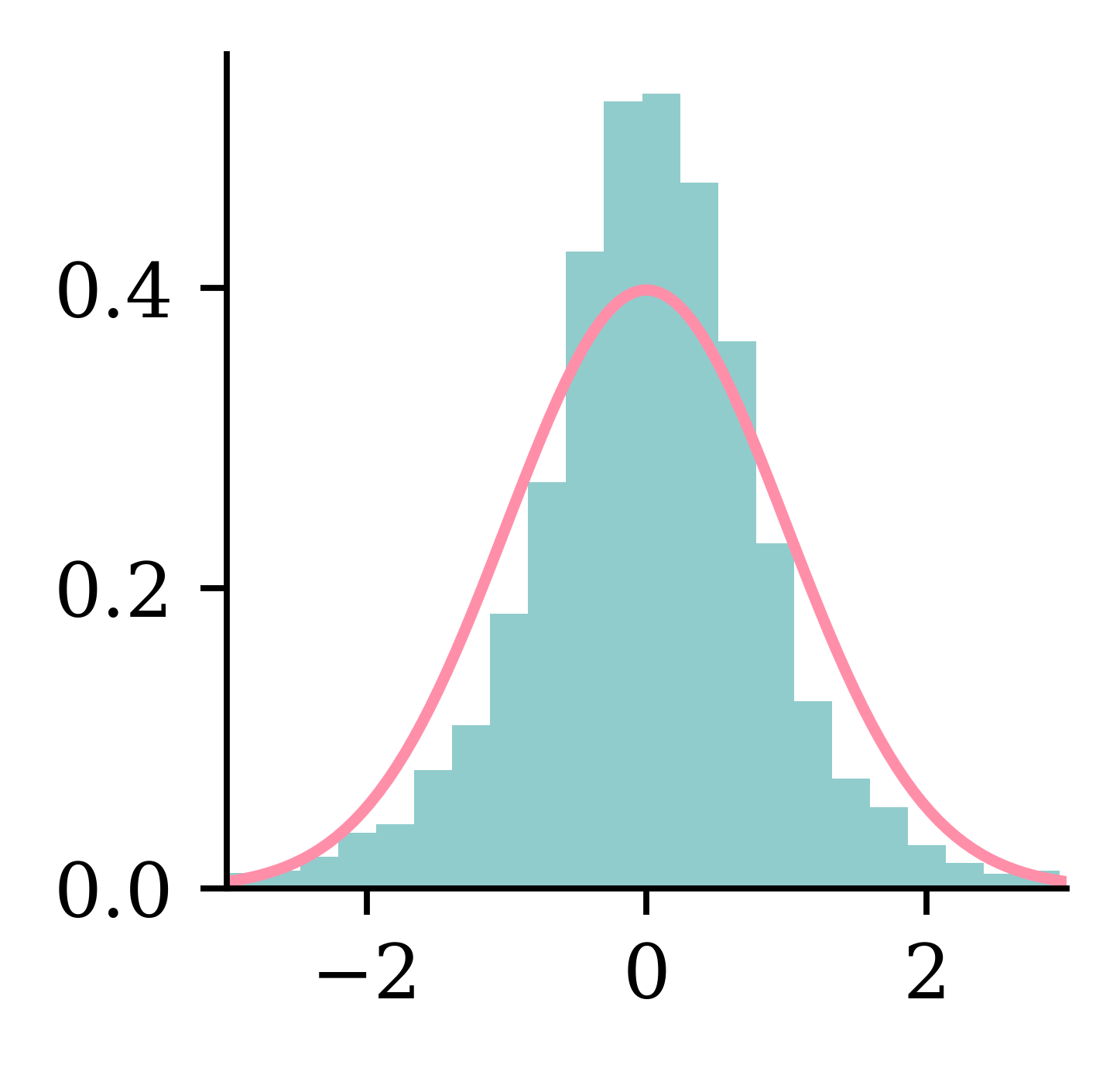

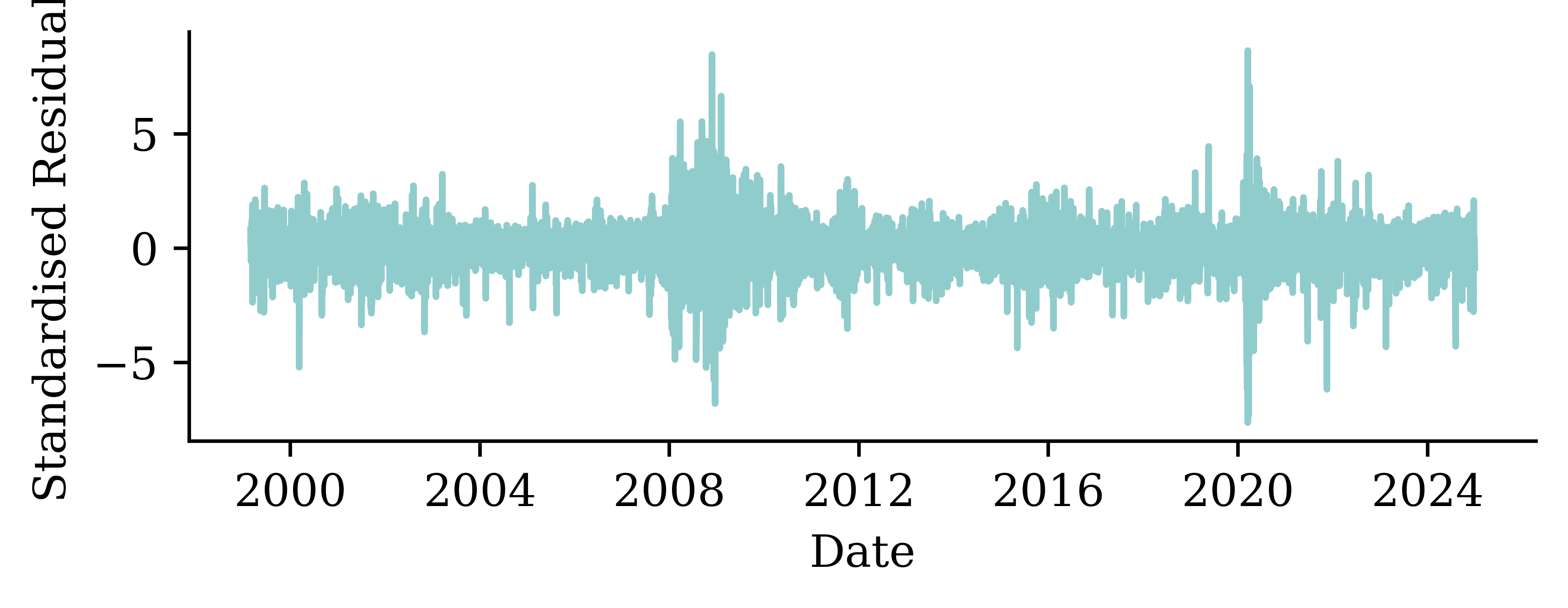

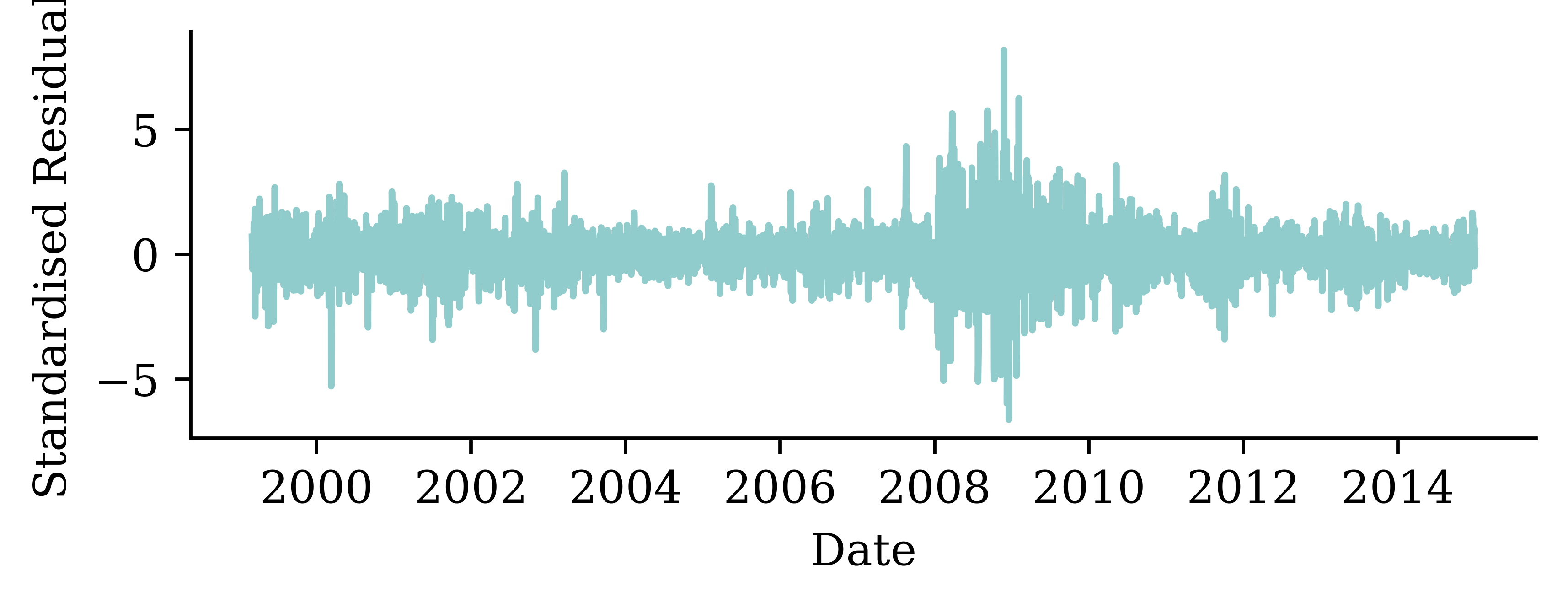

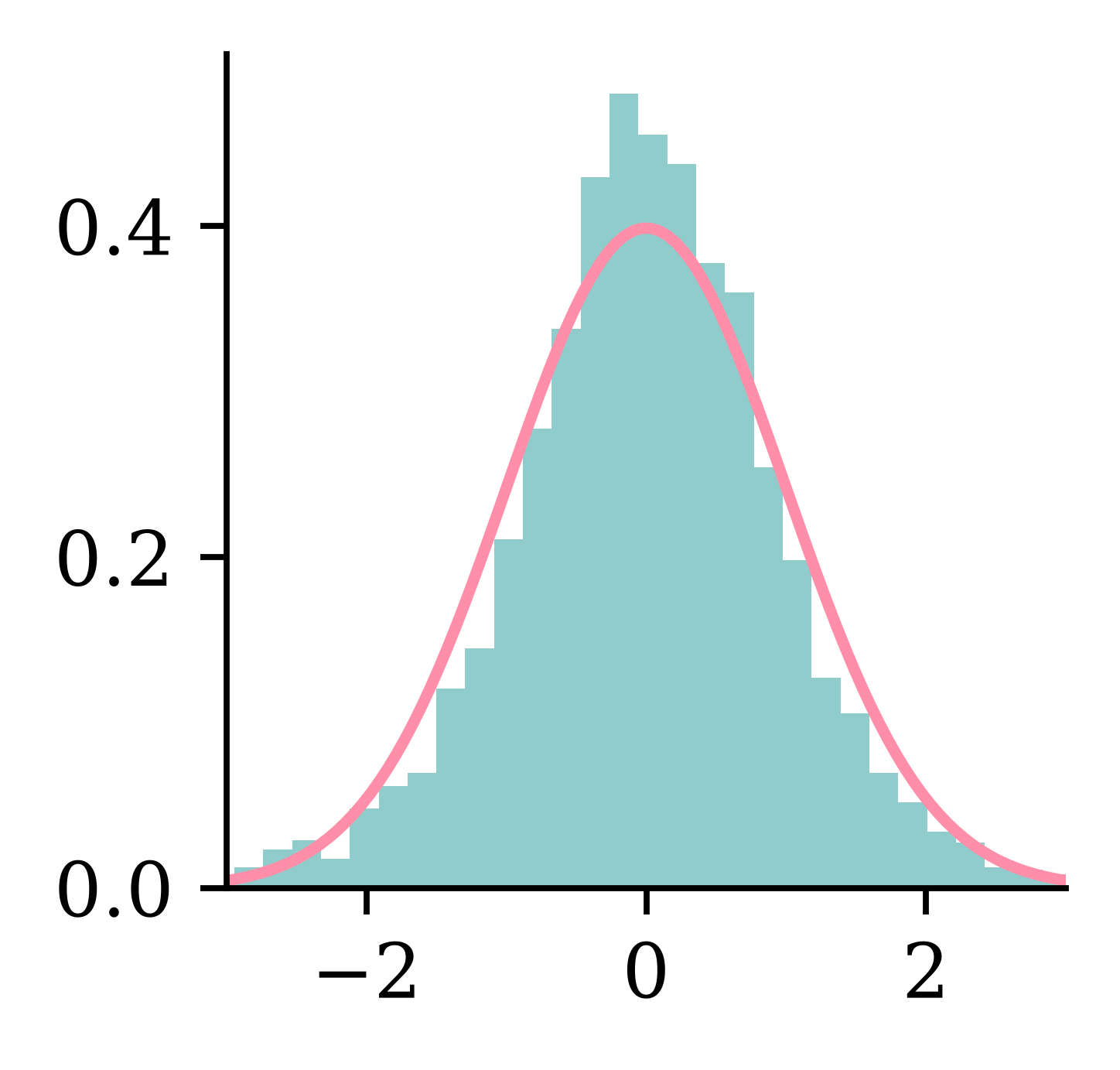

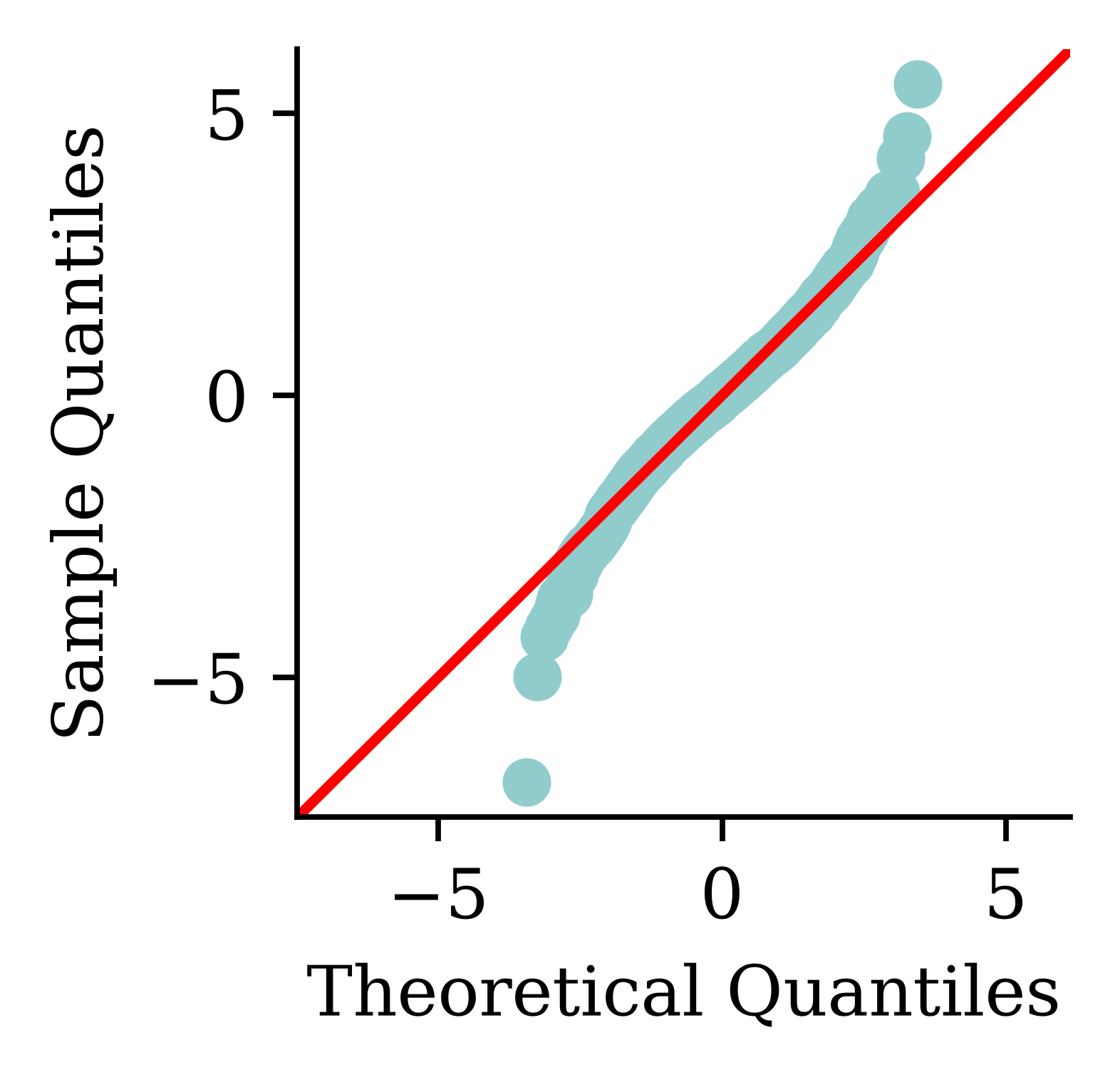

Residuals

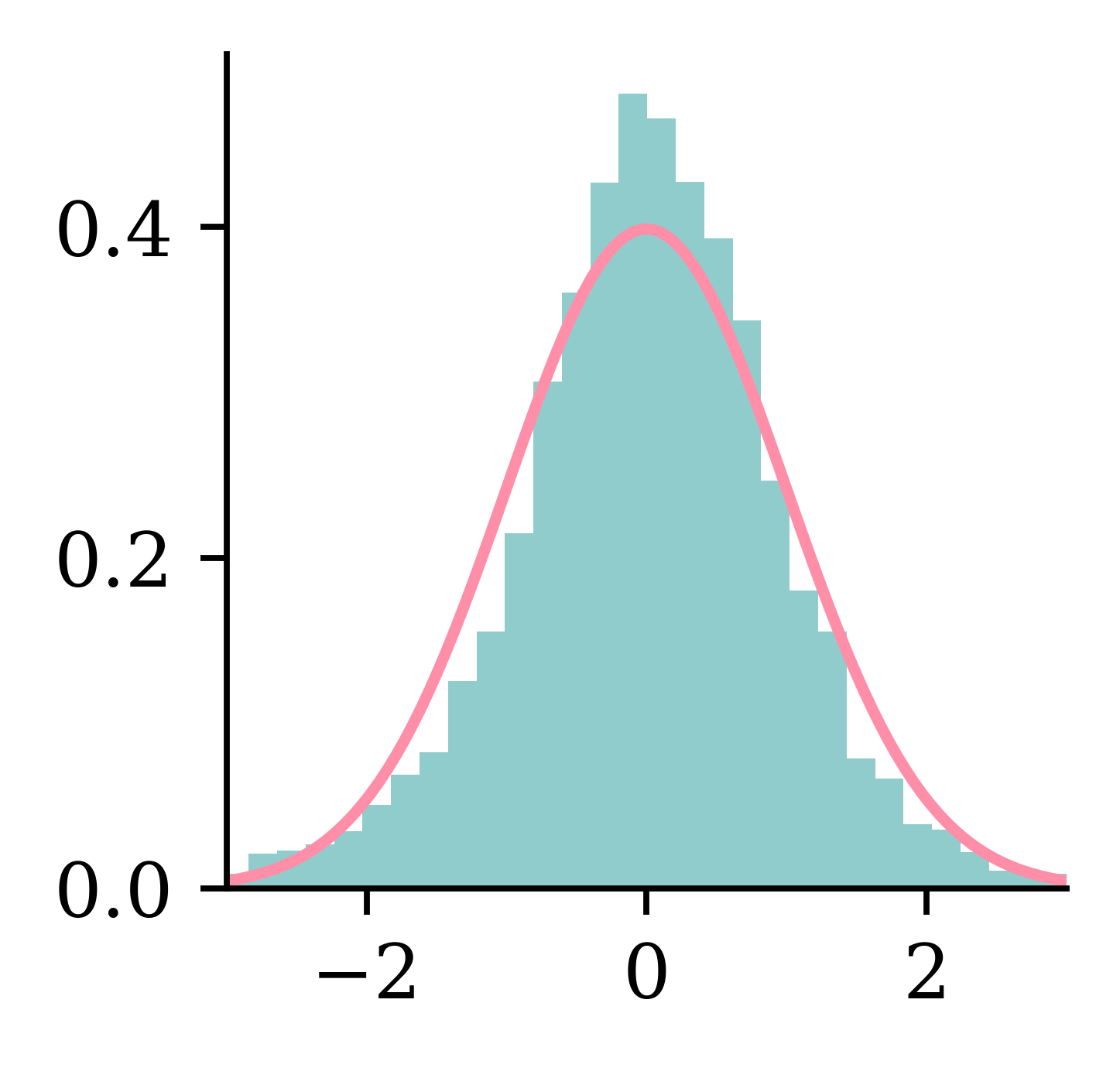

Q-Q plot and P-P plot

Residuals against time

Code

Heteroskedasticity!

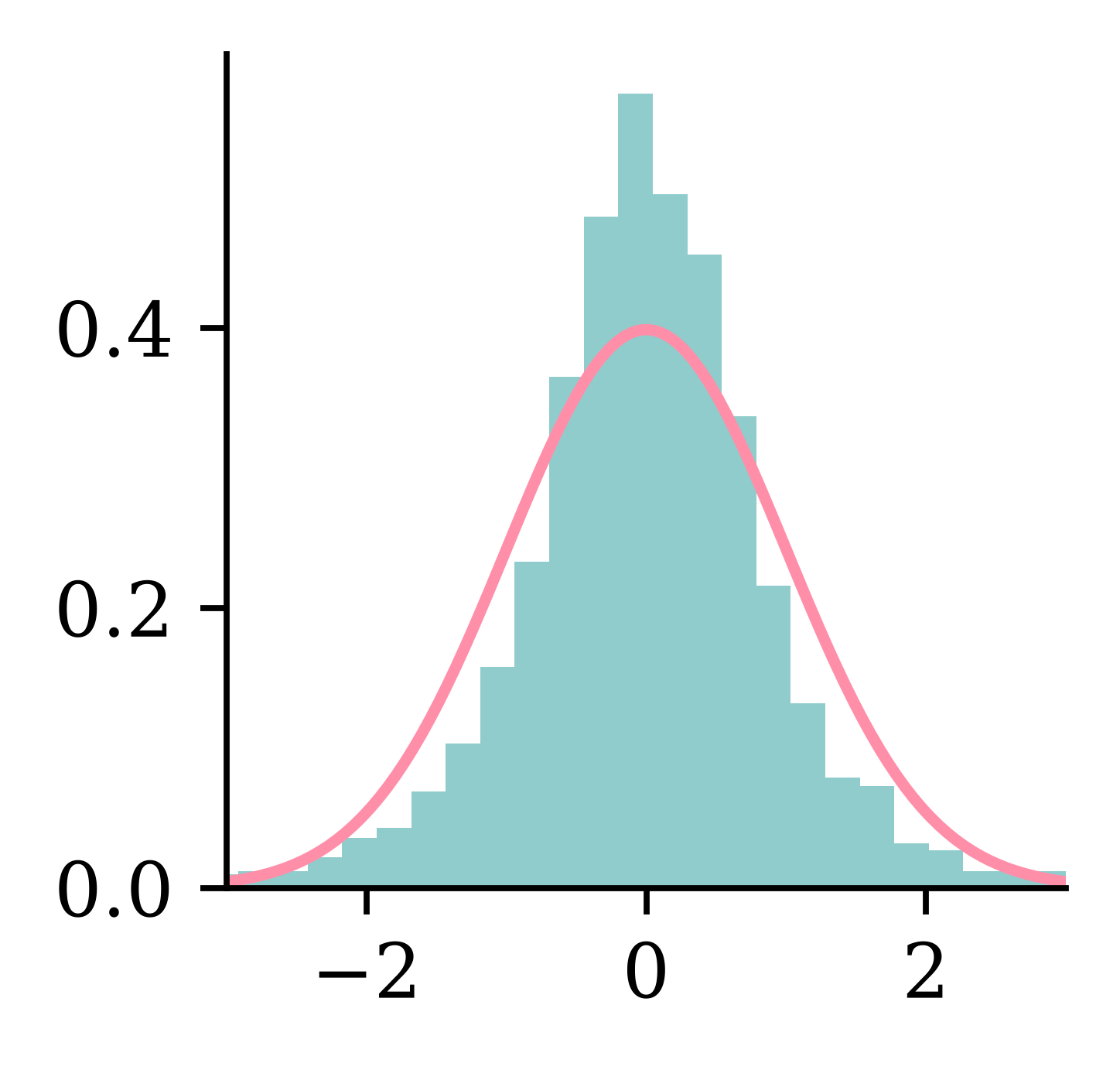

Retrain on less data

Code

# Drop the GFC years (2008-2009) from the training set

mask = ~((y_train.index.year >= 2008) & (y_train.index.year <= 2009))

X2 = X_train.loc[mask]

y2 = y_train.loc[mask]

lr2 = LinearRegression()

lr2.fit(X2, y2)

res2 = y2 - lr2.predict(X2)

res2 = (res2 - np.mean(res2)) / np.std(res2)

plt.plot(y2.index, res2)

plt.xlabel("Date")

plt.ylabel("Standardised Residuals")

plt.tight_layout();

Refit the model without the GFC crisis years.

Residual diagnostics

ShapiroResult(statistic=np.float64(0.983029219714092), pvalue=np.float64(3.326265726133293e-20))

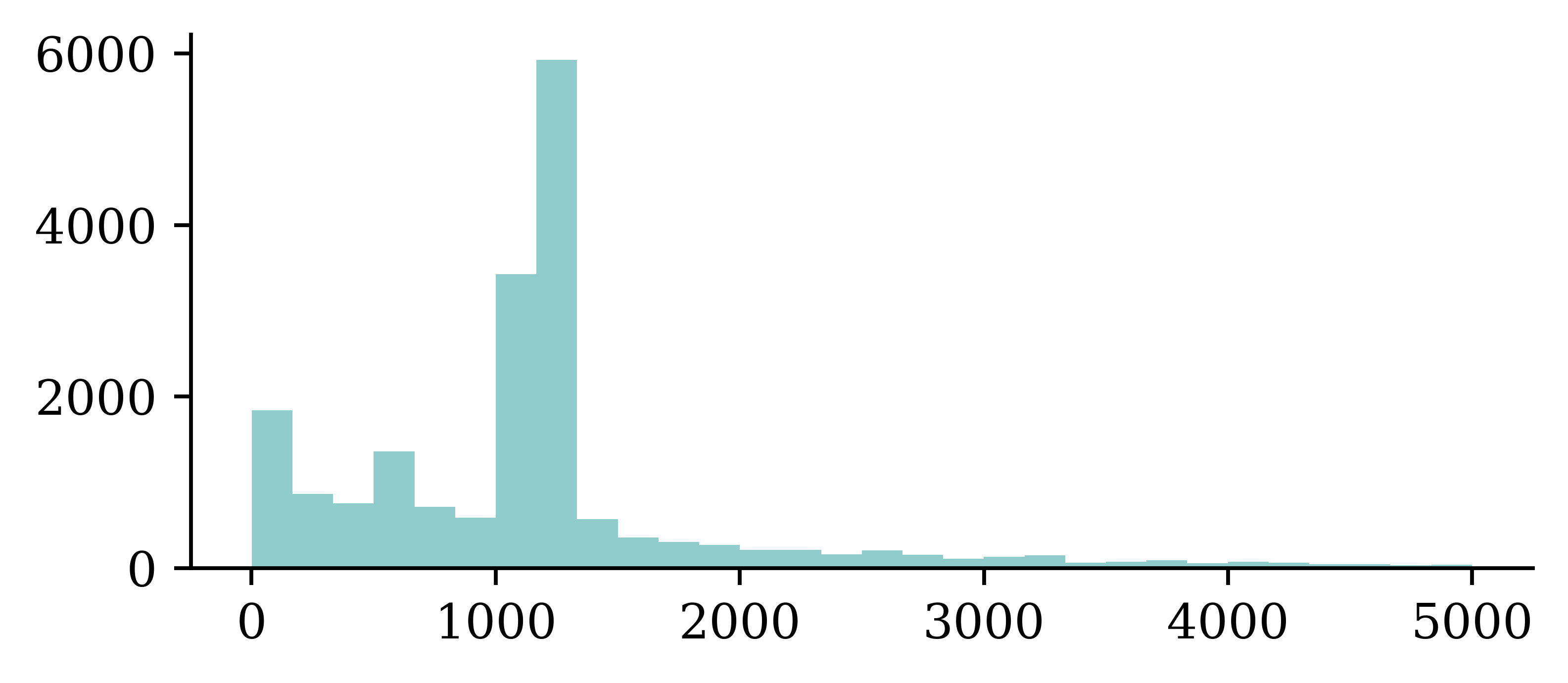

Preprocessing

X_train, X_test, y_train, y_test = train_test_split(

sev.drop("ClaimAmount", axis=1), sev["ClaimAmount"], random_state=2023)

ct = make_column_transformer(

(make_pipeline(OrdinalEncoder(), StandardScaler()), ["Area", "VehGas"]),

("drop", ["VehBrand", "Region"]), remainder=StandardScaler())

X_train = ct.fit_transform(X_train)

X_test = ct.transform(X_test)

plt.hist(y_train[y_train < 5000], bins=30);

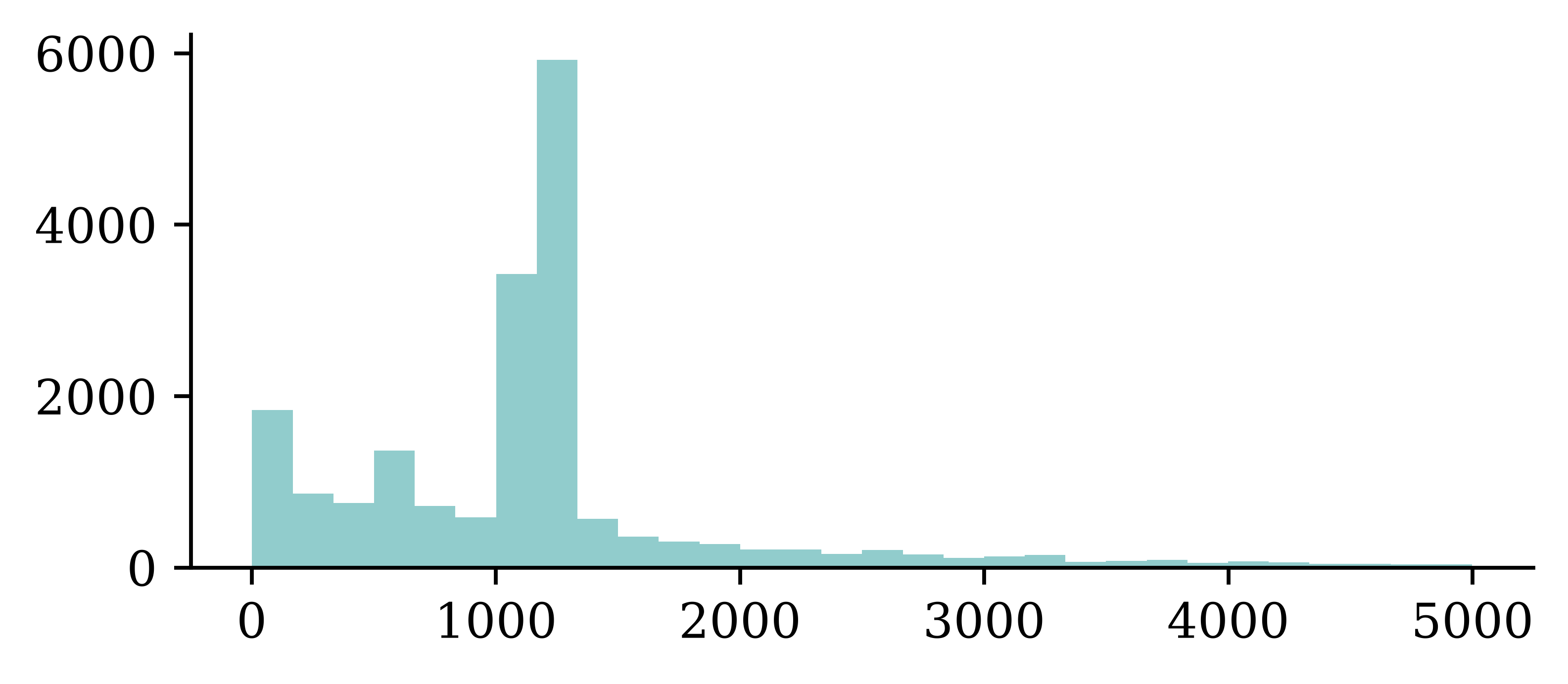

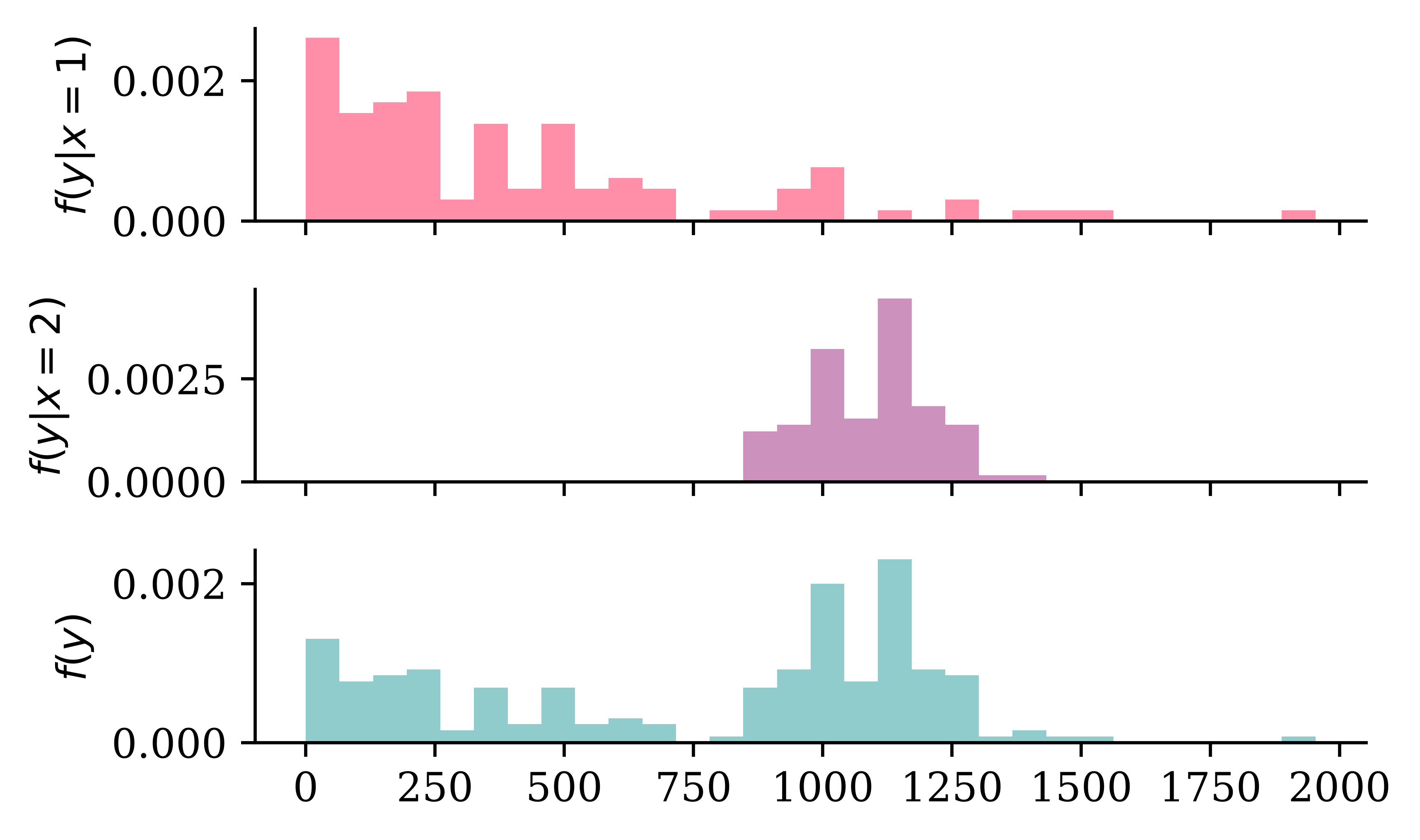

Doesn’t prove that Y | \boldsymbol{X} = \boldsymbol{x} is multimodal

Code

# Make some example where the distribution is multimodal because of a binary covariate which separates the means of the two distributions

np.random.seed(1)

fig, axes = plt.subplots(3, 1, figsize=(5.0, 3.0), sharex=True)

x_min = 0

x_max = y_train.max()

x_grid = np.linspace(x_min, x_max, 100)

# Simulate some data from an exponential distribution which has Pr(X < 1000) = 0.9

n = 100

p = 0.1

lambda_ = -np.log(p) / 1000

mu = 1 / lambda_

y_1 = np.random.exponential(scale=mu, size=n)

# Pick a truncated normal distribution with a mean of 1100 and std of 250 (truncated to be positive)

mu = 1100

sigma = 100

y_2 = stats.truncnorm.rvs((0 - mu) / sigma, (np.inf - mu) / sigma, loc=mu, scale=sigma, size=n)

# Combine y_1 and y_2 for the final histogram

y = np.concatenate([y_1, y_2])

# Determine common bins

bins = np.histogram_bin_edges(y, bins=30)

# Plot each normal distribution with different means vertically

for i, ax in enumerate(axes):

if i == 0:

ax.hist(y_1, bins=bins, density=True, color=COLOURS[i+1])

ax.set_ylabel(f'$f(y | x = 1)$')

elif i == 1:

ax.hist(y_2, bins=bins, density=True, color=COLOURS[i+1])

ax.set_ylabel(f'$f(y | x = 2)$')

else:

ax.hist(y, bins=bins, density=True)

ax.set_ylabel(f'$f(y)$')

plt.tight_layout();

What the GLM predicts

A GLM predicts the mean for each input; the dispersion is a single shared constant, estimated separately.

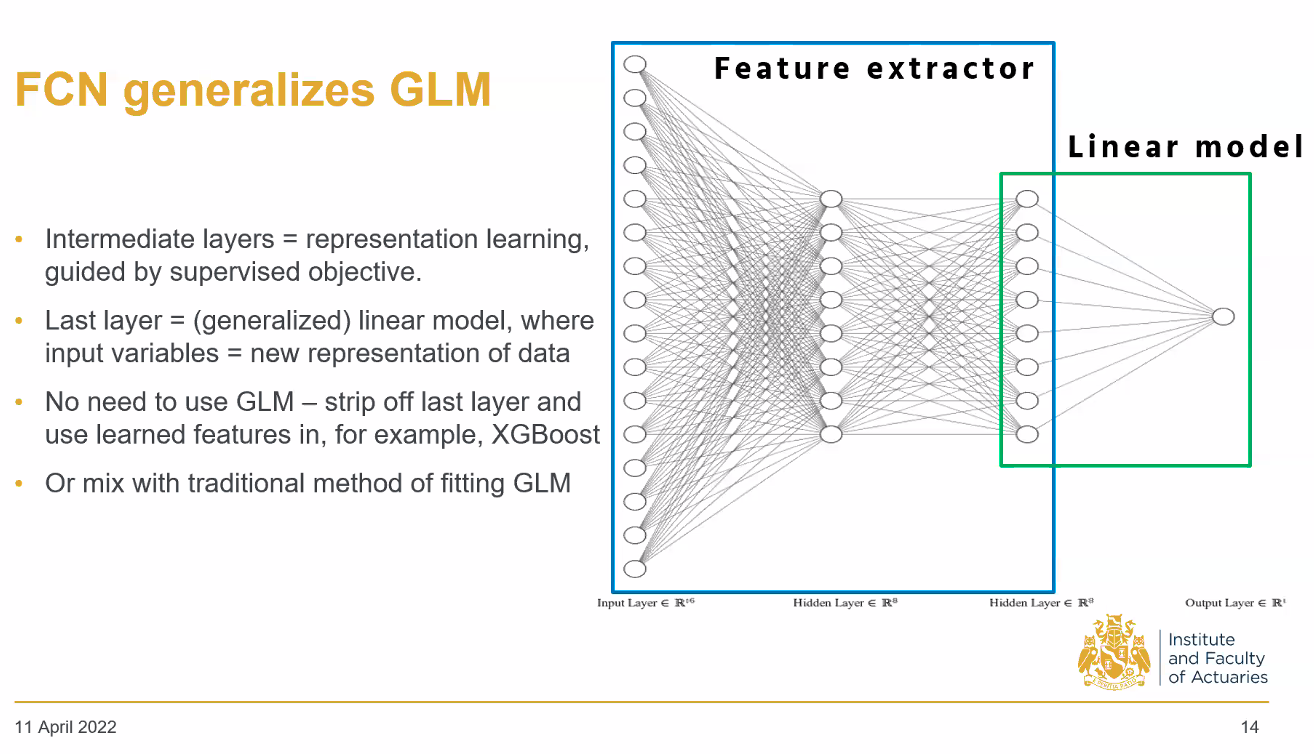

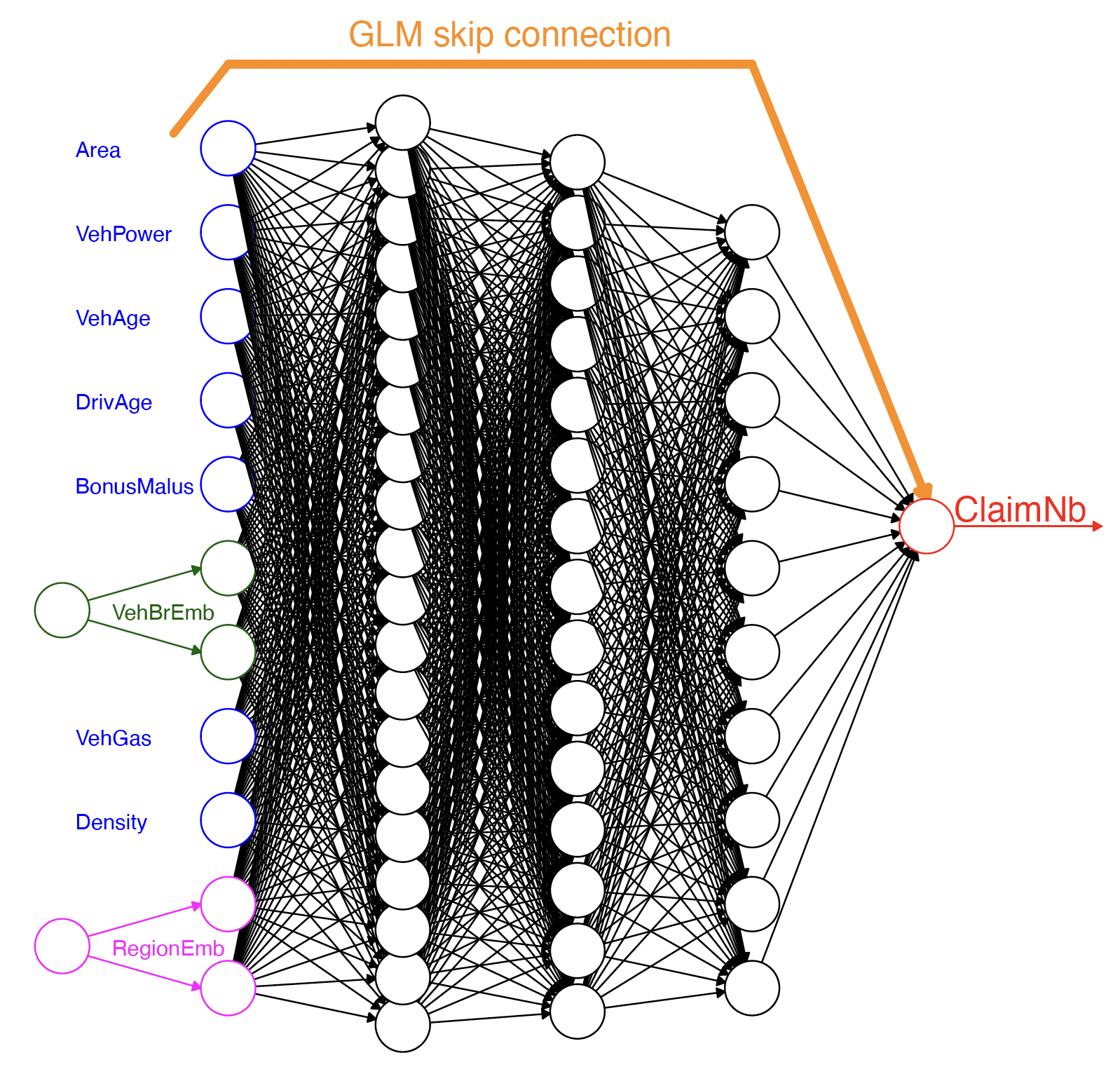

ANN can feed into a GLM

Combining GLM & ANN.

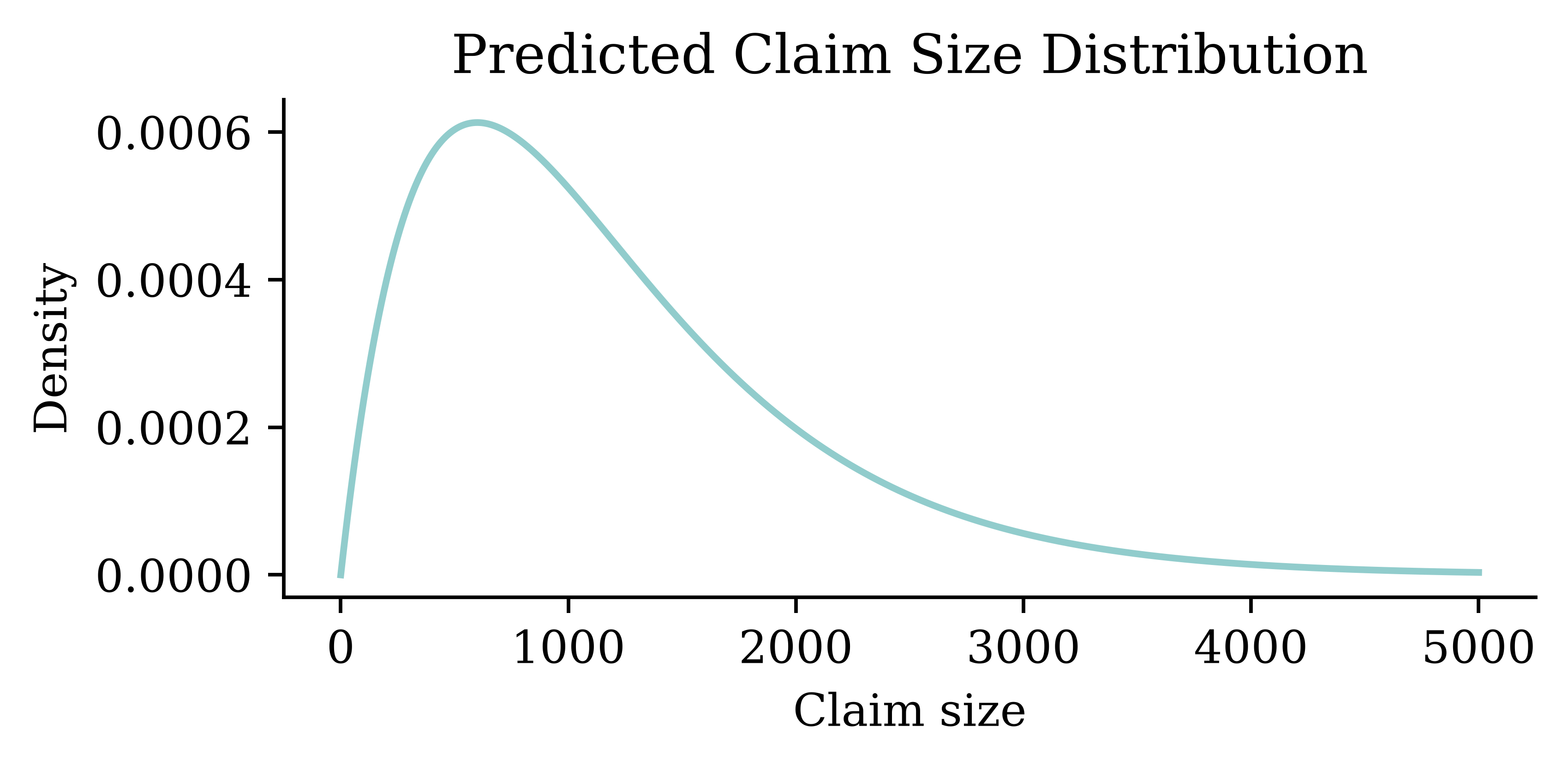

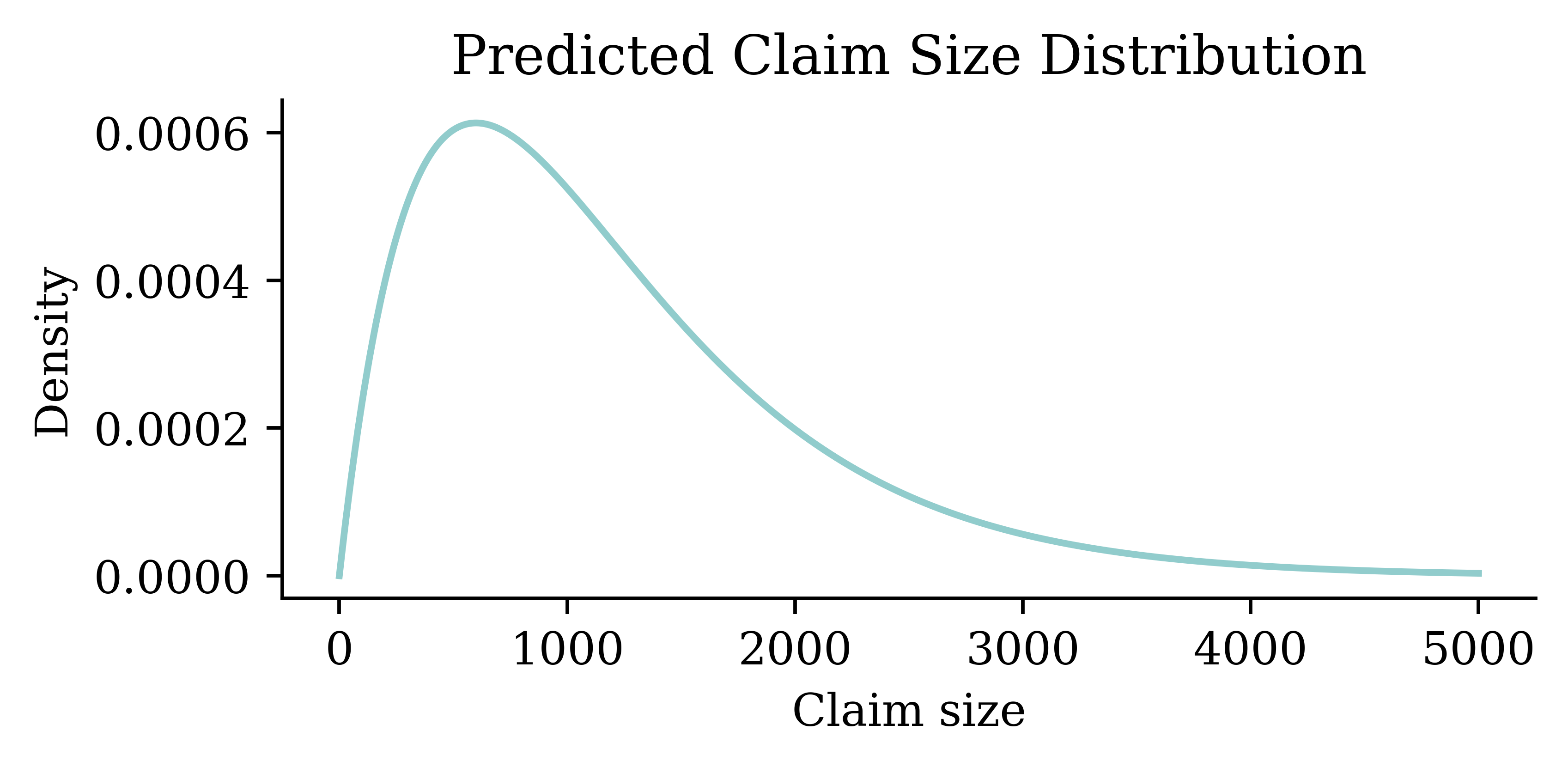

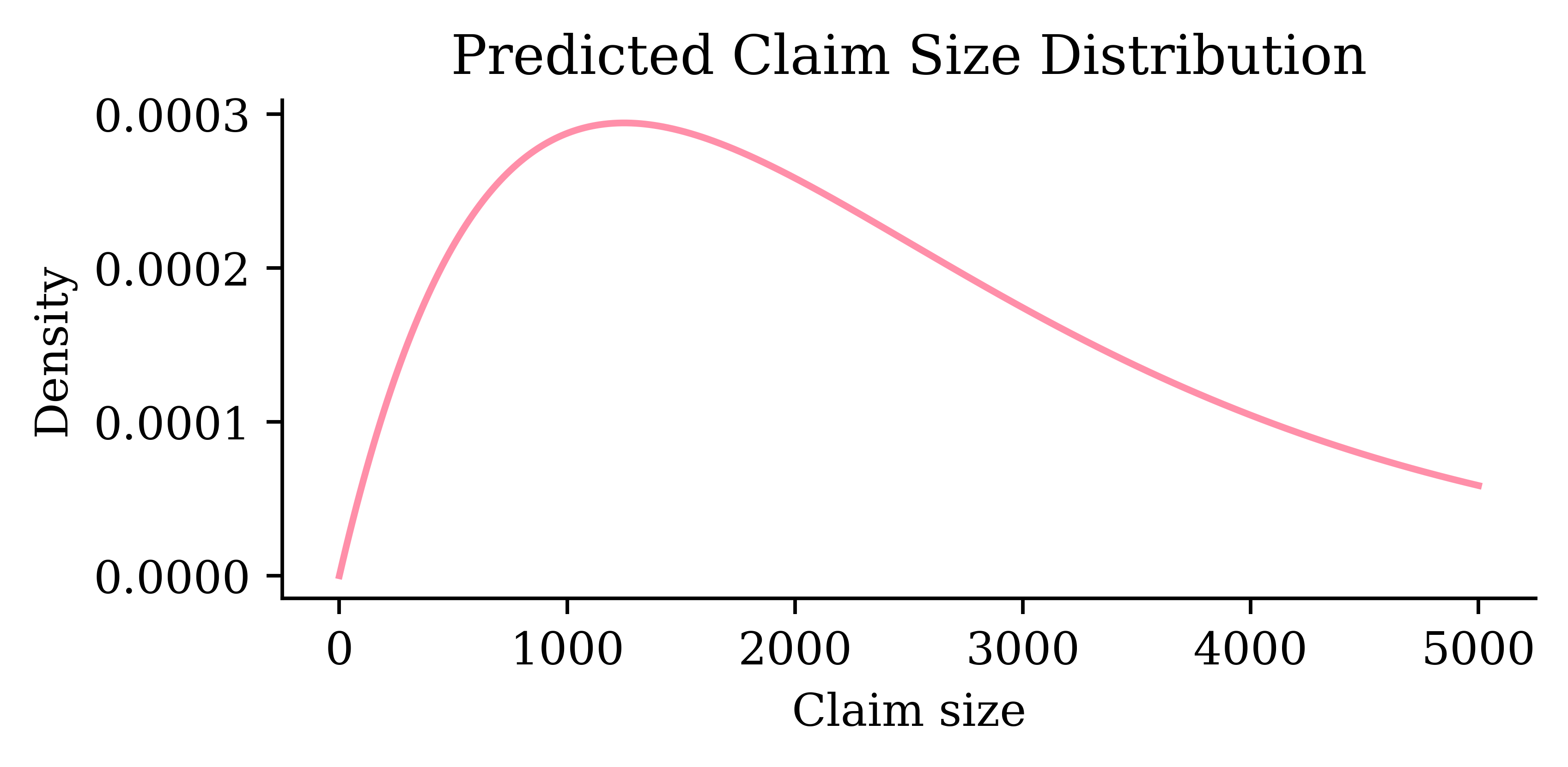

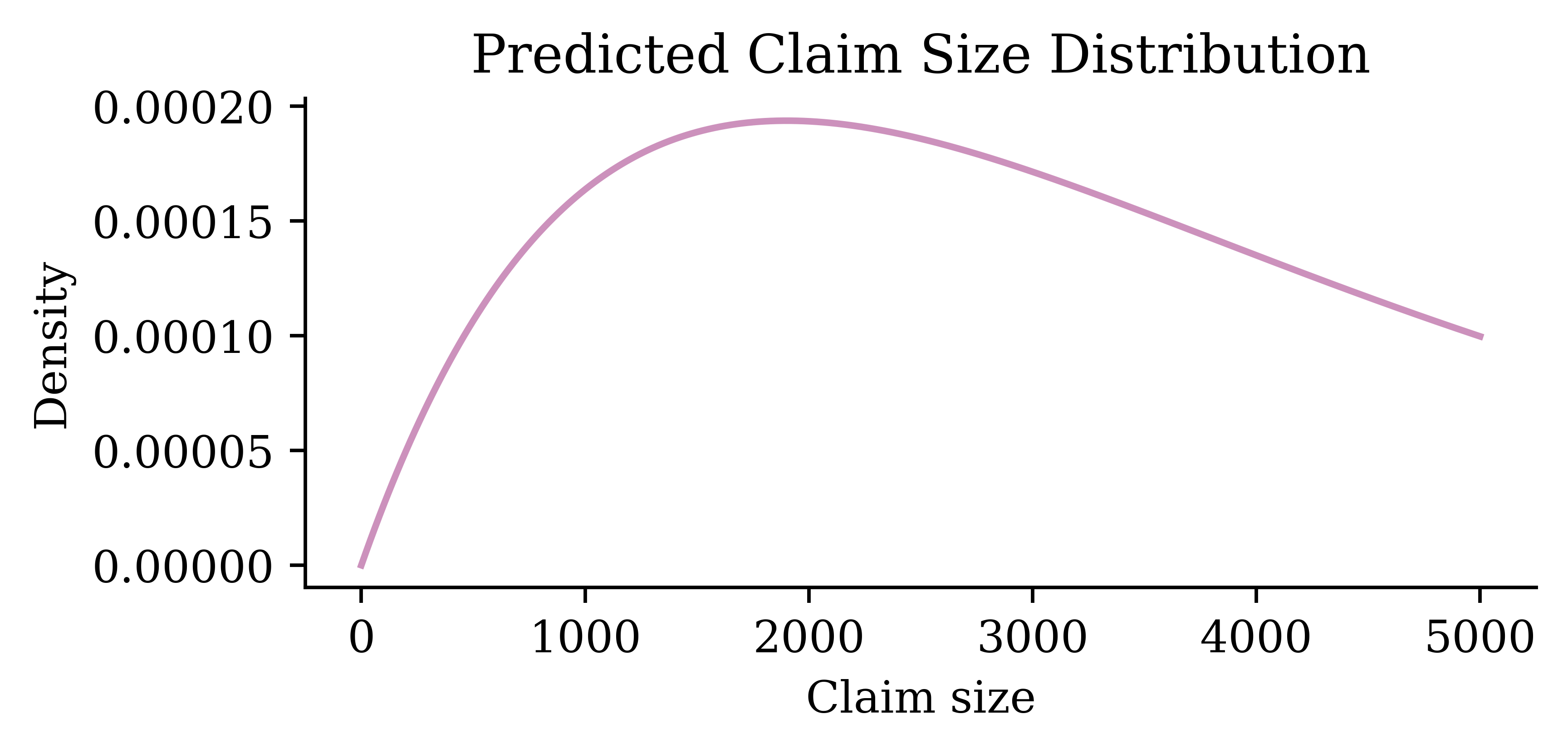

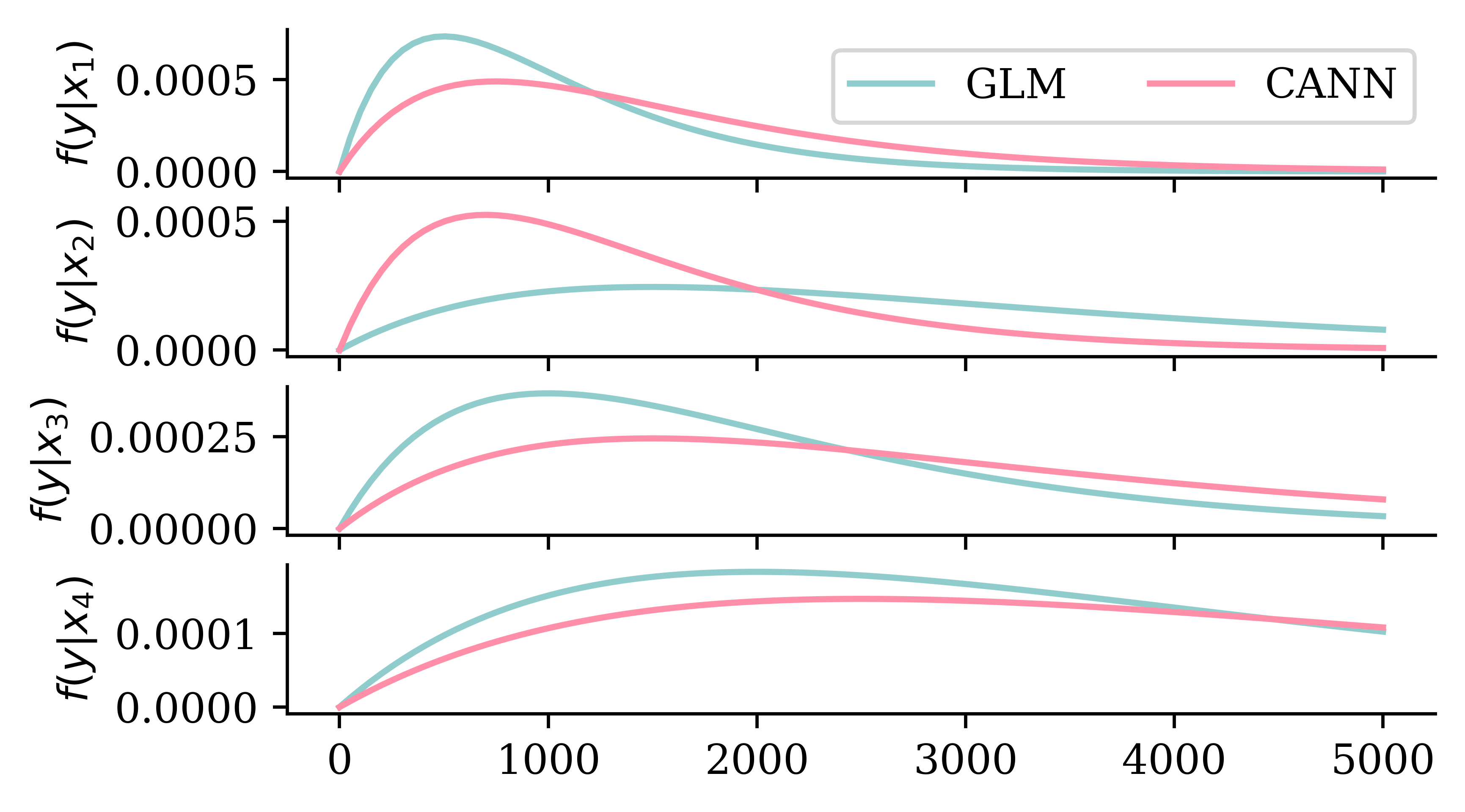

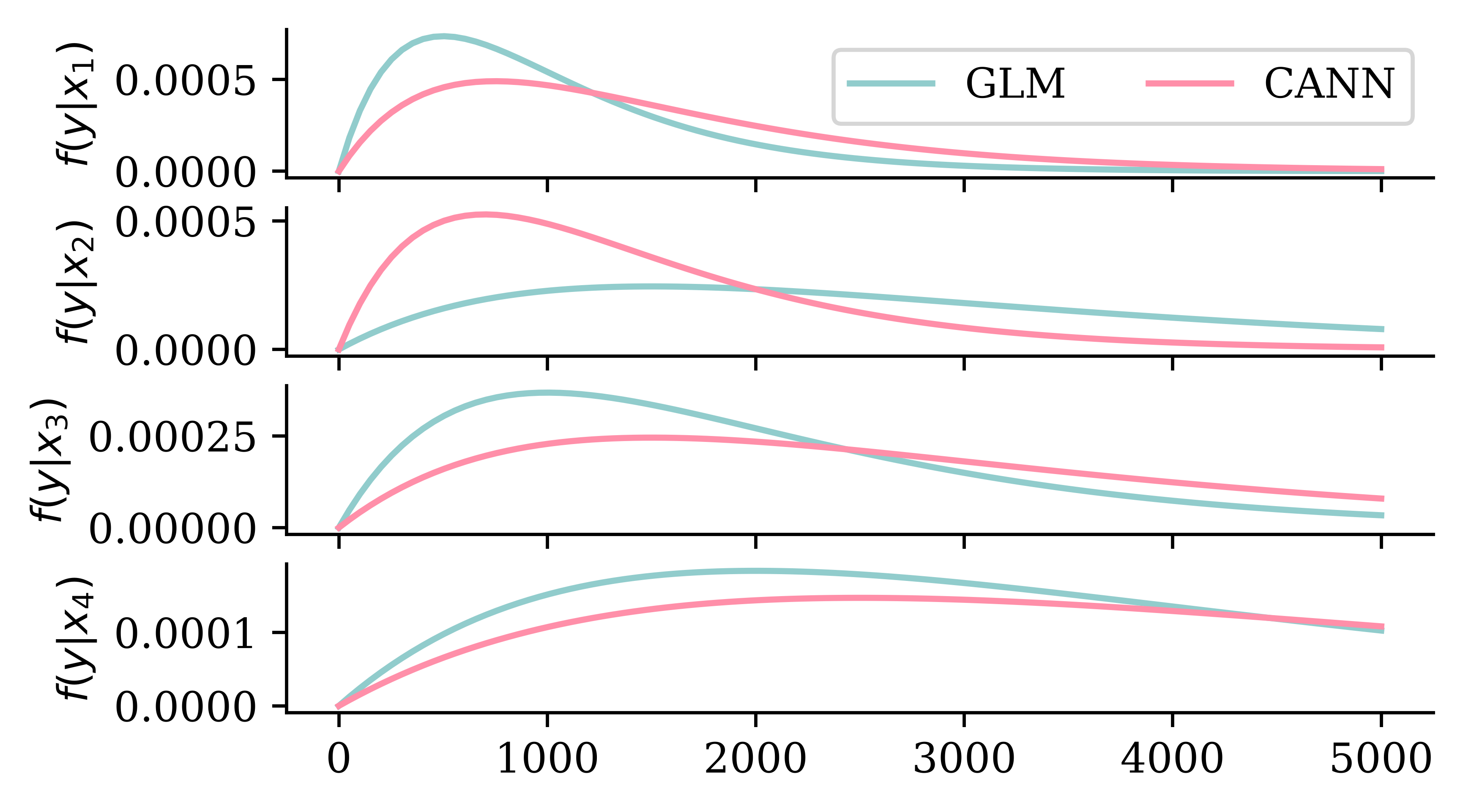

Shifting the predicted distributions

Code

# Ensure reproducibility

random.seed(1)

# Make a 4x1 grid of plots

fig, axes = plt.subplots(4, 1, figsize=(5.0, 3.0), sharex=True)

# Define the x-axis

x_min = 0

x_max = 5000

x_grid = np.linspace(x_min, x_max, 100)

# Plot a few Gamma distribution pdfs with different means.

# Then plot Gamma distributions with shifted means and the same dispersion parameter.

glm_means = [1000, 3000, 2000, 4000]

cann_means = [1500, 1400, 3000, 5000]

for i, ax in enumerate(axes):

ax.plot(x_grid, stats.gamma.pdf(x_grid, a=2, scale=glm_means[i]/2), label=f'GLM')

ax.plot(x_grid, stats.gamma.pdf(x_grid, a=2, scale=cann_means[i]/2), label=f'CANN')

ax.set_ylabel(f'$f(y | x_{i+1})$')

if i == 0:

ax.legend(["GLM", "CANN"], loc="upper right", ncol=2)

Architecture

The CANN architecture.

Generating normal distribution parameters

Our model is

Y \mid \boldsymbol{x} \;\sim\; \mathcal{N}\bigl(\mu(\boldsymbol{x}),\, \sigma^2(\boldsymbol{x})\bigr) .

In-class exercise

Make a neural network that models Y \mid \boldsymbol{x} \;\sim\; \mathcal{N}\bigl(\mu(\boldsymbol{x}),\, \sigma^2(\boldsymbol{x})\bigr).

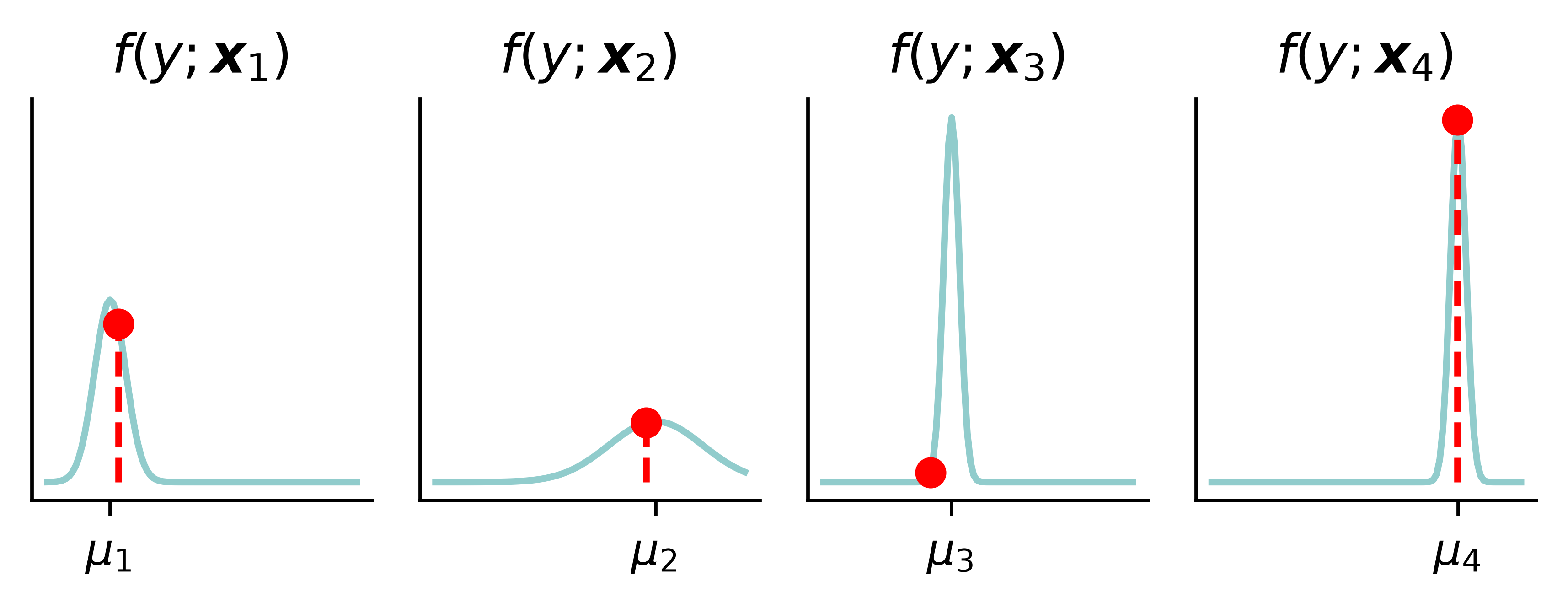

Code

y_pred = np.polyval(coefficients, X_toy[:4])

y_pred[2] *= 1.1

sigma_preds = sigma_toy * np.array([1.0, 3.0, 0.5, 0.5])

fig, axes = plt.subplots(1, 4, figsize=(5.0, 2.0), sharey=True)

x_min = y_pred[:4].min() - 4*sigma_toy

x_max = y_pred[:4].max() + 4*sigma_toy

x_grid = np.linspace(x_min, x_max, 100)

# Plot each normal distribution with different means vertically

for i, ax in enumerate(axes):

y_grid = stats.norm.pdf(x_grid, y_pred[i], sigma_preds[i])

ax.plot(x_grid, y_grid)

ax.plot([y_toy[i], y_toy[i]], [0, stats.norm.pdf(y_toy[i], y_pred[i], sigma_preds[i])], color='red', linestyle='--')

ax.scatter([y_toy[i]], [stats.norm.pdf(y_toy[i], y_pred[i], sigma_preds[i])], color='red', zorder=10)

ax.set_title(f'$f(y ; \\boldsymbol{{x}}_{{{i+1}}})$')

ax.set_xticks([y_pred[i]], labels=[r'$\mu_{' + str(i+1) + r'}$'])

# ax.set_ylim(0, 0.25)

# Turn off the y axes

ax.yaxis.set_visible(False)

plt.tight_layout();

Task: Assume you have X_train and y_train loaded and write the following code, everything up to the model.fit(X_train, y_train) line.

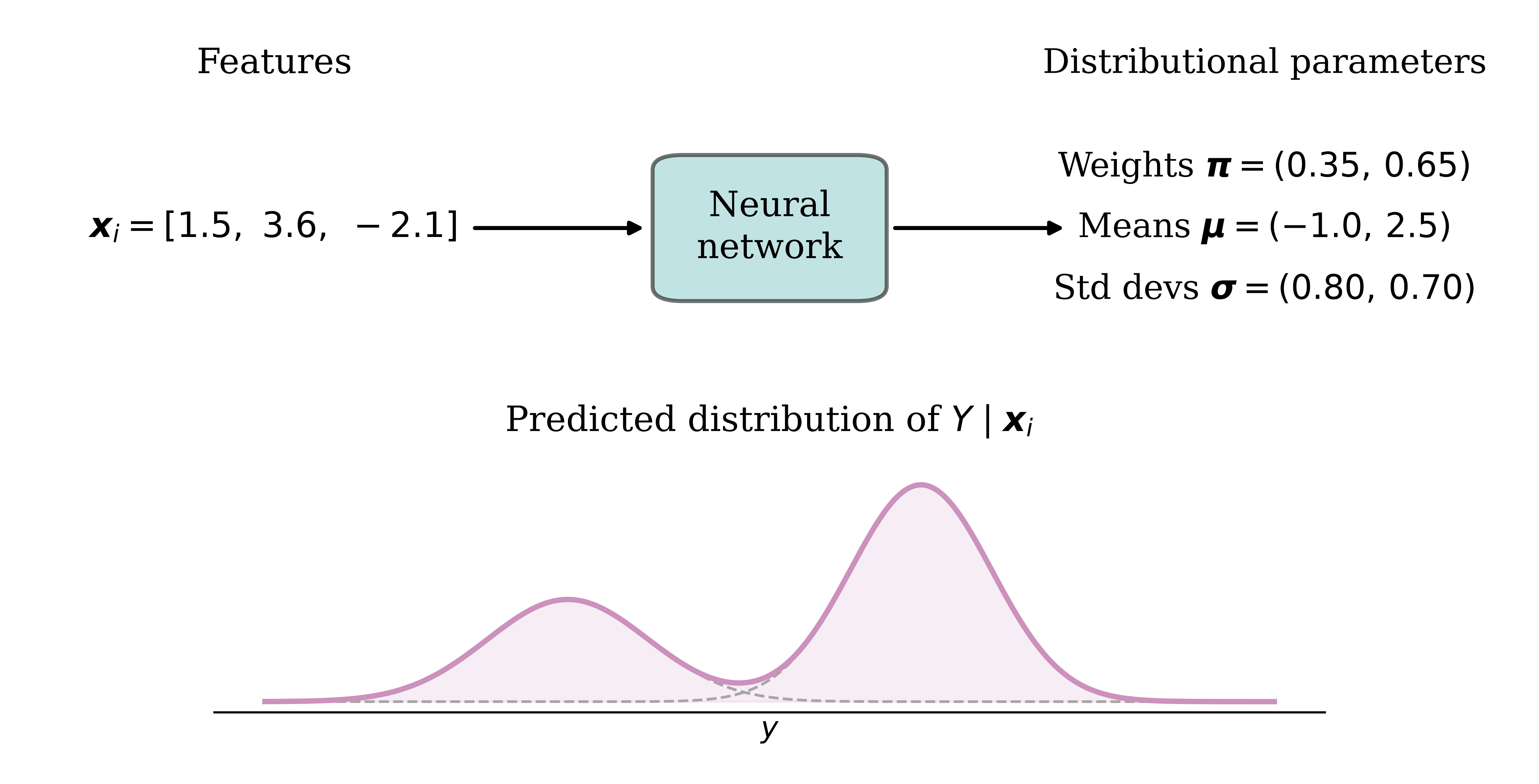

A two-component normal MDN

The Gamma MDN

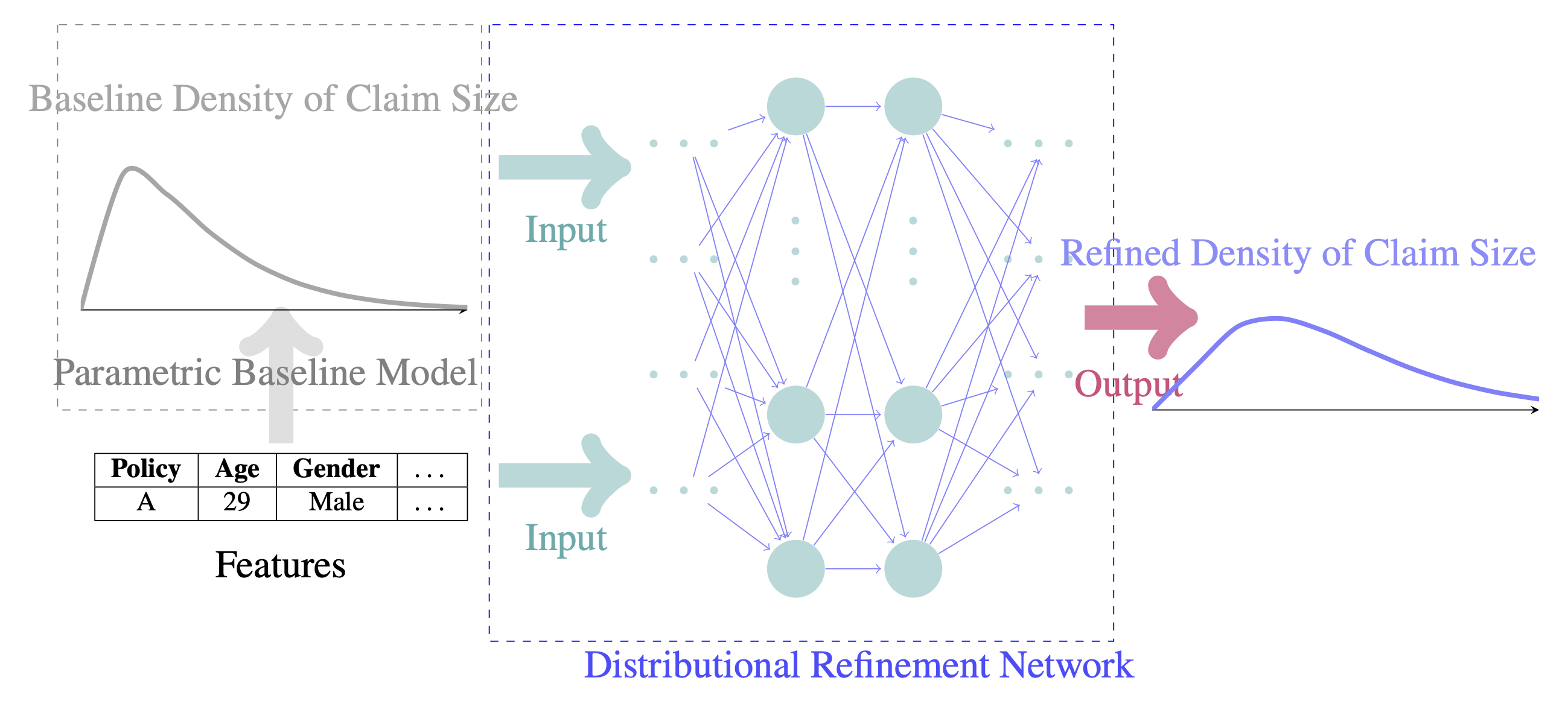

The DRN architecture

Start from a trusted parametric baseline (e.g. a GLM), then let a neural network make small adjustments to the whole distribution.

The DRN keeps the baseline’s shape but flexibly refines it using the features.

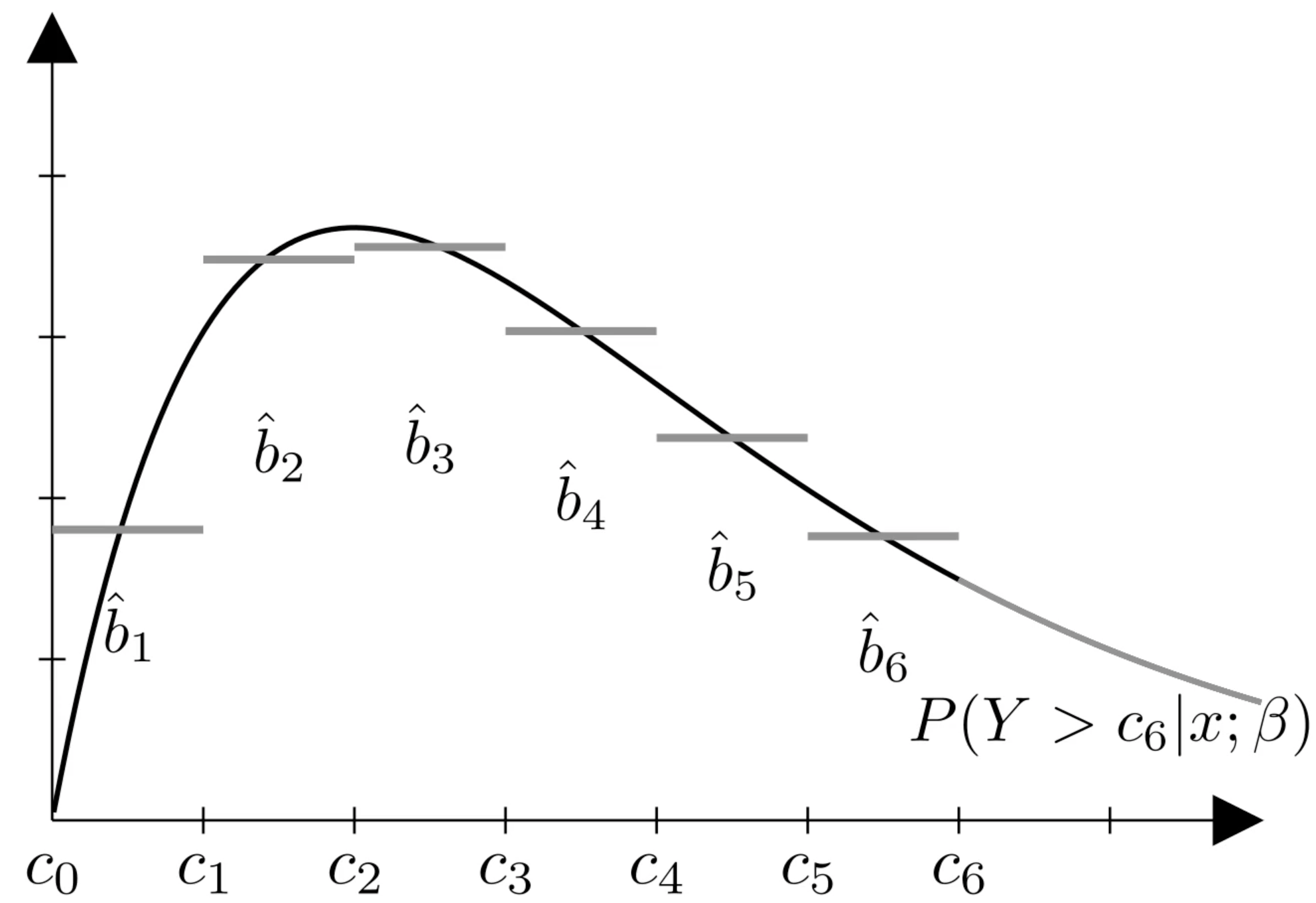

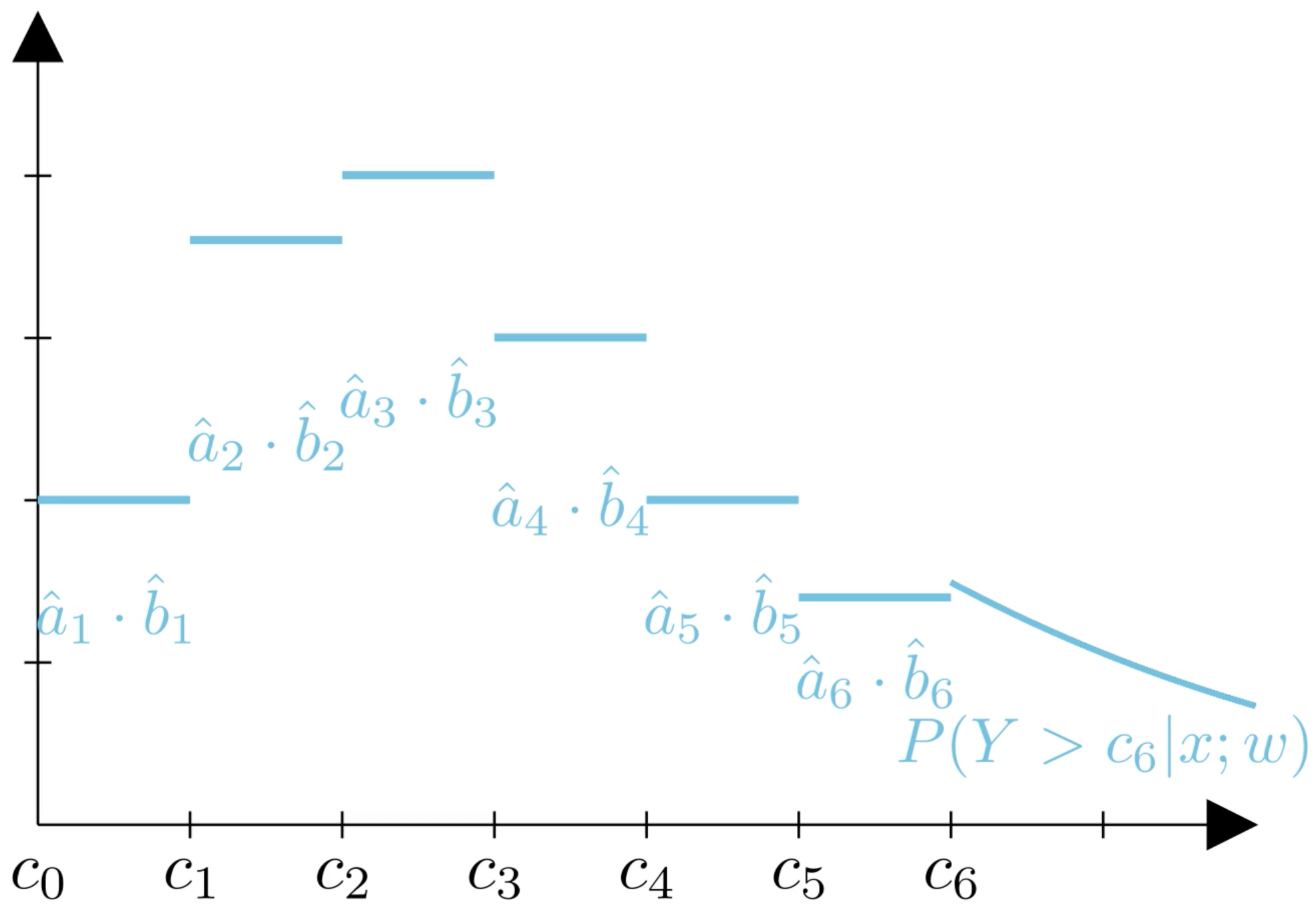

Refining the distribution

Discretise the baseline into bins, then multiply each bin’s mass by a learned adjustment factor \hat{a}_k.

A penalty keeps the adjustments faithful to the baseline, so the model stays interpretable and trustworthy.

Weights before & after L^2

Weights before & after L^1

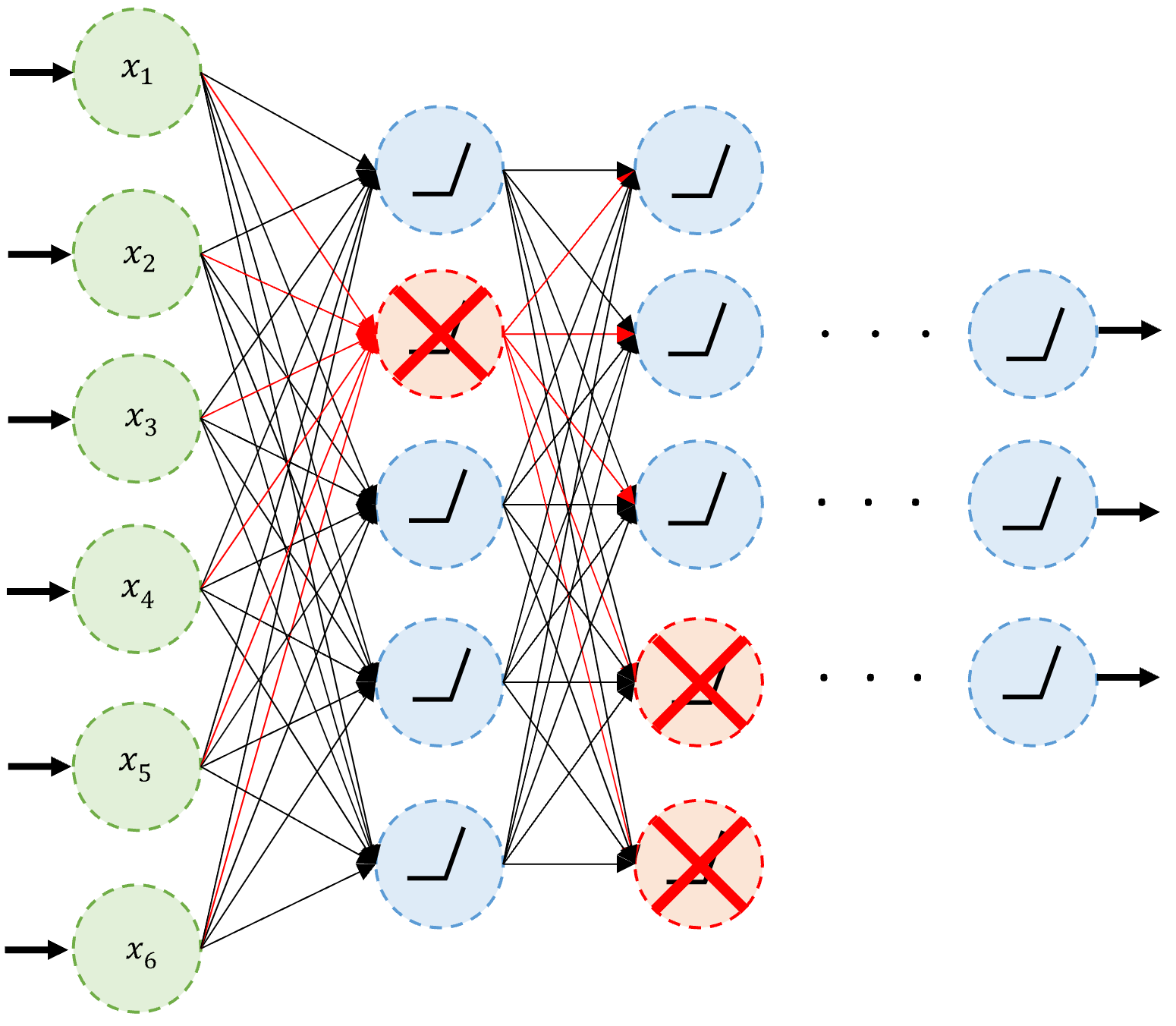

Dropout

An example of neurons dropped during training.

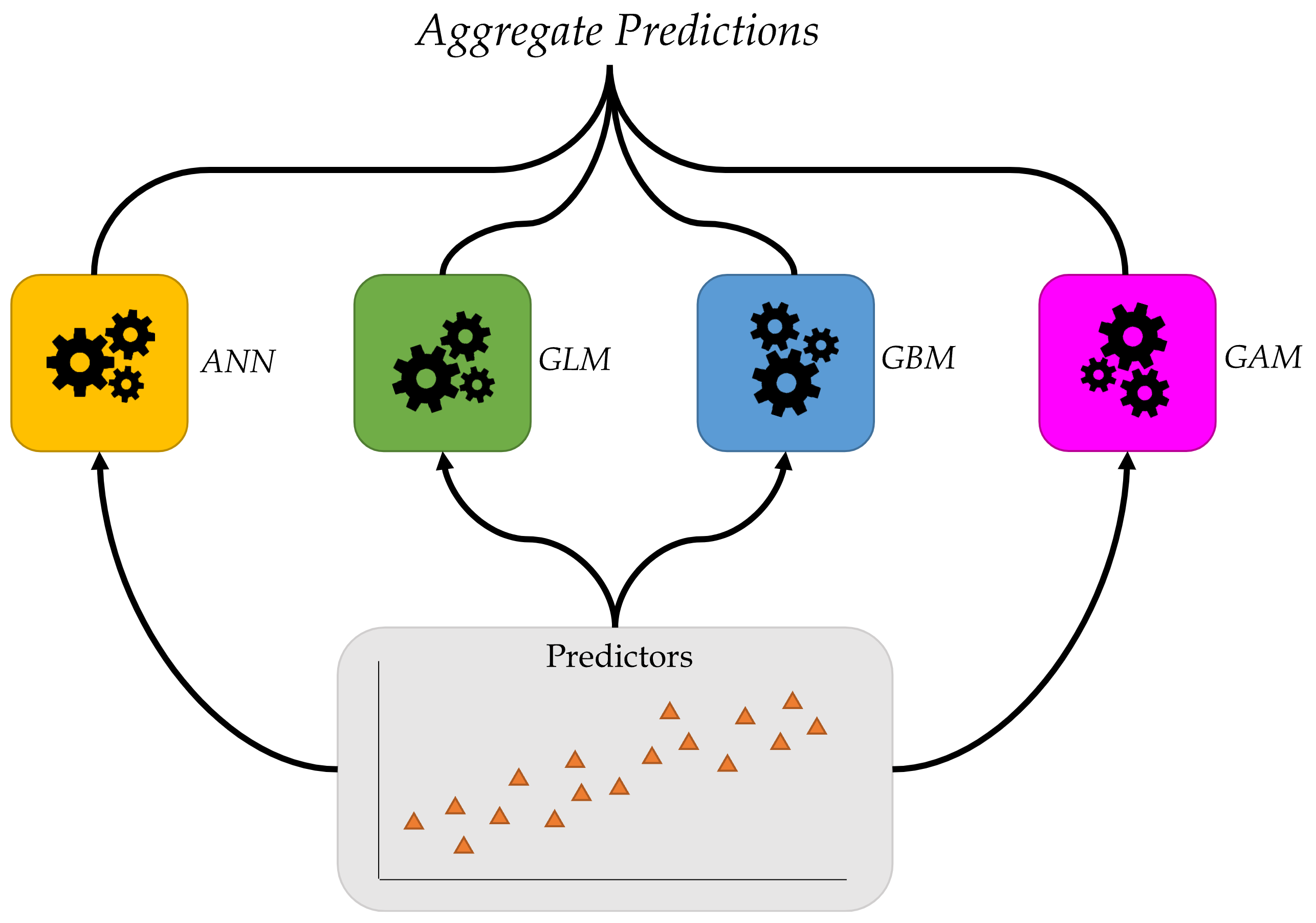

Ensembles

Combine many models to get better predictions.